Sitting down to buy life insurance is rarely a fun experience. You are forced to confront your own mortality while simultaneously trying to solve a massive financial puzzle that affects your family. When you finally reach the part of the application that asks for your desired coverage amount, a feeling of uncertainty usually sets in.

If you find yourself asking, how much life insurance do I need, you are definitely not alone in this confusion. Should you get five hundred thousand, a million, or two million dollars in coverage to feel safe? Without a solid framework, these numbers feel like abstractions floating in the air. Many people end up throwing a dart at a dartboard when picking their policy limits. They might pick a round number that sounds impressive, or they might just accept whatever standard policy their employer offers at work. Others let an insurance agent dictate the number based on the maximum premium they can afford every month without stretching their budget. All of these approaches are deeply flawed because they ignore your unique financial reality and your dependents actual needs.

Life insurance is not a guessing game, and it is not a luxury purchase where you simply buy as much as you can afford right now. It is a precise mathematical tool designed to solve a very specific problem. It replaces the economic value you bring to your family if you were to pass away prematurely. To find the right number, you do not need a crystal ball or advanced calculus. You just need basic math, a clear understanding of your household expenses, and a realistic look at your family future needs over the next few decades.

Why Guessing Your Life Insurance Coverage Is a Costly Mistake

When you guess your coverage amount, you are almost guaranteed to miss the mark entirely. You will likely end up either underinsured or overinsured, and both scenarios carry significant financial consequences for your family. Relying on gut feelings or arbitrary rules of thumb can undermine the entire purpose of getting insured in the first place. You want to provide a financial safety net, but guessing creates massive holes in that net. You must anchor your policy size to your actual liabilities and the standard of living you want your loved ones to maintain. Guessing leaves too much room for emotional bias and mathematical errors.

The Dangers of Underinsurance

Underinsurance is the most common mistake people make when they try to answer the question of how much life insurance do I need. It happens when you buy a policy that feels large on paper but fails to hold up against the crushing weight of real world expenses. A policy worth two hundred and fifty thousand dollars might sound like a windfall today. However, if you have a massive mortgage, a car loan, and two children heading to college in a decade, that money will evaporate in a matter of a few short years.

If you guess too low, you are leaving your family to face a financial cliff right in the middle of their grieving process. A surviving spouse might be forced to sell the family home because they can no longer afford the monthly mortgage payments on a single income. They might have to uproot the children from their current school district or abandon carefully laid plans for university education entirely.

The daily stress of paying for groceries, utilities, and healthcare can compound the emotional trauma of losing a partner or a parent. Underinsurance defeats the core purpose of a policy, which is to provide absolute financial stability when the worst happens. You owe it to your dependents to run the real numbers instead of hoping for the best.

|

Expense Type |

Cost Example |

Time to Deplete a Small Policy |

|

Mortgage Balance |

Three hundred thousand dollars |

Instant depletion upon payoff |

|

Child Education |

One hundred thousand dollars per child |

Depleted within four years of college |

|

Daily Living |

Fifty thousand dollars annually |

Depleted in five years without other income |

The Hidden Cost of Overinsurance

On the other end of the spectrum is overinsurance, which is a mistake that drains your current bank account. This occurs when you panic and buy an excessively large policy, far beyond what your dependents would actually need to sustain their lifestyle. While having too much money might not sound like a problem for your beneficiaries, it represents a massive problem for you while you are still alive.

Life insurance premiums cost money every single month. Every single dollar you spend on unnecessary coverage is a dollar you are not putting into your retirement accounts, your emergency fund, or your children college savings plans. If you are paying two hundred dollars a month for a three million dollar policy when a one million dollar policy would have perfectly covered your family needs for fifty dollars a month, you are wasting one hundred and fifty dollars every thirty days.

Over the course of a twenty year term, that wasted money, if invested in a basic index fund, could have grown into a substantial piece of your retirement nest egg. Overinsurance drains your current wealth to protect against a risk level that simply does not exist in reality. You must find the exact mathematical middle ground.

|

Coverage Amount |

Monthly Premium Impact |

Wasted Investment Potential |

|

Right Sized Policy |

Fifty dollars |

Zero dollars wasted |

|

Slightly Overinsured |

One hundred dollars |

Thousands lost over twenty years |

|

Massively Overinsured |

Two hundred dollars |

Tens of thousands lost over twenty years |

The Fundamental Goal: What Is Life Insurance Actually For?

To calculate the right number, you must first understand the true utility of the product you are buying. Life insurance is fundamentally an instrument of risk management and financial continuity. It is designed to act as a financial bridge, carrying your dependents from the day of your passing to a future point where they are financially self sufficient. You are essentially buying time and stability for the people who rely on your paycheck every month. Without understanding this core purpose, doing the math will feel like a pointless exercise.

Income Replacement and Debt Clearance

For the vast majority of families, the primary goal is income replacement and immediate debt clearance. It is about making sure the promises you made to your family are kept, even in your physical absence. If you promised to pay off the house so your spouse could live mortgage free, life insurance provides the lump sum to clear that debt.

If you promised to send your kids to college, the death benefit steps in to fund those tuition bills without a hassle. It creates an immediate estate that replaces the paychecks you would have earned had you lived a long and healthy life. Understanding this goal makes the math much clearer, because you simply need to calculate the exact cost of those future promises.

You are looking at the exact dollar amounts required to keep the lights on, the fridge full, and the cars running. Once you define what you want the money to do, picking the final coverage number becomes a simple addition problem rather than a massive guessing game.

|

Core Goal |

Practical Application |

Example Outcome |

|

Income Replacement |

Substitutes your monthly paycheck |

Buys groceries and pays bills for ten years |

|

Debt Clearance |

Wipes out outstanding loans |

Pays off the remaining mortgage balance |

|

Future Funding |

Secures long term financial promises |

Covers university tuition for two children |

4 Real Math Methods to Calculate Your Life Insurance Needs

Financial advisors and actuaries use several different frameworks to determine the exact amount of coverage a person needs. Some are highly detailed, while others offer a quicker, broader perspective for those who hate spreadsheets. We will walk through the four most reliable mathematical methods, starting with the most accurate approach. You can pick the method that best aligns with your financial complexity and your willingness to crunch the numbers.

1. The DIME Method

The DIME method is widely considered the gold standard for calculating life insurance needs for the average family. It forces you to look at your actual financial footprint rather than relying on abstract multiples of your income. DIME is an acronym that stands for Debt, Income, Mortgage, and Education. By adding these four pillars together, you arrive at a highly accurate coverage number that reflects your reality.

Because it breaks down your life into four distinct categories, it prevents you from forgetting major expenses that could bankrupt your family later. It is highly recommended that you sit down with your partner and pull up your actual bank statements to run this method accurately.

|

DIME Pillar |

What It Covers |

How to Calculate |

|

Debt |

Credit cards and personal loans |

Add all non mortgage debt balances |

|

Income |

Daily living expenses |

Multiply salary by years needed |

|

Mortgage |

Housing stability |

Check current mortgage payoff amount |

|

Education |

College tuition for children |

Add one hundred thousand per child |

Debt and Final Expenses

The first letter focuses on clearing the financial slate immediately upon your passing. You need to calculate the total amount of all outstanding consumer debt you leave behind. This includes credit card balances, personal loans, auto loans, and any private student loans that are not automatically forgiven upon death. You do not want your surviving spouse inheriting a mountain of high interest debt without your income to help pay it off. Additionally, this category should include your estimated final expenses.

Funeral costs, burial or cremation fees, and end of life medical bills that your health insurance might not cover can easily run into the tens of thousands of dollars. A safe estimate to add to your debt total for these final expenses is roughly fifteen to twenty thousand dollars. Wiping out these immediate debts gives your family a clean slate to begin their recovery process without aggressive creditors calling them.

|

Debt Category |

Average Cost |

Why It Must Be Covered |

|

Consumer Debt |

Ten to twenty thousand dollars |

High interest rates drain savings quickly |

|

Auto Loans |

Thirty thousand dollars |

Ensures the family keeps their transportation |

|

Final Expenses |

Fifteen thousand dollars |

Prevents out of pocket costs for the funeral |

Income Replacement

This is usually the largest piece of the puzzle in the DIME calculation and requires the most thought. You need to determine how much of your annual income your family relies on, and how many years they will need that income to continue. A common approach is to multiply your current annual salary by the number of years until your youngest child graduates from high school or college.

For example, if you make eighty thousand dollars a year and your youngest child is currently eight years old, they have at least ten years until they turn eighteen. You would multiply eighty thousand by ten, resulting in eight hundred thousand dollars for income replacement. If you want to ensure your spouse is supported until they reach retirement age, you might need to stretch that multiplier even further. It is important to consider that a lump sum death benefit can be invested by your beneficiaries, and the interest earned can help combat inflation over those years.

|

Current Salary |

Years Until Youngest is 18 |

Total Income Replacement Needed |

|

Sixty thousand |

Ten years |

Six hundred thousand dollars |

|

Eighty thousand |

Fifteen years |

One point two million dollars |

|

One hundred thousand |

Twenty years |

Two million dollars |

Mortgage Balance

Housing is the largest single expense for most families across the globe. The goal here is to provide enough money to completely pay off the remaining balance of your mortgage. If your surviving spouse no longer has to worry about a monthly housing payment, their need for ongoing income replacement is drastically reduced. Look at your most recent mortgage statement and find the exact payoff amount.

If you currently owe three hundred and twenty thousand dollars on your home, you add three hundred and twenty thousand to your running total. If you rent your home, you might want to add a decade worth of rental payments to this category instead to ensure housing stability. Removing the threat of foreclosure or eviction is the most profound gift you can leave behind for a grieving family trying to find their footing.

|

Housing Situation |

Calculation Method |

Goal for Beneficiaries |

|

Homeowner with Mortgage |

Exact remaining loan payoff balance |

Own the home free and clear |

|

Long Term Renter |

Monthly rent multiplied by ten years |

Guaranteed housing stability |

|

Homeowner no Mortgage |

Zero dollars needed in this category |

Redirect funds to income replacement |

Education Costs

If you have children and plan to help them pay for higher education, you must factor this into the math. College tuition, room and board, textbooks, and living expenses have skyrocketed over the last few decades. You need to estimate the future cost of a four year degree for each child you intend to support.

While public universities are more affordable than private institutions, a conservative estimate for a standard four year public university education is roughly one hundred thousand dollars per child. If you have two children, you add two hundred thousand dollars to your calculation. By isolating this cost, you guarantee that your death does not force your children to abandon their academic dreams or take on massive, life altering student loan debt just to get a degree.

|

Number of Children |

Estimated Public College Cost |

Total Education Allocation |

|

One Child |

One hundred thousand dollars |

One hundred thousand dollars |

|

Two Children |

One hundred thousand dollars each |

Two hundred thousand dollars |

|

Three Children |

One hundred thousand dollars each |

Three hundred thousand dollars |

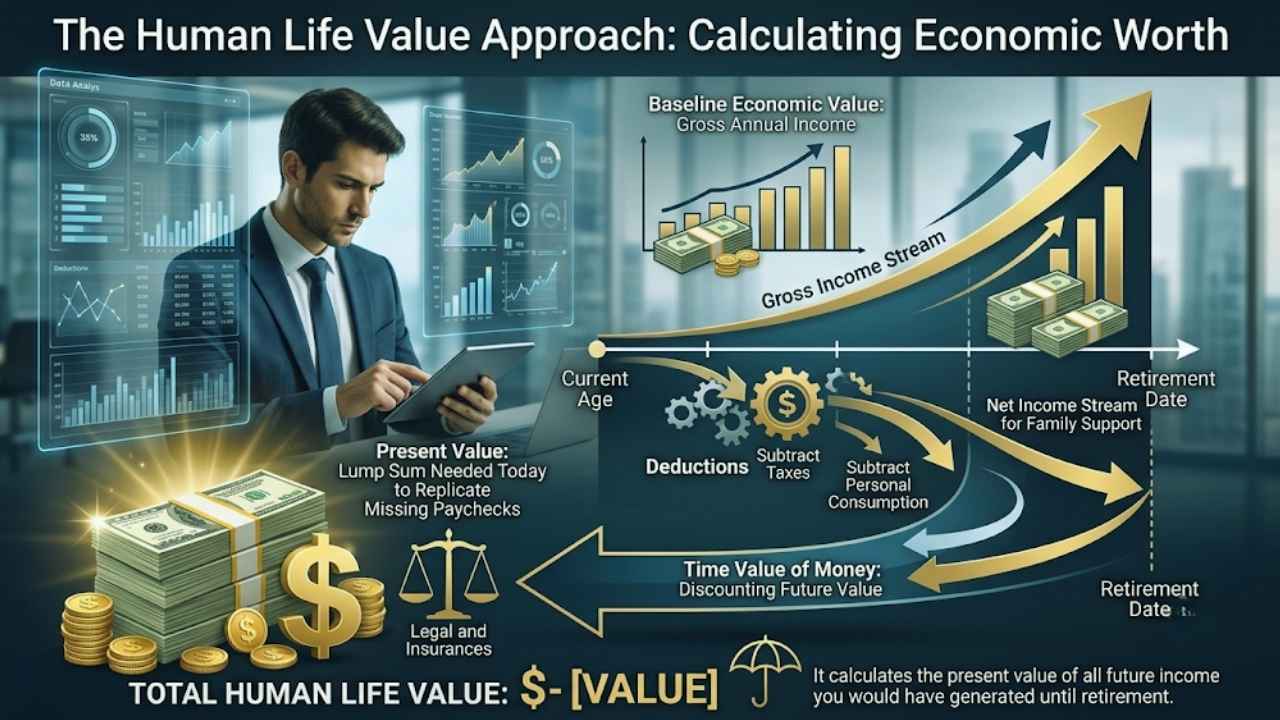

2. The Human Life Value Approach

While the DIME method looks at your family future expenses, the Human Life Value approach looks directly at your economic worth. This is the method frequently used by insurance underwriters and legal professionals to determine the total financial loss a family suffers when an earner passes away. It calculates the present value of all the future income you would have generated until your retirement date. The math here is a bit more complex because it accounts for taxation, personal consumption, and the time value of money.

The time value of money simply means that a dollar received today is worth more than a dollar received ten years from now, because today dollar can be invested and grow. Start with your gross annual income, subtract your taxes, and subtract the money you spend on yourself. You then apply a discount rate to determine the exact lump sum needed today to replicate your missing paychecks for the rest of your natural working years.

|

Calculation Step |

Action Required |

Purpose of the Step |

|

Gross Income |

Identify total yearly earnings |

Establishes the baseline economic value |

|

Deductions |

Subtract taxes and personal spending |

Finds the true amount supporting the family |

|

Present Value |

Apply investment discount rate |

Calculates the exact lump sum needed today |

3. The Income Multiplier Rule

If you find the detailed DIME method and the complex Human Life Value approach too tedious for a quick assessment, the income multiplier rule is the most widely accepted shortcut. Financial experts often suggest buying a policy that is ten to fifteen times your current gross annual income. If you earn ninety thousand dollars a year, this rule dictates that you need between nine hundred thousand and one point three five million dollars in coverage.

This method is incredibly fast and gives you a solid ballpark figure within seconds. The logic is that investing a lump sum of ten times your salary in a moderately conservative portfolio will generate enough interest and dividends to replace a significant portion of your income without rapidly depleting the principal. However, this method scales purely based on income and completely ignores your actual liabilities, so it should only be used as a preliminary starting point.

|

Your Annual Income |

Ten Times Multiplier |

Fifteen Times Multiplier |

|

Fifty thousand |

Five hundred thousand |

Seven hundred fifty thousand |

|

Seventy five thousand |

Seven hundred fifty thousand |

One point one million |

|

One hundred thousand |

One million dollars |

One point five million |

4. The Income Plus Education Formula

This method acts as a reliable middle ground between the overly simplistic multiplier rule and the highly detailed DIME method. It acknowledges that the basic income multiplier often falls short when higher education costs are involved. To use this formula, you take your gross annual income and multiply it by ten. Then, you simply add one hundred thousand dollars for every child you plan to send to college.

If a parent earns seventy five thousand dollars a year and has three children, the math is incredibly straightforward. First, seventy five thousand multiplied by ten equals seven hundred and fifty thousand. Next, three children multiplied by one hundred thousand equals three hundred thousand. Adding those two figures together gives a recommended coverage amount of one million and fifty thousand dollars. It is a highly effective calculation for busy parents who want a safe number without tracking down every single credit card statement in the house.

|

Family Setup |

Multiplier Calculation |

Education Addition |

Total Policy Need |

|

Parent making 80k, 1 child |

Eight hundred thousand |

One hundred thousand |

Nine hundred thousand |

|

Parent making 100k, 2 kids |

One million dollars |

Two hundred thousand |

One point two million |

|

Parent making 120k, 3 kids |

One point two million |

Three hundred thousand |

One point five million |

Factors That Change Your Life Insurance Math Over Time

The calculation you perform today will not remain accurate forever. Your financial life is dynamic, and as your circumstances change, the math behind your life insurance needs will shift. A policy that perfectly covers your family at age thirty might be woefully inadequate at age forty, or entirely unnecessary by age sixty. You must treat your life insurance coverage as a living document that requires periodic review. If you set it and forget it, you risk exposing your family to massive financial gaps if your lifestyle upgrades significantly over a decade.

Inflation and Cost of Living

Inflation is the silent erosion of your purchasing power over time. A one million dollar death benefit sounds like a massive fortune today, but historically, the cost of living doubles roughly every twenty to twenty five years due to standard inflation. If you buy a thirty year term policy today, the real world buying power of that payout in the final years of the term will be significantly less than it is right now.

When calculating your income replacement needs, it is wise to build in a buffer to account for the rising costs of groceries, healthcare, and housing. A loaf of bread and a gallon of gas will cost much more in fifteen years, meaning your family will need more raw dollars to maintain the exact same standard of living. Factoring in a mild inflation buffer prevents the death benefit from falling short in the distant future.

|

Economic Factor |

Current Impact |

Future Impact in 20 Years |

|

Groceries |

Takes ten percent of budget |

Could require double the raw dollar amount |

|

Healthcare |

High premiums |

Expected to vastly outpace standard inflation |

|

General Inflation |

Slow erosion of cash value |

Cuts the buying power of the payout in half |

Changes in Family Dynamics

Life events are the primary triggers for recalculating your coverage. The birth of a new child immediately adds hundreds of thousands of dollars to your liability column in the form of future living expenses and college tuition. Getting married merges your financial life with another person, creating mutual dependencies that must be protected.

Conversely, going through a divorce can drastically alter your obligations, especially if alimony or child support agreements mandate specific life insurance requirements. Caring for an aging parent who suddenly moves into your home also increases the financial burden your policy would need to cover. Every time a human being enters or leaves your immediate financial sphere of responsibility, you need to pull out the calculator and run the numbers again.

|

Life Event |

Liability Shift |

Recommended Insurance Action |

|

Having a Baby |

Massive increase in expenses |

Buy more coverage or add a supplemental policy |

|

Getting Married |

Shared debt and income reliance |

Run the DIME method for both partners |

|

Divorce |

Division of assets and child support |

Adjust beneficiaries and meet legal requirements |

Wealth Accumulation and Asset Growth

This is the most positive factor that changes your math over the decades. As you move through your career, your net worth should theoretically increase year after year. You pay down your mortgage principal every month, shrinking your largest debt. You contribute steadily to your retirement accounts. You build up cash reserves in high yield savings accounts. This ongoing process is known as self insurance.

As your liquid assets grow and your massive debts shrink, the financial gap that life insurance needs to cover gets smaller and smaller. When you are thirty with a new house and no savings, your need for insurance is at its absolute peak. By the time you are sixty, your house might be entirely paid off, your kids have graduated and moved out, and your retirement accounts are fully funded. At that point, your mathematical need for life insurance drops entirely to zero.

|

Age Stage |

Debt to Asset Ratio |

Insurance Need Level |

|

Age Thirty |

High debt, very low assets |

Maximum coverage required |

|

Age Forty Five |

Medium debt, growing assets |

Moderate coverage required |

|

Age Sixty |

Zero debt, massive retirement assets |

Zero coverage required |

Term vs. Permanent Life Insurance: Does the Math Change?

Once you know how much coverage you need, you have to decide what type of policy to buy. The life insurance industry is broadly split into two categories, which are term and permanent life insurance. The type of policy you choose has a massive impact on the math of your monthly budget. Getting the policy type wrong can force you to underinsure your family simply because of extreme budget constraints. It is highly recommended that you understand the mechanics of both before signing any paperwork.

Term Life Insurance: Pure Protection

Term life insurance is incredibly straightforward and cost effective. You buy a specific amount of coverage for a specific period of time, usually ten, twenty, or thirty years. If you pass away during that term, your family gets the money tax free. If you outlive the term, the policy simply expires, and you get nothing back. It functions exactly like car insurance or homeowners insurance.

You are paying for pure risk protection without any hidden fees. Because there is an expiration date, term insurance is remarkably inexpensive. For the vast majority of families, term insurance is the only mathematical choice that makes sense. It allows you to buy massive amounts of coverage to satisfy the DIME method during the years when your family is most vulnerable, without destroying your monthly cash flow. It perfectly aligns with the concept that your need for insurance is temporary and will fade as you build wealth.

|

Policy Feature |

Description |

Benefit to the Consumer |

|

Set Duration |

Lasts 10 to 30 years |

Matches your years of highest financial liability |

|

Low Cost |

Very cheap monthly premiums |

Allows you to afford the massive coverage you actually need |

|

Pure Risk |

No confusing investment components |

Straightforward protection without hidden administrative fees |

Permanent Life Insurance: Coverage Plus Cash Value

Permanent life insurance, which includes whole life and universal life, is designed to last until the day you die, regardless of when that is. Because the insurance company knows they will eventually have to pay out the death benefit, the premiums are astronomically higher than term insurance. These policies also include a cash value savings component that grows very slowly over time. While insurance agents love to sell permanent policies because they carry massive commissions, the math rarely works out for the average person.

The premiums are so high that most people cannot afford to buy the actual amount of coverage their family needs. They end up severely underinsured just to get a permanent policy. For ninety nine percent of the population, the mathematically superior strategy is to buy a cheap term policy and invest the difference in premium costs into traditional investment vehicles like mutual funds or real estate. Permanent insurance is generally only necessary for ultra high net worth individuals who need liquidity to pay estate taxes.

|

Policy Feature |

Description |

Drawback for the Average Consumer |

|

Lifetime Coverage |

Never expires |

Drives the monthly premium cost astronomically high |

|

Cash Value |

Builds savings inside the policy |

Returns are usually lower than basic stock market index funds |

|

High Commissions |

Agents push these products hard |

Consumers often buy too little coverage just to afford the premium |

Real-Life Scenarios: Putting the Math to the Test

To truly understand how these calculation methods work, it is helpful to look at realistic scenarios. By applying the math to different life stages, you can see how drastically the numbers shift based on individual circumstances. Math in a vacuum is boring, but seeing it applied to real life constraints makes the utility of life insurance obvious. You will quickly notice why standard rules of thumb fall apart when tested against actual human lives.

Scenario 1: The Young Family with a Mortgage

Consider Sarah and John, a married couple in their early thirties. They just had their first child and purchased a home in the suburbs. John earns ninety thousand dollars a year, and Sarah is taking five years off work to raise their child before reentering the workforce. They have a three hundred and fifty thousand dollar mortgage and about twenty thousand dollars in combined student loan and car debt. Using the DIME method for John, his debt is twenty thousand dollars.

Sarah needs his income replaced for at least fifteen years until their child is more independent, meaning ninety thousand multiplied by fifteen is one point three five million dollars. The mortgage is three hundred and fifty thousand, and they want one hundred thousand for the baby future college fund. John total mathematical need is one point eight two million dollars. He needs a thirty year term policy for roughly one point eight million to guarantee his family exact lifestyle remains intact.

|

DIME Category |

Sarah and John Cost |

Total |

|

Debt |

Twenty thousand |

$20,000 |

|

Income |

Ninety thousand times 15 years |

$1,350,000 |

|

Mortgage |

Three hundred fifty thousand |

$350,000 |

|

Education |

One hundred thousand |

$100,000 |

Scenario 2: The Single Parent Building a Safety Net

Michael is a forty year old single father raising two teenagers by himself. He is the sole financial provider, earning one hundred and ten thousand dollars a year. He currently rents an apartment, so he has no mortgage, but he has fifteen thousand dollars in credit card debt. He wants to make sure his kids can get through college and that their designated legal guardian has financial support to raise them if he passes away.

Using the DIME method, his debt is fifteen thousand plus fifteen thousand for final expenses, totaling thirty thousand. He wants to provide ten years of income replacement, meaning one hundred and ten thousand multiplied by ten is one point one million dollars. His mortgage is zero. His education goal is two hundred thousand dollars to cover university for both teenagers. Michael total need is one point three three million dollars. Even without a mortgage, Michael role as the sole provider means he needs a substantial policy to protect his children.

|

DIME Category |

Michael Cost |

Total |

|

Debt |

Thirty thousand |

$30,000 |

|

Income |

One hundred ten thousand times 10 |

$1,100,000 |

|

Mortgage |

Zero dollars |

$0 |

|

Education |

Two hundred thousand |

$200,000 |

Scenario 3: The Dual Income Couple with No Kids

Alex and Jamie are in their late twenties. They are married, both work full time, and have decided never to have children. Alex makes seventy thousand a year, and Jamie makes eighty thousand. They rent a condo in the city and live entirely debt free. Because they have no dependents, no mortgage, and no consumer debt, their mathematical need for life insurance is incredibly low.

If one of them passes away, the other can easily survive on their own income without facing bankruptcy. However, they might want a small policy to cover funeral expenses and provide a financial cushion so the surviving spouse can take six months off work to grieve without worrying about rent. A simple term policy of one hundred thousand to two hundred and fifty thousand dollars for each of them is more than enough to cover those transitionary costs. They do not need million dollar policies.

|

DIME Category |

Alex and Jamie Cost |

Total |

|

Debt |

Fifteen thousand for funeral |

$15,000 |

|

Income |

Forty thousand for 6 months leave |

$40,000 |

|

Mortgage |

Zero dollars |

$0 |

|

Education |

Zero dollars |

$0 |

How Often Should You Recalculate: How Much Life Insurance Do I Need?

Life insurance is not a set it and forget it product that you buy once in your twenties and ignore forever. Because your life changes constantly, your math needs to be updated. You should sit down with a calculator and run your numbers at least once every major life milestone. Letting a policy sit unchecked for twenty years is a recipe for disaster if your lifestyle has dramatically upgraded in the meantime.

Review Triggers and Timelines

You need to recalculate your coverage when you get married or divorced, as this shifts your primary beneficiaries entirely. You must run the numbers again every time you welcome a new child into the family, adding their education and living costs to your liability column. Buying a new home, taking on a larger mortgage, or starting a small business all require an immediate reassessment of your debts.

Additionally, massive increases in your income or major promotions mean your family is getting accustomed to a higher standard of living, which requires more income replacement to maintain. Conversely, when you finally pay off your house or reach a point where your retirement accounts hit the million dollar mark, you should recalculate to see if you can safely drop your life insurance coverage altogether. A good rule of practice is to review your DIME calculation every three to five years, ensuring your safety net always perfectly matches your reality.

|

Trigger Event |

Why You Must Recalculate |

Next Steps |

|

Marriage or Divorce |

Shifts your primary beneficiaries |

Update beneficiaries and run DIME |

|

Buying a House |

Adds a massive new liability |

Increase policy size to cover mortgage |

|

Large Salary Increase |

Family standard of living goes up |

Run multiplier method with new pay |

Final Thoughts

We have walked through the numbers, and the math is incredibly clear. You no longer have to blindly wonder how much life insurance do I need while sitting across from a pushy insurance broker. By applying proven methods like DIME or the Human Life Value approach, you take full control of your financial planning. You can confidently purchase a term policy that provides exactly the right amount of protection for your spouse and children without draining your current bank account.

Remember, this is about replacing your economic engine if it suddenly stops working. Run the numbers today, secure the policy while you are young and healthy, and then get back to enjoying your life. The peace of mind that comes from knowing your family is mathematically protected is worth every minute you spend calculating it. Financial experts agree that taking action now is infinitely better than waiting for perfect conditions to arrive.

Frequently Asked Questions (FAQs) About How Much Life Insurance Need

Do stay at home parents need life insurance?

Yes, absolutely. While a stay at home parent might not bring in a traditional salary, their economic value to the household is massive. If they were to pass away, the surviving spouse would suddenly have to pay for full time childcare, household management, cleaning, and meal preparation. These services are incredibly expensive. A stay at home parent should typically have enough coverage to pay for these replacement services until the youngest child is out of the house.

Is the life insurance provided by my employer enough?

In most cases, employer provided life insurance is nowhere near enough. Most companies offer a basic group policy that covers one or two times your annual base salary. As the math methods above demonstrate, most families need closer to ten or fifteen times their income to be fully protected. Furthermore, employer policies are usually tied to your job. If you get fired, laid off, or switch companies, you lose your coverage instantly. It is always best to own an independent, private policy that you control.

Are life insurance payouts subject to income tax?

Generally, no. The death benefit paid out to your beneficiaries is considered entirely tax free by the federal government. If your family receives a one million dollar check, they get to keep exactly one million dollars. The only time taxes become an issue is in complex estate planning scenarios involving incredibly large estates, which is why the death benefit amount you calculate does not usually need to be inflated to account for massive tax deductions.

Can I have more than one life insurance policy at a time?

Yes, and this is actually a very common strategy known as the ladder method. Instead of buying one massive thirty year policy, a person might buy a large twenty year policy to cover the years their kids are growing up, and a smaller thirty year policy to cover their mortgage payoff. As the shorter policies expire, your overall coverage drops, which aligns perfectly with your decreasing financial liabilities and saves you money on premiums over time.

What happens if I outlive my term life insurance policy?

If you outlive your term life policy, the coverage simply expires. You do not get your premium payments back, but that is actually the ideal scenario. The goal of term insurance is to protect your family during your high liability years. By the time the term expires, you should be financially self sufficient, meaning you no longer need life insurance.

Can I lower my coverage amount later if my debts decrease?

Yes. Most insurance companies allow you to reduce the face value of your term policy, which will subsequently lower your monthly premiums. If you pay off your mortgage ten years early, you can contact your provider and request a coverage reduction to match your newly lowered financial liabilities.

{kind=link}