Wall Street loves to make investing look entirely unapproachable for everyday people. You turn on any financial news channel and immediately see screens completely filled with flashing red and green numbers alongside complex stock charts. You hear experts yelling over each other about market predictions, inflation rates, and impending economic doom. It is honestly enough to make anyone want to hide their hard-earned money under a mattress and never think about the future.

You might think you need an expensive finance degree or countless hours of free time to research individual companies just to make a decent return in the stock market. That is simply a myth perpetuated by an industry that wants to charge you high fees for their services.

If you want a highly effective, incredibly simple, and wonderfully low-stress way to grow your wealth over time, you are reading the right guide. Legendary investors like Warren Buffett consistently recommend this exact strategy for regular folks who want to secure their financial future without losing sleep. We are going to walk you through everything you need to know about this specific type of investing. You will learn what these financial tools actually are, how they function behind the scenes to make you money, and how you can seamlessly add them to your own life. Finding the right index funds for beginners does not require any special skills or a massive bank account. You just need a little bit of patience and a willingness to let the global economy do the heavy lifting for you.

|

Concept |

Description |

Real World Benefit |

|

Stock Market |

A digital marketplace where buyers and sellers trade shares of public companies. |

Allows everyday people to own small pieces of incredibly profitable global businesses. |

|

Investing |

Putting your money to work over decades to generate a compounding profit. |

Helps your savings beat the silent wealth-killer known as inflation. |

|

Indexing |

Buying a massive, preset group of stocks rather than picking them one by one. |

Drastically reduces your financial risk and eliminates the need for deep company research. |

What Exactly Is an Index Fund?

The Definition in Simple Terms

To truly wrap your head around this concept, it helps to use a very simple and relatable analogy. Imagine you want to buy fresh fruit at your local grocery store. You could spend a massive amount of time inspecting individual apples, oranges, and bananas, desperately hoping you pick the absolute best ones of the bunch. This takes a lot of time, and sometimes you might accidentally pick a bad apple that looked perfectly fine on the outside but was rotten on the inside. An index fund is just like buying a giant, pre-packaged fruit basket. Instead of choosing individual stocks one by one and stressing over your choices, you are buying a tiny piece of hundreds or even thousands of different companies all at once with a single, easy purchase.

When looking at index funds for beginners, the absolute best way to understand them is as a convenient bundle of investments that saves you from doing any of the heavy lifting. Technically speaking, it is a type of mutual fund or exchange-traded fund that pools money from many different investors to purchase a massive group of stocks or bonds. Instead of a highly stressed person sitting at a trading desk deciding which stocks to buy and sell on a daily basis, the fund is programmed to simply copy a specific financial market index. An index is just a mathematical list that tracks the performance of a certain group of investments over time. If the companies on that list go up in value, your fund goes up in value right alongside them. If the list goes down, your fund goes down. You are just along for the ride, letting the natural growth of the businesses drive your wealth upward.

Active vs. Passive Investing

There are two primary ways to invest your money in the stock market today, and understanding the difference is crucial to your long-term success. You can choose active investing or you can choose passive investing. Active investing involves hiring a highly paid fund manager who constantly buys and sells stocks throughout the day. They spend their time reading dense financial reports, listening to corporate earnings calls, and trying to outsmart the entire market to get higher returns than everyone else. Because of all this frantic trading, deep research, and massive corporate overhead, actively managed funds charge regular investors very high annual fees. They have to pay for those fancy Wall Street offices somehow.

Index funds fall completely and entirely under the umbrella of passive investing. They do not try to beat the market at all. They just try to match it perfectly. Because there is absolutely no need for a massive team of expensive financial analysts working around the clock to pick winning stocks, the costs associated with running these funds are practically zero. You might think that paying a professional active manager would result in better returns, but the historical data strongly disagrees. Over long periods, passive investing actually performs much better than active investing simply because human beings are terrible at predicting the future. Data consistently shows that over a standard fifteen-year period, nearly ninety percent of actively managed stock funds actually fail to beat their simple benchmark index. You literally end up paying them higher fees for remarkably worse results.

|

Investing Style |

How Decisions Are Made |

Average Cost |

Historical Success Rate |

|

Active Investing |

Human managers guess which stocks will perform the best. |

Very high annual fees. |

Rarely beats the market over long periods. |

|

Passive Investing |

Computers automatically buy everything on a specific list. |

Incredibly low fees. |

Consistently matches average market growth. |

How Do Index Funds Work?

Tracking a Market Index

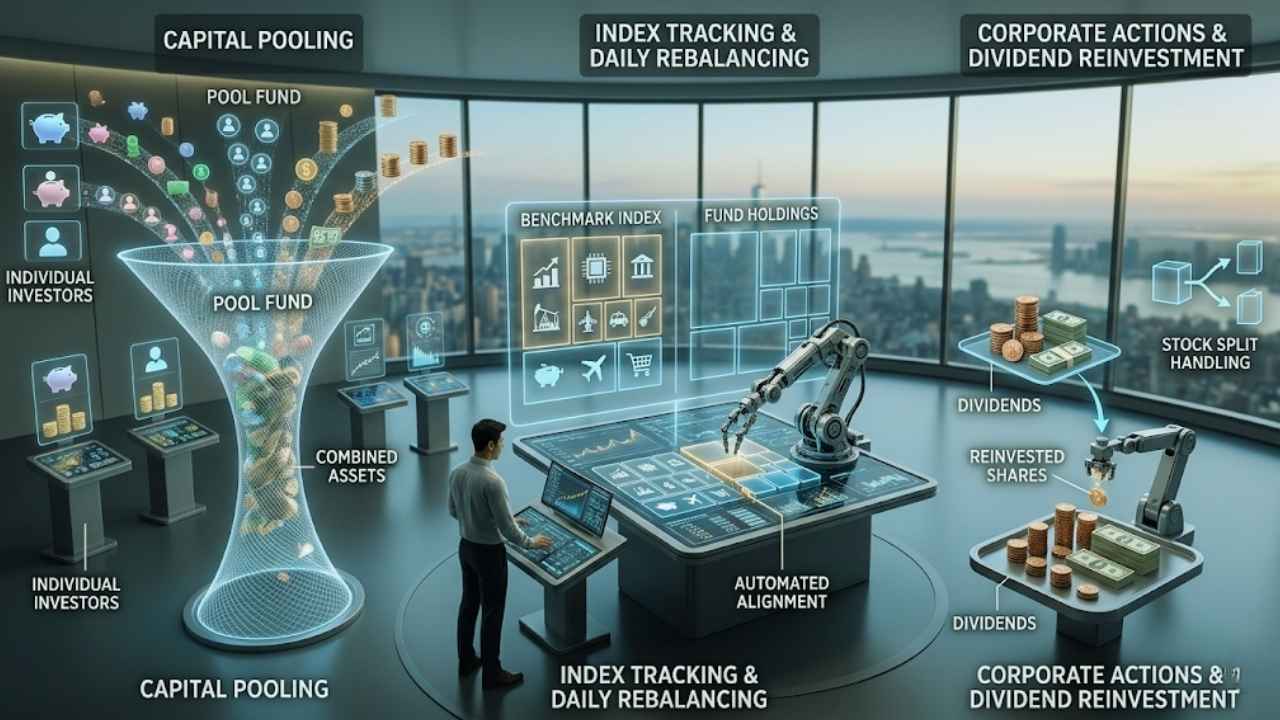

The actual mechanics behind these investments are remarkably straightforward once you peek under the hood to see how the engine runs. You definitely do not need to understand complex math or advanced economics to grasp how your money goes from your checking account into the shares of hundreds of global corporations. When you deposit your money into the fund, it joins the money of thousands of other everyday investors. The financial institution managing the fund takes that massive, combined pool of cash and strictly buys shares of the companies listed on the target index. They buy these shares in the exact same proportions that they exist on the list. This brilliant, automated nature is exactly what makes index funds for beginners such an incredibly smart and stress-free choice for building long-term wealth.

Let us say an index is made up of 500 of the largest companies in the United States, and the rules of the list dictate that larger companies get a bigger slice of the pie. If a massive tech company like Apple makes up exactly seven percent of the index, the fund manager will automatically put seven percent of all investor money directly into Apple stock. If a smaller company only makes up zero point one percent of the index, the fund buys exactly that amount. This is called market-capitalization weighting. If a struggling company eventually drops off the list entirely, the fund manager automatically sells those shares without you ever knowing. If a new, highly successful company grows large enough to be added to the list, the fund manager automatically buys it. This constant, emotionless mirror effect ensures your investment always reflects the true reality of the broader economy.

The Role of Fund Managers

You might be wondering if anyone is actually flying the plane or if the entire financial system is just run by rogue robots. While there is definitely a human manager overseeing the fund at the brokerage firm, their daily job is mostly automated by highly advanced computer algorithms. Their primary responsibility is merely to ensure the fund’s holdings accurately reflect the index it is legally supposed to track. They handle the daily inflows and outflows of cash from thousands of investors buying and selling, and they make sure the fund is constantly buying or selling the right number of shares to keep everything perfectly balanced. They do not make any subjective guesses about the future of the economy.

They also handle something incredibly important called corporate actions and dividend reinvestment. When the highly profitable companies inside the fund pay out a portion of their earnings as cash dividends, the human manager collects those massive piles of pennies and dollars. They then strategically use that cash to buy even more shares of the companies for the fund, which increases the value of your personal investment over time. They also handle things like stock splits or corporate mergers to ensure the fund remains a perfect replica of the chosen index. This extremely hands-off, administrative approach is exactly why these financial products are so incredibly cheap to own and maintain over a lifetime.

|

Mechanic |

How It Functions |

Impact on the Everyday Investor |

|

Capital Pooling |

Investor funds are combined into one massive financial account. |

Allows you to buy into incredibly expensive stocks with very little starting money. |

|

Index Tracking |

The fund strictly buys the exact stocks listed on a chosen benchmark. |

Ensures your personal returns perfectly match the overall market performance. |

|

Daily Rebalancing |

The fund automatically adjusts holdings as companies grow larger or shrink in size. |

Keeps your portfolio completely aligned with the economy without any effort on your part. |

Why Are Index Funds for Beginners So Popular?

Built-In Diversification

Putting all your financial eggs in one single basket is a terrible and highly stressful strategy for your money. If you buy stock in just one single company and that specific company becomes involved in a massive public scandal or goes completely bankrupt, you lose your entire investment overnight. Think about infamous corporate disasters like Enron or Lehman Brothers from years past. Regular people who had all their retirement money tied up in those single, supposedly safe stocks lost their entire life savings in a matter of days. You never want your financial security tied to the decision-making skills of one single corporate CEO.

Because a broad fund holds hundreds or even thousands of completely different stocks, the sudden failure of one single company will barely even register on your portfolio balance. If one major technology company has a terrible year due to new regulations, a massive healthcare company or a nationwide retail chain in that exact same fund might be having a record-breaking year of profits. The massive success of the winners easily balances out the minor losses of the losers. You are essentially betting on the entire global economy succeeding over the course of decades rather than betting on one specific horse to win a single race. This sector rotation happens naturally, protecting your money from localized industry crashes.

Lower Costs and Fees

Whenever you choose to invest your money in any type of mutual fund, you are required to pay a recurring yearly fee known as an expense ratio. This hidden fee quietly covers the cost of running the fund, paying the administrative managers, and keeping the lights on at the brokerage firm. Actively managed funds might casually charge you one full percent or more of your total investment value every single year, regardless of whether they actually made you any money. Passive funds, on the other hand, often charge practically nothing, sometimes as little as zero point zero three percent. A few modern brokerages have even introduced funds with an expense ratio of exactly zero to attract new customers.

While the mathematical difference between one percent and zero point zero three percent sounds like a laughably tiny amount of money to worry about, it is actually massive when applied over a lifetime. Thanks to the mathematical miracle of compound interest, those tiny fees aggressively multiply over decades. If you invest ten thousand dollars today and leave it completely alone for thirty years, a one percent fee could easily eat up tens of thousands of dollars of your potential future profit. Keeping your investment costs as close to zero as humanly possible is the absolute easiest and most reliable way to guarantee you have significantly more money in your pocket when you finally decide to retire.

Consistent Long-Term Performance

Historically speaking, the broader stock market has always gone up over long periods of time. This happens relentlessly despite short-term stock market crashes, severe global recessions, unexpected wars, and worldwide pandemics. By owning a small piece of the entire market, you are perfectly positioning yourself to capture that relentless, long-term upward trend of human progress and corporate innovation. Companies exist to make profits, and as long as humans continue to buy goods and services, those companies will continue to grow in value.

You definitely will not become a millionaire overnight using this incredibly boring strategy. You will never find the next hidden tech startup that explodes by a thousand percent in a single week. However, you are utilizing a slow, steady, and historically proven method that stretches back over a century. Legendary billionaire Warren Buffett famously bet one million dollars of his own money that a simple, unmanaged S&P 500 fund would easily beat a hand-picked group of highly paid hedge fund managers over a ten-year period. Buffett won the bet easily, proving once again that simple patience usually beats complex financial maneuvering.

|

Feature |

Why It Matters Scientifically |

Real World Beginner Benefit |

|

Broad Market Exposure |

You own pieces of many completely different sectors like tech, healthcare, and retail. |

You never have to guess which specific industry will perform best this year. |

|

Total Automation |

Dividends and portfolio rebalancing happen seamlessly without you clicking a button. |

You can easily set it, completely forget it, and go live your actual life. |

|

Easy Accessibility |

Modern brokerages now allow you to buy in with just a few spare dollars. |

You do not need thousands of dollars saved up to start your investing journey today. |

The Pros and Cons of Investing in Index Funds

Advantages of Index Funds

The absolute biggest advantage of this strategy is that it requires very little of your personal time or any specialized financial knowledge to manage effectively. You never need to sit down and read dense corporate balance sheets, follow boring financial news networks, or try to predict what the Federal Reserve is going to do next month. They offer instant, massive diversification across many different economic industries with one single, easy purchase on your smartphone. You are buying a tiny slice of human progress.

They also boast significantly lower fees than any actively managed alternatives, which we already know makes a absolutely massive difference to your final net worth over decades of compounding. Finally, they are highly transparent by design. You always know exactly what companies you own because the index rules are entirely public information. You will never wake up to find your rogue fund manager made a wild, risky bet on a failing company with your retirement money without telling you first.

Disadvantages and Limitations

The most glaringly obvious limitation of this strategy is that you will absolutely never beat the market average because your entire mathematical goal is just to match it. If the market goes up an average of ten percent in a year, you make exactly ten percent minus your tiny fee. You will never experience the incredible thrill of picking a single penny stock that miraculously triples in value in a single month. You trade the potential for massive, overnight wealth for the guarantee of slow, reliable growth.

You also have absolutely zero control over the individual companies the overarching fund decides to invest in. If the benchmark index includes a massive oil company, a weapons manufacturer, or a tobacco company that you deeply and morally disagree with, you are still mathematically forced to own a tiny piece of it. Finally, they are entirely subject to major, economy-wide market crashes. If the whole global economy goes into a severe recession and the market drops thirty percent, your personal portfolio is going to drop thirty percent right along with it. There is no manager actively moving your money into safe cash to protect you from the fall.

|

Pros of Passive Indexing |

Cons of Passive Indexing |

|

Incredibly low annual fees keep much more of your money directly in your pocket. |

You have absolutely no downside protection during massive, economy-wide market crashes. |

|

Provides instant diversification across hundreds of profitable companies instantly. |

You mathematically will never beat the average historical market return. |

|

Highly tax-efficient compared to active funds that trade constantly. |

You cannot easily remove specific companies you morally dislike from your personal portfolio. |

|

Requires absolutely zero specialized financial knowledge or daily effort. |

You are strictly forced to own the failing businesses right alongside the wildly successful ones. |

Examples of Popular Market Indexes

S&P 500

This is undoubtedly the most famous and widely followed financial index in the entire world. It specifically tracks 500 of the absolute largest publicly traded companies located in the United States. To even be included on this prestigious list, a company must be highly profitable and incredibly large. This list includes massive household names that you interact with every day, like Apple, Microsoft, Amazon, Google, and Johnson & Johnson. You are quite literally buying a piece of the American economy.

Many experienced financial experts strongly consider the S&P 500 to be the absolute best representation of the overall US stock market. Historically speaking, it has reliably returned an average of about ten percent per year before inflation over the last century. If you decide to only ever buy a single fund that tracks this specific index for the rest of your life, you will likely end up doing significantly better than the vast majority of people who try to actively trade stocks.

Dow Jones Industrial Average

Often simply referred to on television as the Dow, this extremely old index tracks only 30 large, highly prominent companies in the United States. You hear it mentioned excitedly on the evening news every single day without fail. When happy newscasters loudly proclaim that the market is up a thousand points today, they are almost always talking specifically about the Dow. It includes classic American businesses that have been around for generations.

While it is undeniably very famous, many modern financial experts actually strongly prefer the S&P 500 over the Dow. This is simply because 500 different companies provide vastly better diversification and safety than just 30 companies. Furthermore, the Dow is strangely weighted by the actual price of the stock rather than the total financial size of the company. This quirk makes it a slightly flawed and outdated mathematical measurement by today’s rigorous financial standards.

Nasdaq Composite

This massive index includes thousands of different stocks that trade specifically on the Nasdaq stock exchange in New York. Unlike the other lists, it is incredibly heavily weighted toward the technology sector, software developers, and massive internet companies. If a company builds computers, writes code, or runs a social media network, it is probably listed heavily on this specific index.

Funds accurately tracking this index can easily see much higher, explosive growth during massive tech booms because they hold such heavy amounts of technology stocks. However, because of this lack of industry diversification, they can also be significantly more volatile and drop much further and faster during unexpected economic downturns. It is definitely a slightly riskier index to track than the broader S&P 500, but it has completely rewarded patient investors handsomely over the last two decades.

|

Index Name |

What It Actually Tracks |

Best Suited For |

|

S&P 500 |

500 of the absolute largest publicly traded US companies. |

Core portfolio building and incredibly reliable general US market exposure. |

|

Dow Jones |

30 massive, highly influential US corporate giants. |

Tracking traditional, old-school blue-chip industrial stocks. |

|

Nasdaq Composite |

Over 3,000 stocks, very heavily focused on modern technology. |

Investors actively looking for higher growth and comfortable with wild volatility. |

How to Invest in Index Funds in 4 Simple Steps

Step 1: Choose Your Account Type

Before you can actually buy any investments at all, you desperately need a specialized financial account to safely hold them. If you are specifically saving for your distant retirement and do not plan to actually touch the money for several decades, you should immediately open an Individual Retirement Account. A Traditional IRA or a Roth IRA offers massive, completely legal tax benefits that powerfully shield your growing money from the government over time.

If you just want to invest for general, everyday wealth building, perhaps to easily buy a new house in ten years or fund a child’s education, a standard taxable brokerage account is definitely the way to go. You absolutely will not get the special government tax breaks, but you can freely withdraw your money at any time without facing any strict financial penalties. You can easily open either of these accounts online in about ten minutes.

Step 2: Pick an Index to Track

Next, you need to firmly decide what specific part of the global market you actually want to invest your hard-earned money in. For the vast majority of absolute beginners, a broad market index like the S&P 500 or a Total US Stock Market index is the absolute perfect, foolproof starting point. It provides massive exposure to the entire US economy in one incredibly clean, easy-to-understand package.

If you want to be even more aggressively diversified to protect yourself, you could also easily add a Total International Stock Market index to your new portfolio. This simple addition allows you to easily own small pieces of thousands of different companies located in Europe, Asia, and rapidly emerging global markets, protecting you if the US economy ever briefly slows down.

Step 3: Select a Specific Fund

Many entirely different financial companies fiercely compete to offer you funds that track the exact same mathematical index. For example, massive industry giants like Vanguard, Fidelity, and Charles Schwab all proudly offer their own specific, branded version of an S&P 500 fund. Despite having completely different names, they all literally hold the exact same 500 stocks in the exact same mathematical proportions.

Your only real job here is to carefully look at the advertised expense ratios and ruthlessly choose the one with the absolute lowest annual fees. Also, you should quickly check to see if the brokerage requires a large minimum investment just to get started. Fidelity, for instance, amazingly allows you to start investing with just one single dollar, making it incredibly accessible for people who are just starting out with very little spare cash.

Once you have securely linked your personal bank account and deposited your initial money, simply use the brokerage app’s search bar to easily find the fund’s specific ticker symbol. A ticker symbol is just a short three to five-letter identification code used by the stock market. Enter the exact amount of money you want to invest and confidently hit the buy button to become a partial owner of hundreds of businesses.

The absolute most crucial part of this final step is to immediately set up automated, recurring monthly transfers. You should instruct your brokerage to automatically pull fifty or a hundred dollars directly out of your checking account every single payday. This brilliant strategy ensures you systematically invest consistently through good markets and bad markets, entirely removing human emotion and actively building your massive wealth on total autopilot.

|

Step |

Action Required |

Pro Tip for Beginners |

|

1. Choose Account |

Open a specialized IRA, Roth IRA, or standard brokerage account online. |

Always use a Roth IRA if you are saving for retirement to get entirely tax-free growth. |

|

2. Pick Index |

Decide carefully between the S&P 500, Total Stock Market, or International. |

A Total Stock Market fund easily gives you massive exposure to large, medium, and small companies alike. |

|

3. Select Fund |

Find a highly reputable, low-cost fund from Vanguard, Fidelity, or Schwab. |

Always look for an expense ratio well under 0.10 percent to save money. |

|

4. Automate |

Set up strict, monthly recurring cash transfers from your primary checking account. |

Boring consistency matters vastly more than trying to perfectly time the unpredictable market. |

Index Funds vs. Mutual Funds vs. ETFs

Index Funds vs. Traditional Mutual Funds

As you enthusiastically read modern books and endless articles about investing, you will constantly see these three specific terms thrown around casually. It can quickly get incredibly confusing because financial experts often use them completely interchangeably, even when they actually mean slightly different things. Clearing up this common confusion is essential for your confidence.

As we thoroughly covered earlier, an index fund is actually just a very specific flavor or style of a mutual fund. The only real difference lies entirely in the underlying management strategy. Traditional mutual funds are highly actively managed by stressed human beings sitting in offices frantically trying to guess which individual stocks will miraculously go up next month. Passive mutual funds are simply managed by cold computers to perfectly copy a boring list. When you hear financial advisors loudly tell you to avoid mutual funds because of their ridiculously high fees, they are talking strictly about the active ones, not the passive ones you are buying.

Index Funds vs. Exchange-Traded Funds

You can actually choose to buy your chosen index in two entirely different physical formats through your brokerage app. You can buy it formatted as a traditional mutual fund, or you can buy it formatted as an Exchange-Traded Fund, which absolutely everyone simply calls an ETF. Both formats do the exact same underlying job of perfectly tracking a specific index and making you money.

The main difference is simply how they operate technically on the backend of the stock market. ETFs trade freely on the open stock market throughout the entire day exactly like regular corporate stocks. You can easily buy or sell an ETF at ten in the morning, and the price will rapidly change by the minute. Mutual funds, however, only ever trade exactly once a day. If you place a buy order at noon, it will not actually execute until the market officially closes at four in the afternoon. ETFs also tend to be slightly more tax-efficient if you hold them in a standard taxable account. For a beginner securely holding investments for twenty years, both are absolutely excellent choices.

|

Investment Vehicle |

Trading Style and Speed |

Pricing Mechanism |

Best Suited For |

|

Traditional Mutual Fund |

Trades exactly once per day directly after the market officially closes. |

Priced exactly once per day based on closing numbers. |

Highly automated, completely hands-off monthly investing strategies. |

|

Exchange-Traded Fund (ETF) |

Trades rapidly all day long exactly like a regular corporate stock. |

Price fluctuates wildly by the second during market hours. |

Investors who want extreme flexibility and slightly lower tax burdens. |

|

Index Fund |

Can technically be formatted as either a mutual fund or an ETF. |

Completely depends on the chosen format. |

Reliable, long-term wealth accumulation for retirement. |

Final Thoughts

Building wealth does not require you to take extreme risks, trade cryptocurrency in the middle of the night, or have a master’s degree in finance. Wall Street thrives on making you think you cannot do this yourself, but you absolutely can. By keeping your costs incredibly low, diversifying your portfolio across the entire global economy, and investing consistently every single month, you are setting yourself up for massive success.

These simple financial tools provide the perfect vehicle for a stress-free investment strategy. The most important step you can take right now is simply to open an account and get started. Finding the right index funds for beginners is just the first hurdle. Once you set up your automated contributions, just stay patient, ignore the scary news headlines, and let the math of compound interest do all the heavy lifting for you over the next few decades.

Frequently Asked Questions (FAQs) About What is Index Fund

What is tracking error?

Tracking error is the slight difference in performance between your fund and the actual index it is copying. Because the fund has tiny fees and has to manage cash flows from investors buying and selling, it will never match the index to the exact penny. A good fund will have a tracking error of just a fraction of a percent.

Do I have to pay taxes on my funds if I do not sell them?

If your investments are in a standard taxable account, you will have to pay taxes on any dividends the fund pays out to you during the year, even if you automatically reinvest them. However, you do not pay capital gains taxes on the growth of the fund itself until you actually sell your shares. If you use a Roth IRA, you do not pay taxes on the growth or the dividends at all.

What happens if the company that runs my fund goes bankrupt?

If a massive brokerage like Vanguard or Fidelity were to go bankrupt, your money does not disappear. Brokerages are legally required to keep investor assets completely separate from their own corporate assets. You own the underlying stocks in the fund, not the brokerage. Another financial institution would simply step in and take over the management of the fund.

{kind=link}