Health insurance networks are not just random lists of doctors thrown together on a website. They are strict financial agreements between huge insurance companies and local healthcare providers. When a doctor, hospital, or lab joins a network, they sign a contract agreeing to charge a specific, heavily discounted rate for their services.

In exchange for lowering their prices, the insurance company sends a steady stream of patients their way. This is exactly why staying “in-network” is so important for your personal bank account. The insurance company penalizes you for going outside this predefined circle of doctors because it costs them more money. The type of network you choose—whether it is an HMO, PPO, or EPO—determines how much freedom you actually have to step outside that circle. It also dictates how much financial punishment you will take if you decide to break the rules and see an out-of-network specialist. Understanding this core concept is the first step in decoding the complex world of American healthcare.

|

Network Feature |

What It Means for You |

Real-World Impact |

|

Network Purpose |

To lower costs through negotiated provider rates. |

Keeps your monthly premiums from skyrocketing. |

|

In-Network |

Providers who signed a contract with your insurance. |

You pay the lowest possible copays and deductibles. |

|

Out-of-Network |

Providers with zero ties to your insurance company. |

You pay the highest rates, or potentially the entire bill. |

|

Network Scope |

The physical size and location of the covered doctors. |

Determines if you have coverage when traveling out of state. |

What is an HMO Health Maintenance Organization?

An HMO is easily the most strict and highly structured type of health insurance on the market. It stands for Health Maintenance Organization, and its primary mission is to keep medical costs as low as possible by tightly coordinating every piece of your care through one central person. When you sign up for an HMO, you are strictly required to pick a Primary Care Physician, commonly known as a PCP. This specific doctor becomes your medical gatekeeper and your main point of contact for absolutely everything from a routine flu shot to unexplained joint pain.

If you want or need to see anyone else in the medical field, your PCP has to give you official permission first. You cannot bypass them. The insurance company uses this gatekeeper method to prevent patients from ordering unnecessary tests or seeing expensive specialists for minor issues. If you break this rule and see a specialist without a referral, the HMO will completely deny your claim, leaving you on the hook for the entire medical bill.

How an HMO Works in the Real World?

Let’s say you wake up on a Tuesday with a strange, persistent rash on your arm that won’t go away. Under an HMO plan, you cannot simply look up a local dermatologist and book an appointment for the next day. Instead, you have to call your Primary Care Physician and schedule an evaluation. You go in, pay your copay, and let the PCP examine the rash.

If the PCP decides it is beyond their expertise, they will write a formal referral to an in-network dermatologist. You then have to wait for the HMO to process and approve that referral. Once approved, you can finally book your appointment with the skin doctor. This multi-step process effectively prevents you from making rash medical decisions, but it undeniably slows down your access to specialized care.

The Pros and Cons of an HMO Plan

The absolute biggest advantage of an HMO is the predictable, low price tag attached to it. Because the insurance company controls your care so tightly, they reward you with the lowest monthly premiums and incredibly low, flat-rate copays for your office visits. You also benefit from having one doctor who intimately knows your entire medical history.

On the flip side, the lack of freedom is a massive headache for many people. You are essentially trapped inside a local, geographic bubble. If you travel frequently for work or decide you want a second opinion from a famous doctor two states over, your HMO will not pay a single cent. It offers zero out-of-network coverage unless you are dying in an emergency room.

|

HMO Factor |

Detail and Explanation |

Impact on Your Care |

|

Monthly Cost |

Usually the cheapest option available. |

Great for tight household budgets. |

|

PCP Required |

Yes, you must assign a primary gatekeeper. |

One doctor manages all your records. |

|

Referrals |

Mandatory for every single specialist visit. |

Slows down access to specialized treatment. |

|

Out-of-Network |

Absolutely no coverage provided. |

You pay 100% of the bill if you break the rules. |

What is a PPO Preferred Provider Organization?

A PPO, or Preferred Provider Organization, is built from the ground up for people who demand total control over their healthcare. It is widely considered the “VIP” version of health insurance because it removes almost all the annoying roadblocks. First and foremost, you do not ever have to pick a primary care doctor to act as your gatekeeper. Second, you never need to ask an insurance company for a referral to see a specialist.

If you feel like something is wrong with your heart, you can simply find a cardiologist and book the appointment yourself. PPOs also feature massive, often nationwide networks of doctors and hospitals. Even better, if you decide to see a doctor who is completely outside of that massive network, the PPO will still step in and cover a portion of your medical bill. You pay a heavy premium for this luxury, but for many, the freedom is worth every penny.

How a PPO Works in the Real World?

Imagine you are on a family vacation three states away from home and you suddenly develop a severe ear infection. With a PPO, you do not have to panic or call a doctor back home for permission to get treated. You can simply open your phone, look up an urgent care clinic or an ear, nose, and throat specialist in your current city, and walk right in. If that doctor happens to be in your PPO’s “preferred” network, you just pay your standard, negotiated rate.

Even if that doctor has absolutely no relationship with your insurance company, you can still get treated. You will likely have to pay a higher percentage of the total bill—known as coinsurance—but you are not left paying the entire thousands-of-dollars invoice by yourself. You manage your own health timeline without anyone looking over your shoulder.

The Pros and Cons of a PPO Plan

The main selling point of a PPO is the absolute freedom to see any licensed medical professional you want, whenever you want. You get to skip the annoying gatekeeper routine and aggressively manage your own health issues. PPOs are also a lifesaver for people who travel constantly, as the out-of-network benefits act as a safety net anywhere in the country. However, this flexibility comes with brutal financial downsides.

PPOs feature the highest monthly premiums on the open market, meaning a chunk of your paycheck disappears before you even get sick. They also usually saddle you with higher annual deductibles. Finally, because there is no central doctor managing your care, you have to do the legwork to ensure your medical records actually get sent from one specialist to another.

|

PPO Factor |

Detail and Explanation |

Impact on Your Care |

|

Monthly Cost |

The most expensive health plan option. |

Takes a larger bite out of your monthly income. |

|

PCP Required |

No primary doctor is ever required. |

You direct your own health journey. |

|

Referrals |

Never needed to see any specialist. |

Fast, immediate access to experts. |

|

Out-of-Network |

Partial coverage is guaranteed. |

Safe to travel and seek second opinions. |

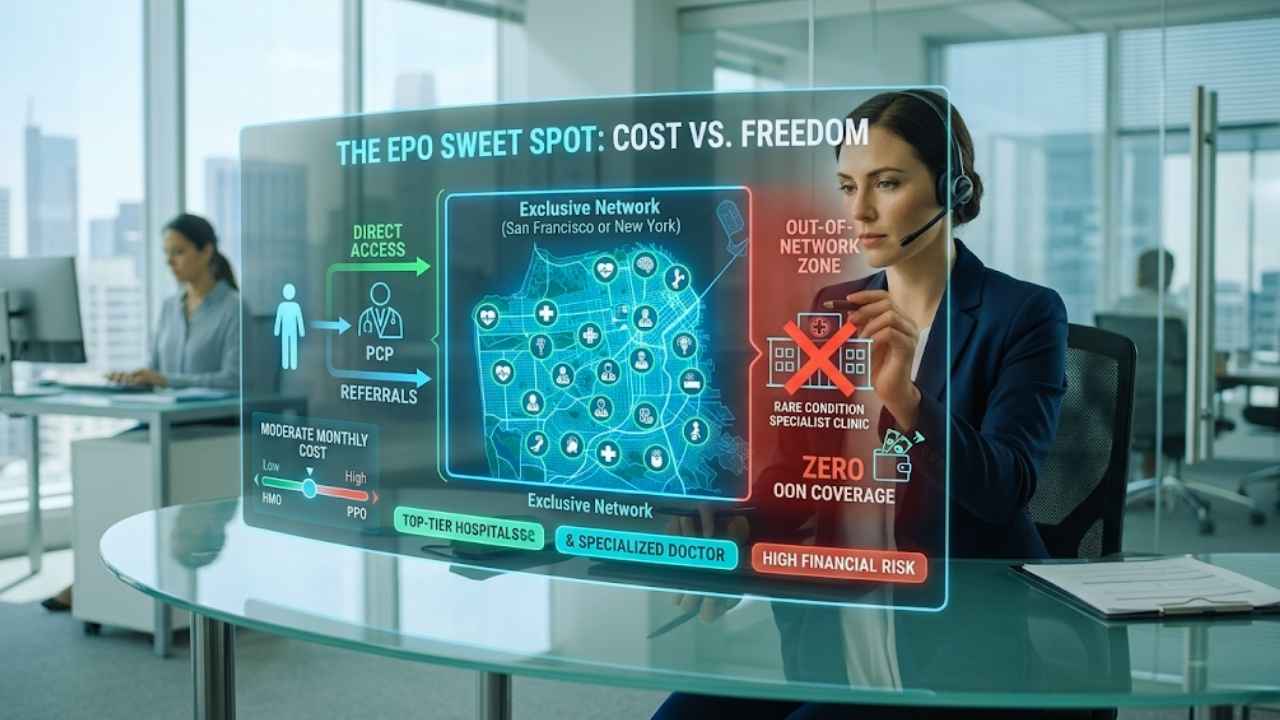

What is an EPO Exclusive Provider Organization?

An EPO, or Exclusive Provider Organization, is essentially the modern middle child of the health insurance world. It was specifically designed by insurance companies to bridge the massive gap between the cheap, restrictive HMO and the expensive, flexible PPO. An EPO steals the best feature from the PPO: it completely eliminates the need for referrals. You do not have to pick a primary care doctor, and you do not need anyone’s permission to book a specialist.

However, to keep the costs down, it steals the strictest rule from the HMO: it enforces a rock-solid, exclusive network. If you go outside of the EPO’s designated network for anything other than a life-or-death emergency, the insurance company will completely deny the claim. It is a plan built for speed and convenience, but it requires you to be incredibly disciplined about checking network directories before you agree to any medical services.

How an EPO Works in the Real World?

Let’s say you tweak your knee while playing basketball on the weekend. With an EPO, you completely bypass the annoying step of visiting a primary care doctor just to get a piece of paper. You immediately start searching for orthopedic sports medicine specialists. The catch is, you have to log onto your insurance company’s specific portal and make absolutely sure the doctor you want is listed as “in-network” for your exact EPO plan.

Once you verify their status, you call their office, book the appointment, and go. It saves you days of waiting and the cost of an extra doctor’s visit. But if you get sloppy, assume a doctor is in-network, and guess wrong, your EPO plan will leave you holding a massive bill for the consultation, the X-rays, and any treatments you received.

The Pros and Cons of an EPO Plan

EPOs are fantastic because they hit the financial sweet spot. They are noticeably cheaper per month than a PPO, but they offer vastly more day-to-day freedom than an HMO. They are the perfect fit for people living in large metropolitan areas where the “exclusive” network actually includes dozens of top-tier hospitals and hundreds of specialists.

The glaring downside is the absolute lack of an out-of-network safety net. If you develop a rare condition and the only expert who can treat it is out-of-network, your EPO will not help you pay for it. The network boundaries are entirely rigid, and the financial penalty for crossing them accidentally is severe.

|

EPO Factor |

Detail and Explanation |

Impact on Your Care |

|

Monthly Cost |

Moderate pricing, right in the middle. |

Balances budget with flexibility. |

|

PCP Required |

No, you can skip the general doctor. |

Saves time and copay money. |

|

Referrals |

Not required for any specialist visit. |

Direct access to the care you need. |

|

Out-of-Network |

Zero coverage, totally strict network. |

High financial risk if you make a booking mistake. |

Key Differences Between HMO PPO and EPO Plans

When you stack up HMO vs PPO vs EPO side by side, the core differences always boil down to two main things: how much money you want to spend upfront, and how much administrative hassle you are willing to tolerate. The insurance industry operates on a simple scale of risk. When they have control over where you go (HMO), their risk is low, so your price is low.

When you have the power to go wherever you want (PPO), their risk is high, so they charge you a massive premium to cover their potential losses. The EPO just tries to slice that risk right down the middle. You have to look at your own personality to decide which of these structures actually makes sense for your daily life.

Comparing Costs Premiums and Deductibles

In the world of health insurance, your monthly premium is basically the subscription fee you pay just to have the card in your wallet. HMO premiums are the lowest because the insurance company uses the primary care doctor to block expensive, unnecessary care. PPO premiums are the highest because the insurance company has absolutely zero control over your healthcare spending habits.

EPOs slide right into the middle slot. Beyond the premium, you have to evaluate the deductible—the raw amount of cash you have to burn through before the insurance actually starts helping. PPOs almost always saddle you with much higher deductibles than HMOs, meaning you have to spend thousands out of pocket at the start of the year before the “good” coverage kicks in.

Comparing Flexibility and Network Size

If you value freedom above all else, the PPO network size will blow the others out of the water. PPOs partner with massive, national networks, ensuring you can find an in-network provider in almost any state. HMOs are incredibly localized. If you live in a rural county, your HMO network might literally only consist of one hospital and a handful of local clinics.

EPO networks vary wildly depending on the insurance carrier. In big cities, an EPO network might be huge and robust, giving you plenty of options without ever feeling trapped. But in smaller towns, an EPO can feel just as suffocating as an HMO, but without the benefit of a primary doctor to help guide you through it.

|

Feature Comparison |

HMO |

PPO |

EPO |

|

Upfront Premium |

Lowest |

Highest |

Mid-range |

|

Annual Deductible |

Typically very low |

Typically high |

Mid-range |

|

Specialist Access |

Blocked by a gatekeeper |

Totally unrestricted |

Totally unrestricted |

|

Geographic Reach |

Usually highly local |

Often nationwide |

Usually regional/local |

How to Choose Between HMO vs PPO vs EPO?

There is no magical “best” plan hidden among these options. The smartest choice depends entirely on your current physical health, your bank account balance, and your tolerance for annoying paperwork. Choosing the wrong plan can either drain your savings through high premiums you didn’t need, or bankrupt you with out-of-network bills you weren’t expecting. You need to sit down, look at how many times you actually went to the doctor last year, and make a logical choice based on hard data rather than just guessing.

When to Choose an HMO?

You should absolutely choose an HMO if keeping your monthly household expenses down is your number one priority. It is the perfect plan for a young, generally healthy person who only needs to see a doctor once a year for a routine checkup and maybe a flu shot. You won’t feel the restrictions of the network because you simply don’t use the medical system enough to care.

An HMO is also a surprisingly great choice if you already have a primary care doctor you trust with your life, and that doctor happens to be the centerpiece of the local HMO network. You get to keep your favorite doctor while paying the lowest possible price.

When to Choose a PPO?

You should bite the bullet and pay for a PPO if you have a complex medical history that requires constant monitoring by several different specialists. If you are battling a chronic illness, the absolute last thing you want to deal with is fighting an insurance company for a new referral every single month.

It is also the only logical choice if your job requires you to travel across the country frequently, as the out-of-network coverage ensures you are protected no matter what state you are in. If you have the financial breathing room to afford the higher premiums and deductibles, the sheer peace of mind a PPO provides is unmatched.

When to Choose an EPO?

You should lock in an EPO if you are deeply frustrated by the slow, clunky referral process of an HMO but you simply cannot afford the luxury price tag of a PPO. It is the ultimate compromise plan. It works beautifully if you live in a dense, urban environment where the in-network hospital systems are massive and filled with top-tier specialists.

However, you must be a highly organized person to make an EPO work. If you are the type of person who forgets to check network directories or blindly trusts that every doctor in a building takes your insurance, an EPO will eventually burn you with a massive denied claim.

|

Your Profile |

Best Plan Fit |

Why It Works For You |

|

Healthy & Budget-Focused |

HMO |

Lowest premiums, you rarely need specialists anyway. |

|

Chronic Illness / High Usage |

PPO |

No referrals needed, easy access to multiple experts. |

|

Frequent Traveler |

PPO |

National networks and out-of-network safety nets. |

|

City Dweller wanting Speed |

EPO |

Fast specialist access without the massive PPO price tag. |

The Role of High Deductible Health Plans and HSAs

As you scroll through your enrollment options, you will inevitably see the acronym HDHP, which stands for High Deductible Health Plan. It is vital to understand that an HDHP is not a network type like an HMO or PPO; it is simply a financial structure overlaid on top of them. You can easily buy an HMO that is also an HDHP, or a PPO that is an HDHP.

These plans slash your monthly premium to the absolute bone, but they require you to pay thousands of dollars entirely out of your own pocket before the insurance company pays a dime for anything other than basic preventative care. Insurance companies offer these plans to shift the upfront financial risk entirely onto your shoulders.

The single biggest reason people choose an HDHP is because it legally qualifies you to open a Health Savings Account, or HSA. An HSA is essentially a secret weapon for personal finance. It is a special bank account where you can deposit money completely tax-free, let it grow tax-free, and spend it tax-free as long as you use it for qualified medical expenses.

Unlike other flexible spending accounts, the money in an HSA rolls over every single year and stays with you even if you quit your job or change insurance plans. If you are relatively healthy, pairing an EPO or PPO with an HSA allows you to build a massive, tax-sheltered safety net for future healthcare costs while keeping your current monthly bills as low as possible.

|

Feature Comparison |

High Deductible (HDHP) |

Traditional Copay Plan |

|

Monthly Premium |

Dirt cheap |

Noticeably more expensive |

|

Annual Deductible |

Extremely high ($3,000+) |

Usually lower ($500 – $1,500) |

|

HSA Eligible |

Yes, you can open the tax-free account |

No, legally restricted from HSA use |

|

Best Used For |

Healthy people building long-term savings |

People who visit the doctor constantly |

Final Thoughts

There is no universal winner in the ongoing debate of HMO vs PPO vs EPO. Surviving open enrollment is entirely about being brutally honest with yourself about your health and your wallet. If you want a hands-off, low-cost experience where someone else handles the logistics, the HMO remains a bulletproof choice. If you refuse to be told what to do and want the freedom to chase down the best specialists in the country, you have to open your checkbook and buy the PPO.

If you want a modern, streamlined experience that cuts out the gatekeeper but still respects a budget, the EPO is a fantastic middle ground. Take a hard look at your medical bills from last year, check to see which networks your favorite doctors actually belong to, and choose the plan that gives you the peace of mind you deserve.

Frequently Asked Questions FAQs About Health Insurance Networks

1. Can I switch from an HMO to a PPO mid year?

Generally, you cannot. You have to wait for open enrollment. The only exception is if you have a life event like getting married, losing your job, or having a child. These are called Qualifying Life Events and they open a special 60-day window for you to change your plan type.

2. What happens if I have an emergency out of network with an HMO or EPO?

Do not worry about the network in a real emergency. Under the No Surprises Act, insurance companies must cover emergency services at in-network rates, even if the hospital is out of network. If you are having a heart attack, go to the nearest ER. The insurance company cannot charge you extra just because the hospital was not on their list.

3. Why are PPO plans more expensive?

PPOs are expensive because they offer more. The insurance company has to pay out more money when you see out-of-network doctors. Since they cannot control which doctors you see or how often you see specialists, they charge a higher monthly fee to cover that extra risk and lack of coordination.

4. Do all doctors accept PPO insurance?

Not necessarily. While PPOs let you go out of network, a doctor can choose not to accept any insurance at all. Always call the doctor’s office and ask, “Are you in-network with my specific PPO plan?” rather than just asking if they “take” your insurance.

{kind=link}