Picking a life insurance policy is one of those adult responsibilities that feels unnecessarily complicated until you break it down into simple math. In 2026, the world looks a bit different than it did a decade ago, with a global market hitting over $9 trillion and more people looking for financial certainty in an unpredictable economy.

The main clash has always been term vs whole life insurance, and while the names sound simple, the impact on your long-term wealth is massive. Most people treat insurance like a “set it and forget it” bill, but the truth is that your choice determines whether you are just buying a safety net or building a complex financial asset. We are going to dig into the actual mechanics of these policies, looking at the 2026 costs and the real-world utility of each so you can stop guessing and start planning.

Understanding the Simplicity of Term Life Insurance

Term life insurance is the purest form of financial protection you can buy because it does exactly one thing: it pays out if you pass away within a specific timeframe. You choose a term, like 10, 20, or 30 years, pay a monthly fee, and that is the end of the story. There are no hidden fees, no investment accounts to track, and no complicated tax strategies to worry about.

For most families in 2026, this remains the most popular choice because it provides the largest possible payout for the smallest monthly cost. It acts like a safety harness that you wear only while you are climbing the most dangerous parts of your financial mountain, such as when you have a large mortgage or young children who depend entirely on your income.

|

Term Life Metric |

2026 Data & Details |

|

Average Cost (Age 30) |

$18 – $25 per month for $500k coverage |

|

Duration Options |

10, 15, 20, 25, 30, or 35 years |

|

Cash Value |

Zero (no savings component) |

|

Underwriting Speed |

2026 “Instant” tech allows approval in minutes |

|

Best Utility |

Debt protection and income replacement |

The Fixed Window of Protection

A term policy is essentially a contract with a deadline. If you buy a 20-year policy at age 30, it protects you until you are 50. If you are still healthy and living at 51, the policy ends, and you don’t get your premiums back. This is why some people call it “rented” insurance, as you are paying for the right to be covered only during your most vulnerable years.

Maximum Coverage for Minimum Cost

The biggest draw of term is the price. Because the insurance company knows there is a high statistical chance you will outlive the policy, they can afford to charge very little. In 2026, this allows a young family to get a million dollars in coverage for the price of a couple of pizzas a month, leaving more money for their actual investments.

The Permanent Nature of Whole Life Insurance

Whole life insurance is a permanent contract that stays active as long as you live, provided you keep up with the premium payments. Unlike term, this policy creates a “cash value” savings account that grows at a guaranteed rate over time. It is a slow-burn financial tool that many high-net-worth individuals use to ensure there is always a pot of money waiting for their heirs, regardless of how long they live.

In the 2026 financial landscape, where market volatility can make traditional savings feel risky, the guaranteed growth of whole life offers a level of stability that many find comforting. However, that stability comes at a high price, often costing ten times more than a term policy for the same death benefit payout.

|

Whole Life Metric |

2026 Data & Details |

|

Average Cost (Age 30) |

$350 – $500 per month for $500k coverage |

|

Duration |

Lifelong (no expiration date) |

|

Cash Value |

Guaranteed growth + potential dividends |

|

Loan Access |

Can borrow against policy after 3-5 years |

|

Tax Status |

Tax-deferred growth and tax-free death benefit |

Building a Living Asset

The cash value component is what sets this apart. A portion of every dollar you pay goes into an internal account that you can eventually borrow against for things like a down payment on a house or an emergency fund. You don’t have to die to see the value, which makes it feel more like a bank account combined with a life insurance policy.

Fixed Premiums for Life

One of the most attractive features is that your premium stays the same forever. If you lock in a rate at age 25, you will pay that same amount when you are 85. Even as your health declines or you get much older, the insurance company cannot raise your rates, providing a predictable line item in your long-term budget.

Side-by-Side: Term vs Whole Life Insurance Comparison

When you put term vs whole life insurance in a direct head-to-head match, the winner depends entirely on your goals. Term is designed for people who want to protect a specific risk, like a mortgage that will eventually be paid off. Whole life is for people who want to manage their taxes or leave a guaranteed legacy.

In 2026, the gap between the two has widened because term insurance has become cheaper thanks to better data analytics, while whole life remains an expensive, specialized product. You have to decide if you want to pay for a temporary shield or a permanent foundation, and the table below breaks down exactly how those two philosophies differ in practice.

|

Feature |

Term Life Insurance |

Whole Life Insurance |

|

Monthly Premium |

Very Low ($) |

Very High ( ) |

|

Coverage Length |

Temporary (ends after term) |

Permanent (lasts for life) |

|

Cash Value |

None |

Guaranteed growth |

|

Flexibility |

High (cancel anytime) |

Low (early cancellation is costly) |

|

Death Benefit |

Fixed |

Can grow with dividends |

|

Complexity |

Simple |

Highly Complex |

Evaluating the Cost-to-Benefit Ratio

If you are looking at your bank account today, term gives you the biggest bang for your buck right now. It covers your largest risks for the least amount of cash. Whole life, however, is a marathon. It feels expensive and “not worth it” in the first ten years, but for those who hold it for forty years, the accumulation of cash value can become a significant part of their net worth.

Strategic Keyword Subhead: Term vs Whole Life Insurance Use Cases

You should think of term as “income replacement” and whole life as “estate planning.” If your family would starve without your paycheck tomorrow, buy term. If your family is already wealthy and you want to make sure your kids can pay the inheritance taxes on your mansion and businesses, whole life is the tool that handles that specific problem.

The Strategy of Buying Term and Investing the Rest

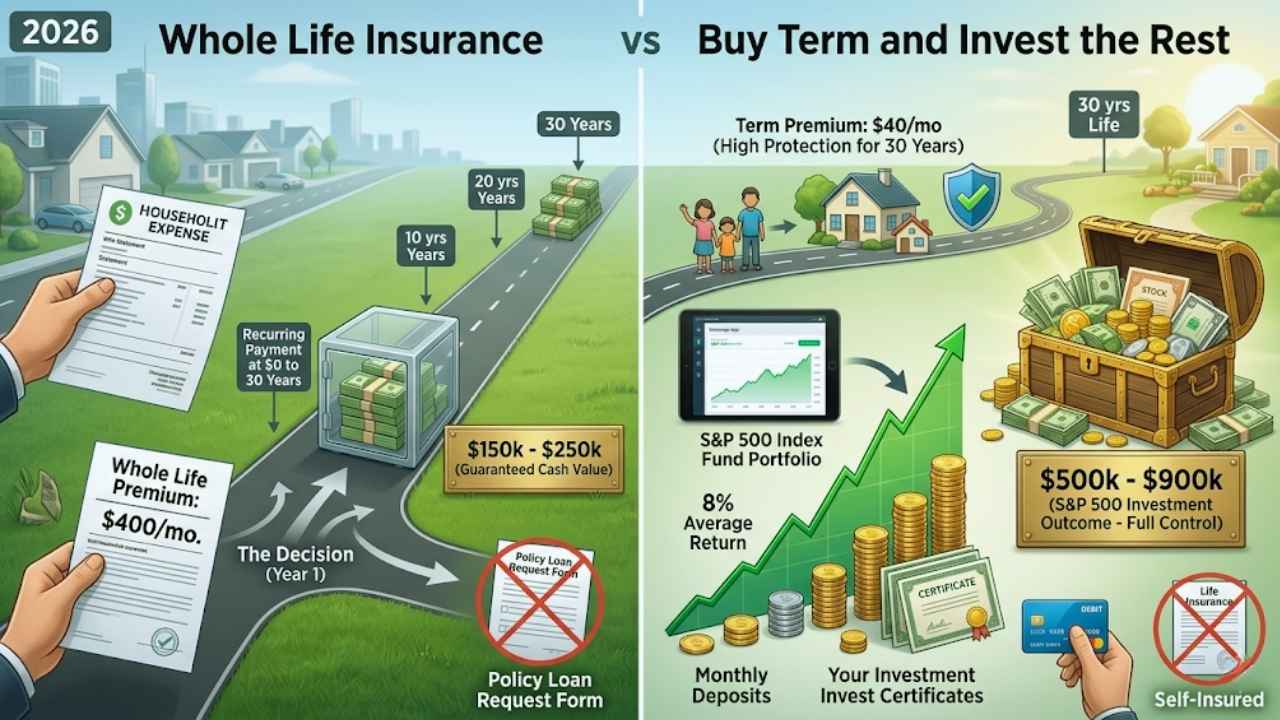

A popular strategy in 2026 that continues to gain steam is “Buy Term and Invest the Rest.” The idea is that instead of paying $400 a month for a whole life policy, you pay $40 for term insurance and put the other $360 into a diversified investment account like an S&P 500 index fund. Historically, the returns from the stock market far outpace the 2% to 4% guaranteed growth you might find inside a whole life policy.

This approach gives you the high protection of a life insurance payout while your kids are young, but it also builds a much larger pile of liquid cash that you can access without having to ask an insurance company for a loan. By the time the term policy ends, you are “self-insured” because your investment account is large enough to cover any needs.

|

Investment Path |

Estimated 30-Year Outcome |

Control Level |

|

Whole Life Cash Value |

$150k – $250k (Guaranteed) |

Managed by Insurer |

|

S&P 500 Index Fund |

$500k – $900k (Based on 8% Avg) |

Full User Control |

|

Real Estate Portfolio |

Variable Growth + Cash Flow |

High Management |

|

Savings Account |

$130k – $160k (Inflation Risk) |

High Liquidity |

The Power of Compound Interest

When you invest the difference yourself, you are taking advantage of the stock market’s growth without the high management fees and commissions that insurance companies bake into whole life policies. Over 20 or 30 years, those saved fees turn into hundreds of thousands of dollars in your own pocket rather than the insurer’s pocket.

Maintaining Financial Discipline

The only risk to this strategy is human nature. If you buy the cheap term policy but then spend the extra money on vacations and expensive cars instead of investing it, you end up with nothing when the term expires. For the disciplined saver, this is the superior wealth-building path, but for the impulsive spender, the “forced savings” of whole life might be safer.

2026 Market Trends: Technology and Underwriting

The insurance industry has been dragged into the digital age, and in 2026, the process of getting a policy is faster than it has ever been. We have moved away from the days of waiting six weeks for a nurse to come to your house and draw blood. Now, “accelerated underwriting” uses your digital footprint, prescription history, and even your driving records to assess your risk in real-time.

This has made term vs whole life insurance shopping much easier for the consumer. You can compare ten different companies in five minutes and have a policy active by the time you finish your coffee. This transparency is forcing companies to be more competitive with their rates, which is great news for your wallet.

|

2026 Trend |

Impact on Consumers |

|

AI Underwriting |

Instant approvals for healthy adults |

|

Wearable Integration |

Discounts for sharing Apple Watch/Fitbit data |

|

Micro-Policies |

Short-term 1-year coverage for specific trips/tasks |

|

Digital Death Benefits |

Faster payouts to beneficiaries via blockchain |

The Death of the Medical Exam

For most people under age 50 seeking less than $1 million in coverage, the traditional medical exam is becoming a thing of the past. Algorithms can now predict your life expectancy with incredible accuracy based on data points you’ve already generated. This has removed the biggest hurdle to getting covered, which was the “hassle factor” of doctors and needles.

Personalized Pricing via Data

In 2026, if you live a healthy lifestyle, you can prove it. Many insurers now offer “wellness riders” where you can sync your fitness tracker to your policy. If you hit your step goals and keep your heart rate in a healthy zone, the company might give you a 5% to 10% discount on your premiums, making both term and whole life more affordable for the health-conscious.

Choosing Based on Your Current Life Stage

Your age and where you are in your career should be the final deciding factor in the term vs whole life insurance debate. A 25-year-old starting their first job has zero need for a permanent legacy, but they have a massive need for low-cost protection to cover their student loans.

Meanwhile, a 55-year-old whose children have graduated and whose house is paid off might look at a whole life policy as a way to leave a tax-free gift to their grandchildren. The right choice today might not be the right choice in twenty years, which is why understanding the flexibility of each policy is so vital to your success.

|

Life Stage |

Ideal Policy Type |

Why? |

|

Gen Z / Single |

Low-Cost Term |

Protect co-signers on loans |

|

Young Families |

20-30 Year Term |

Replace income during high-debt years |

|

Established Career |

Convertible Term |

Keep options open for permanent later |

|

Legacy Planning |

Whole Life |

Guaranteed payout for final expenses |

The New Parent Strategy

If you just brought a baby home, your world has changed. You suddenly have a 20-year liability sitting in a crib. A 20-year term policy is the perfect “set it and forget it” tool to ensure that child is taken care of until they are through college. It is the most selfless financial move you can make for a very low monthly price.

The Business Owner Strategy

If you own a business with partners, insurance is often used to fund “buy-sell” agreements. If one partner dies, the insurance payout allows the other partner to buy out the deceased partner’s family. In this case, a whole life policy is often preferred because business partnerships don’t have a “term” or expiration date; you need the money to be there whenever the event happens.

Final Thoughts

When you strip away the sales pitches and the complex jargon, the decision comes down to one question: are you trying to protect a temporary need or build a permanent asset? For the vast majority of people reading this in 2026, term life insurance is the smarter, more efficient choice. It gives you the massive protection you need while you are building your life, without locking you into high monthly payments that might become a burden later. It respects your ability to invest your own money and gives you the freedom to change your mind as your life evolves.

That said, whole life insurance isn’t a bad product; it is just a specialized one. If you have already maxed out your retirement accounts, paid off your debts, and are looking for a tax-advantaged place to store wealth for the next generation, it can be a powerful part of a larger plan. The most important thing is that you don’t stay in a state of “analysis paralysis.” Every day you wait to get covered is a day you are taking a massive risk with your family’s future. Whether you choose term vs whole life insurance, the goal is to get a policy in place today so you can stop worrying about the “what ifs” and start focusing on the “what’s next.”

Frequently Asked Questions (FAQs) Term vs Whole Life Insurance

What happens if I outlive my term life insurance policy?

Actually, if you outlive the policy, it simply expires. You don’t get a payout, and you don’t get your money back. While this feels like a “loss,” it is actually the best-case scenario because it means you lived a long, healthy life. Most people find that by the time the policy expires, they have enough savings that they no longer need insurance.

Can I change my mind and switch from term to whole life?

Yes, most modern term policies are “convertible.” This is a huge advantage because it allows you to start with a cheap term policy while you are young and then flip it into a permanent whole life policy later in life without having to take another medical exam. This is a great way to “lock in” your insurability while you are healthy.

Yes, almost all life insurance policies cover death by suicide, but only after a “suicide clause” period has passed. This is typically two years from the date the policy starts. If the event happens within the first two years, the company usually only refunds the premiums paid. After two years, it is treated like any other cause of death.

Is the cash value in whole life insurance accessible during an emergency?

You can access it, but it isn’t like a regular savings account. You usually have to take out a “policy loan.” The insurance company will charge you interest on your own money, and if you don’t pay it back, that amount is deducted from the final death benefit that goes to your family. It is a good safety net, but it has strings attached.

Why is term insurance so much cheaper than whole life?

The math is simple: the insurance company is betting that you won’t die during the term. With whole life, they know for a fact they will have to pay out eventually because everyone dies. Since a payout is guaranteed with whole life, they have to charge you enough to build up that massive pool of money over time.

How much life insurance do I really need in 2026?

A common rule of thumb is to aim for 10 to 12 times your annual salary. If you make $70,000 a year, you should look for around $700,000 to $850,000 in coverage. This ensures your family can invest the payout and live off the interest while they figure out their next steps.

{kind=link}