The standard advice for your career usually looks like a long marathon. You spend your twenties finding your footing, your thirties and forties climbing the ladder, and your fifties counting down the days. By the time you reach 65, you finally get the keys to your own life. But a growing group of people is decided that waiting four decades is a bad deal.

They are following a different path known as Financial Independence Retire Early (FIRE). This is not just a trend for tech bros in Silicon Valley anymore. It has become a global lifestyle shift focused on reclaiming time while you are still young enough to enjoy it.

Financial Independence Retire Early (FIRE) is about aggressively cutting costs and boosting income to invest as much as possible. The goal is to build a portfolio that pays for your life so you never have to work for a paycheck again. It is a radical departure from consumer culture, where the goal is often to buy a bigger house or a flashier car every time you get a raise. In the FIRE community, a raise is simply more fuel for your freedom fund. This guide will walk through the mechanics, the different styles of the movement, and the gritty reality of what it takes to actually quit the rat race early.

What is the FIRE Movement?

The movement started as a whisper on internet forums and personal blogs where people shared their spreadsheets and frugal tips. It eventually exploded into a mainstream philosophy that challenges everything we know about work and leisure. At its heart, it is about intentionality. Most people spend their money on things they do not need to impress people they do not like. Practitioners of the FIRE movement do the opposite. They prioritize long-term freedom over short-term status symbols, often living on 30% or 50% of their income to invest the rest.

The Core Philosophy

The main idea is that once your investments generate enough passive income to cover your living expenses, you are free. You do not have to stop working, but you do not have to work for money. This shift in perspective turns employment from a survival necessity into an optional activity. Many people who reach financial independence continue to work on passion projects, volunteer, or start small businesses because they want to, not because they have to pay the rent. It is about removing the “forced” part of labor and replacing it with total autonomy.

|

Feature |

Traditional Retirement |

FIRE Retirement |

|

Typical Age |

65 to 67 |

30 to 45 |

|

Savings Rate |

5% to 15% |

50% to 75% |

|

Primary Goal |

Post-work relaxation |

Lifelong time freedom |

|

Spending Habit |

Lifestyle inflation |

Aggressive frugality |

|

Work View |

A 40-year necessity |

A temporary tool for capital |

The Financial Independence Retire Early Math

To make early retirement work, you have to move past vague goals and get into the actual numbers. The movement is built on a mathematical foundation that tells you exactly when you can stop working. This is not about winning the lottery or inheriting wealth; it is about calculating your survival cost and multiplying it by a specific factor. Once you understand the math, the path to Financial Independence Retire Early becomes a predictable, though difficult, engineering problem. It removes the guesswork and gives you a clear finish line to aim for.

The Rule of 25

The most famous number in this community is the Rule of 25. To figure out how much you need to retire, you first need to know exactly how much you spend in a year. If you spend $50,000 annually, you multiply that by 25. The resulting $1.25 million is your target number. This calculation is based on the idea that a million-dollar-plus portfolio, invested in a mix of stocks and bonds, should be able to support you for the rest of your life. It is a simple way to visualize your goal without needing a degree in finance.

The 4% Withdrawal Rule

The 4% rule is the companion to the Rule of 25. It comes from a study that looked at historical market data to see how much a retiree could take out of their accounts without running out of money. The idea is that if you withdraw 4% of your total portfolio in the first year and adjust for inflation every year after, your money should last at least 30 years. For early retirees who might need their money to last 50 years, many now suggest a more conservative 3.5% withdrawal rate. This provides a safety net against market crashes or high inflation years that could otherwise drain your savings too quickly.

|

Annual Spending |

Nest Egg (4% Rule / 25x) |

Nest Egg (3.5% Rule / 28.5x) |

|

$30,000 |

$750,000 |

$857,000 |

|

$40,000 |

$1,000,000 |

$1,142,000 |

|

$60,000 |

$1,500,000 |

$1,714,000 |

|

$80,000 |

$2,000,000 |

$2,285,000 |

|

$100,000 |

$2,500,000 |

$2,857,000 |

Choosing Your Path: The Different FIRE Variations

Not everyone wants to live in a van and eat beans and rice to retire early. As the movement has grown, it has branched out into different styles that fit different lifestyles and income levels. Some people want to retire with a million dollars, while others want five million. To achieve Financial Independence Retire Early, you first have to decide what kind of life you want to live after you quit. This flexibility is what has allowed the movement to stay relevant across different age groups and economic backgrounds.

Lean FIRE

This is the minimalist version of the movement. Lean practitioners aim for a very low cost of living, usually under $40,000 a year. They often use geo-arbitrage, moving to cheaper states or even different countries to make their money go further. It is the fastest way to retire because the target number is much lower. If you can live happily on $30,000 a year, you only need $750,000 to be free. It requires a high level of discipline and a genuine love for a simple, non-materialistic life.

Fat FIRE

Fat FIRE is for the high earners who want a “traditional” upper-middle-class lifestyle in retirement. They do not want to worry about the price of a steak dinner or a trip to Europe. Their annual budgets are usually $100,000 or more. This requires a much larger portfolio, often between $2.5 million and $5 million. Because the goal is so high, people on this path usually have very high salaries in fields like tech, medicine, or law. They still save aggressively, but their end goal is a life of abundance rather than just survival.

Barista FIRE

This is a great middle ground for people who are tired of the corporate grind but are not ready to stop working entirely. In this scenario, you save enough so that your investments cover your big bills, like housing and utilities. You then quit your high-stress job and take a part-time job—perhaps at a coffee shop—to cover your daily fun money and, most importantly, to get health insurance. It allows you to “retire” from the 60-hour work week much sooner while keeping a small, manageable stream of income.

Coast FIRE

Coast FIRE is all about the power of compound interest. In this version, you work extremely hard in your 20s and early 30s to front-load your retirement accounts. Once you hit a certain number, you stop contributing to those accounts entirely. You let the money sit and grow for the next 20 or 30 years until you reach traditional retirement age. This means you only have to earn enough to cover your current living expenses today. You do not have to save another dime for the future because your “past self” already took care of it.

|

Type |

Lifestyle Level |

Target Portfolio |

Strategy Focus |

|

Lean |

Minimalist/Frugal |

< $1 Million |

Cutting expenses to the bone |

|

Fat |

Luxury/Comfortable |

> $2.5 Million |

High income and high investment |

|

Barista |

Semi-retired |

$500k – $1M |

Part-time work for benefits |

|

Coast |

Front-loaded |

Varies by age |

Early aggressive investing |

Practical Strategies for Wealth Accumulation

You cannot just wish your way into early retirement; you have to build a machine that makes it happen. The accumulation phase is the “boring middle” where you spend years repeating the same smart habits. To find success with Financial Independence Retire Early, you need to master a few specific skills. It is a combination of defense (spending less) and offense (earning more). When these two forces work together, the timeline to retirement shrinks rapidly. Most people focus on just one, but the real magic happens when you do both.

Optimizing the Savings Rate

The most important lever you can pull is your savings rate. If you save 10% of your income, it takes about 51 years to retire. If you save 50%, it takes about 17 years. This is because every dollar you save is a dollar you do not need to replace with passive income later. People in the movement look for “leaks” in their budget, such as unused subscriptions, expensive dining habits, or high-interest debt. By plugging these leaks and redirecting the cash to investments, they accelerate their journey.

Passive Investing in Index Funds

The FIRE community typically avoids “get rich quick” schemes or day trading. Instead, they favor low-cost, broad-market index funds. These funds allow you to own a piece of almost every major company in the stock market. Over long periods, the market has historically returned about 7% to 10% annually. By keeping fees low and staying invested through market ups and downs, your wealth snowballs. You do not need to be a financial genius to win; you just need to be patient and consistent.

Strategic Frugality

Frugality in the FIRE movement is not about being cheap; it is about value. It means spending money on things that actually improve your life and cutting everything else. This often involves “house hacking,” where you live in one part of a property and rent out the rest to cover your mortgage. It might mean buying a reliable three-year-old car instead of a brand-new one to avoid the massive initial depreciation. These strategic choices save thousands of dollars a year without significantly lowering your quality of life.

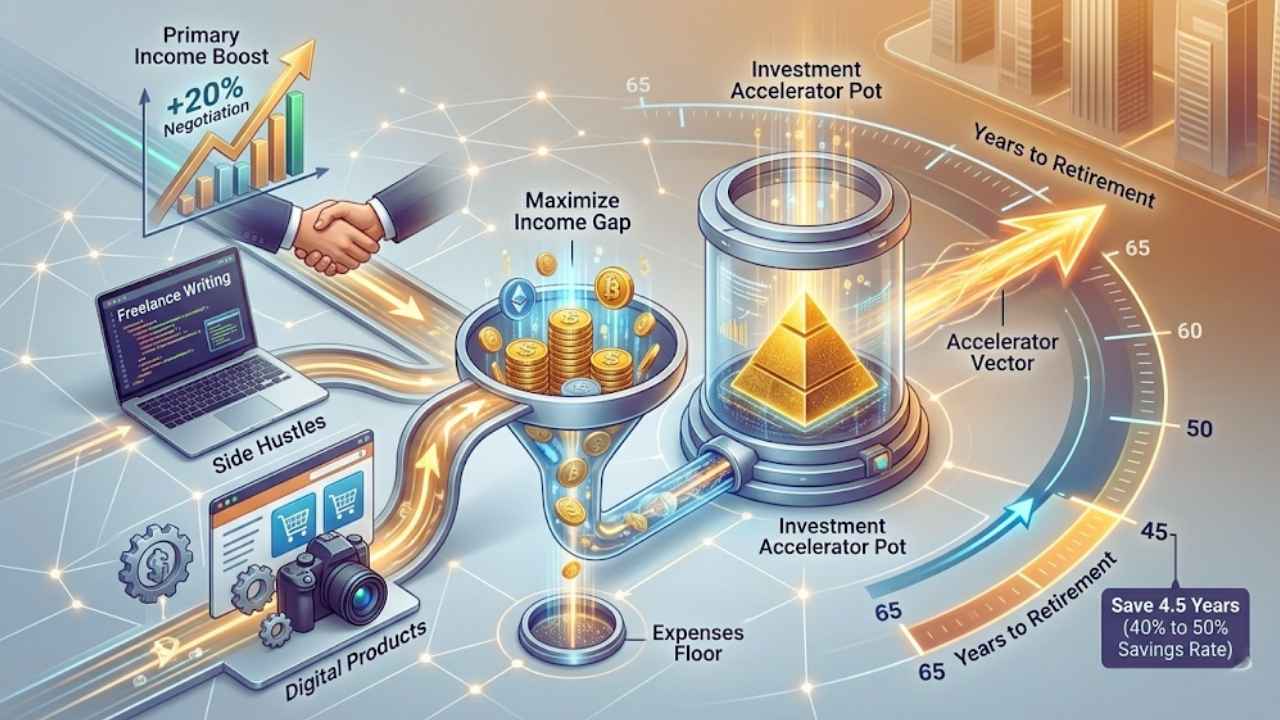

Income Generation and Side Hustles

While cutting expenses has a floor, your income has no ceiling. Many people in the community use side hustles to speed up their progress. Whether it is freelance writing, consulting, or selling digital products, that extra income goes straight into the investment pot. Increasing your primary salary is also key. Regularly negotiating raises or switching companies for a 20% bump can shave years off your working career. The goal is to maximize the gap between what you earn and what you spend.

|

Current Savings Rate |

New Savings Rate |

Years Saved to Retirement |

|

10% |

20% |

14 Years |

|

20% |

30% |

9 Years |

|

30% |

40% |

6 Years |

|

40% |

50% |

4.5 Years |

|

50% |

60% |

3.5 Years |

The Real Risks and Potential Rewards

Any strategy that promises to let you quit work 30 years early comes with risks. It is not all sunshine and tropical beaches. You have to be aware of the pitfalls that could send you back to a cubicle when you are 60. Financial Independence Retire Early is a long-term bet on yourself and the economy. While the rewards are massive—total control over your life—the risks are real and require careful planning to mitigate. You have to be prepared for the worst-case scenario while hoping for the best.

Sequence of Returns Risk

This is the biggest technical threat to an early retiree. It refers to the danger of the stock market crashing right after you retire. If you start withdrawing money from a shrinking portfolio, it might never recover. To fight this, many retirees keep one or two years of cash in a high-yield savings account. This “cash cushion” allows them to live without selling their stocks when the market is down, giving their portfolio time to bounce back.

The Inflation Factor

Inflation is the silent killer of purchasing power. If your expenses double over twenty years but your investment income stays the same, you are in trouble. This is why most FIRE math includes an inflation adjustment. It is also why many practitioners keep a high percentage of their wealth in stocks rather than bonds or cash, as stocks have historically been a better hedge against rising prices. You have to ensure your “future dollars” can actually buy the same amount of groceries and fuel as your “today dollars.”

Health Insurance Strategies

In places like the United States, healthcare is the “X-factor” that keeps people in their jobs. Without an employer-sponsored plan, insurance can cost thousands of dollars a month. Early retirees often use the Affordable Care Act (ACA) and try to keep their taxable income in a range that qualifies them for subsidies. Others use health share ministries or look for part-time “Barista” jobs that offer benefits. It is a complex puzzle that requires constant attention as laws and prices change.

|

Pro |

Con |

|

Complete Time Freedom |

Market Volatility Risks |

|

Reduced Stress |

Social Isolation from Working Peers |

|

Ability to Pursue Passions |

High Cost of Private Healthcare |

|

Financial Security |

Risk of Outliving Your Money |

|

Ownership of Your Schedule |

Potential Loss of Professional Identity |

Making it Work in the Modern Economy

The world has changed since the early days of the FIRE blogs. Housing is more expensive, and inflation has been volatile. However, the modern economy also offers tools that make Financial Independence Retire Early more achievable than ever. Remote work, the gig economy, and easy access to global markets have changed the game. You no longer have to live in an expensive city to earn a high wage, which is a massive advantage for anyone trying to save a large portion of their income.

Dealing with High Cost of Living

If you live in a city where a small apartment costs $3,000 a month, reaching your goal will be a slow climb. Many in the community choose to “geo-arbitrage.” This means earning a high salary in a tech hub or through a remote job and then living in a much cheaper area. By moving from New York to a mid-sized city in the Midwest or even to a digital nomad hub in Portugal or Southeast Asia, you can effectively double or triple your savings rate overnight.

Mental Preparation for Early Retirement

Most people spend so much time focusing on the money that they forget to plan for the time. Quitting your job creates a massive void in your daily schedule. Without a plan for how to spend those 40+ hours, many retirees face depression or a sense of worthlessness. It is important to build hobbies, community connections, and passion projects while you are still working. You want to retire to something, not just from something. Mental health is just as important as the size of your bank account.

|

Region |

Cost of Living Index |

Healthcare Access |

Lifestyle Vibe |

|

Southeast Asia |

Very Low |

Moderate |

Tropical / Adventurous |

|

Southern Europe |

Moderate |

High |

Relaxed / Cultural |

|

US Midwest |

Low |

High |

Family-oriented / Stable |

|

Latin America |

Low |

Moderate |

Vibrant / Diverse |

|

Eastern Europe |

Low |

Moderate |

Historic / Developing |

Final Thoughts

The path to Financial Independence Retire Early is not a sprint; it is a long-distance hike that requires a sturdy pair of boots and a lot of patience. It is not about becoming a miser or hating your job. It is about realizing that your time is the most valuable currency you have, and you should not spend it all working for someone else’s dream. Whether you want to quit work entirely at 35 or just want the peace of mind that comes with a “f-you fund,” the principles of the FIRE movement can help you get there.

You do not have to follow every rule perfectly. Even if you only get halfway to your goal, you will be in a much better position than the average person. Having a few hundred thousand dollars in the bank gives you options that most people do not have. You can say no to a toxic boss, take a six-month sabbatical, or start that business you have always dreamed of. Ultimately, Financial Independence Retire Early is about freedom. It is about making sure that the best years of your life belong to you, not your employer.

Frequently Asked Questions (FAQs) About Fire Movement Explained

Can I achieve FIRE if I have children?

Yes, but the math changes. You will need a larger “Fat FIRE” style nest egg to cover education, extra healthcare, and larger housing. Many people with kids reach financial independence by focusing on “house hacking” or moving to areas with excellent but affordable public schools.

What is the “One More Year” syndrome?

This is a psychological trap where someone has reached their retirement number but is too afraid to quit. They keep saying, ~I will just work one more year to be safe~. It often stems from a fear of market crashes or a loss of identity without a job title.

Is the FIRE movement just for high earners?

While a high income makes it faster, many people with average salaries achieve it through extreme frugality and Coast FIRE strategies. It is about the gap between your income and expenses, not just the raw salary number.

What happens if the stock market crashes right after I retire?

This is why having a “cash bucket” or “bond tent” is vital. By having 2-3 years of living expenses in cash or low-risk assets, you can avoid selling your stocks during a downturn, allowing your portfolio to recover without being depleted.

Do I have to pay taxes on my withdrawals?

Yes, but early retirees often pay very little. By strategically withdrawing from a mix of taxable accounts, Roth IRAs, and traditional 401ks, many can keep their taxable income low enough to stay in the 0% or 10% tax brackets.

{kind=link}