You have probably heard TV talking heads complain about central banks “printing money” during a crisis. They make it sound like a giant machine is turning out stacks of fresh greenbacks in some dark government basement. The reality is a lot less dramatic and entirely digital.

But it goes by a heavily clinical name that confuses most people. If you are trying to figure out what is quantitative easing, you are looking at the exact financial emergency button that central banks push when normal economic fixes completely crash.

Usually, when the economy tanks, central banks cut short-term interest rates. This makes borrowing cheap, which gets people and businesses spending again. But what happens when those interest rates hit absolute zero? You simply cannot cut them any lower. That is when the financial powers bring out the heavy artillery to force cash into the system. Let’s strip away the textbook jargon and look at how this strategy actually works, why it matters to your wallet, and what it is doing to the global economy right now in 2026.

What Is Quantitative Easing?

To truly grasp the mechanics behind what is quantitative easing (often shortened to QE), you have to look at how central banks behave behind closed doors. It is an incredibly aggressive monetary policy where a central bank, like the Federal Reserve in the US or the European Central Bank in Europe, steps into the open market and buys massive piles of financial assets.

Most of the time, they specifically buy long-term government bonds and mortgage-backed securities from private institutions. By buying these assets up in huge quantities, the central bank intentionally floods the banking system with a massive wave of liquid cash. The end goal is incredibly simple: give commercial banks so much idle money that they have absolutely no choice but to lend it out to everyday consumers and businesses at rock-bottom interest rates.

When it costs almost nothing to borrow money, regular people confidently buy new houses. Local businesses build new warehouses and hire more staff. Everyday consumers finance new cars and appliances. That sudden, massive wave of spending acts exactly like a defibrillator to a frozen, panicked economy, forcing money to change hands when everyone otherwise wants to hoard it.

|

Core Mechanic |

How It Functions In Reality |

The Direct Economic Goal |

|

Asset Buying Spree |

Central banks buy up bonds from private lenders. |

Clears slow-moving assets off private bank ledgers. |

|

Digital Cash Injection |

New electronic money pays for those bonds. |

Forces fresh, liquid cash directly into the banking system. |

|

Crushing Bond Yields |

Massive bond buying drives long-term interest rates down. |

Makes 15-year and 30-year loans significantly cheaper. |

|

Pushing Retail Loans |

Private banks sit on heaps of idle, non-profitable cash. |

Compels banks to offer easy credit to move their money. |

How Central Banks Print Money with a Keyboard?

One of the absolute biggest myths surrounding this entire concept is the vivid image of ink and paper. Today, central banks create money with nothing more than a few deliberate keystrokes. Here is exactly how the financial plumbing works in the real world. The Federal Reserve decides it wants to inject billions of dollars into the financial system to stop a panic. It contacts major commercial banks and offers to buy their extremely safe government bonds.

But to pay for those bonds, the Fed does not transfer existing tax funds, and it does not borrow money from foreign nations. It simply updates a digital ledger, instantly crediting the commercial banks’ reserve accounts with brand-new digital cash created completely out of thin air. Once those private banks hold this newly minted digital cash, they face an immediate business problem.

Banks do not make a profit by just holding onto cash; they make money by charging interest on loans. Because they are suddenly flush with billions in reserves, they drop their lending standards and slash their interest rates to get that money out the door as fast as possible. That specific chain reaction is exactly how cash travels from a central bank computer screen straight into the real, functioning economy.

|

Operational Step |

Central Bank Action |

Real-World Impact on You |

|

1. The Trigger |

Bank sets a massive, multi-billion dollar asset-buying target. |

Financial markets rally instantly on the news. |

|

2. The Digital Swap |

Bank buys government bonds from private financial institutions. |

Safe bonds move directly to the central bank’s ledger. |

|

3. The Deposit |

Bank artificially credits private bank reserve accounts. |

Private banks instantly become incredibly cash-rich. |

|

4. The Ripple Effect |

Private banks slash their loan rates to move the idle cash. |

Regular people borrow, buy property, and invest heavily. |

Why Pull the Emergency Brake?

Central bankers absolutely do not play with this tool during normal, everyday economic times. It is a radical, highly controversial step saved specifically for avoiding a catastrophic deflationary spiral. Deflation might sound great on paper because everyone loves the idea of cheaper groceries and rent. But in reality, it completely destroys modern economies. If prices drop consistently every single week, you naturally stop buying big-ticket items today because you know they will cost significantly less next month.

When everyone collectively stops buying, corporate revenues completely collapse, mass layoffs spike, and the entire economy freezes solid. Furthermore, when a major financial crash happens, simply dropping short-term rates to zero is almost never enough to make terrified business owners take out new loans. By stepping in and buying long-term bonds, the central bank deliberately targets and suppresses long-term interest rates.

This forceful action pushes investors out of safe, boring government bonds and forces them to put their money into riskier places, like corporate bonds or the stock market. That sudden rush of investment capital keeps struggling businesses from going under and thaws out completely frozen credit lines.

|

Economic Danger |

The Standard Playbook |

Why Extreme Measures Take Over |

|

Typical Recession |

Cut interest rates by 1 or 2 percent. |

Usually more than enough to get people borrowing again. |

|

Major Economic Collapse |

Cut interest rates all the way to 0 percent. |

Traditional monetary tools hit an absolute dead end at zero. |

|

Deflationary Spiral |

Standard interest rate cuts fail to spark demand. |

Needs a massive wall of cash to forcefully jumpstart spending. |

|

Total Credit Freeze |

Banks stop lending out of pure, unchecked panic. |

A flood of central cash forces banks back into the lending game. |

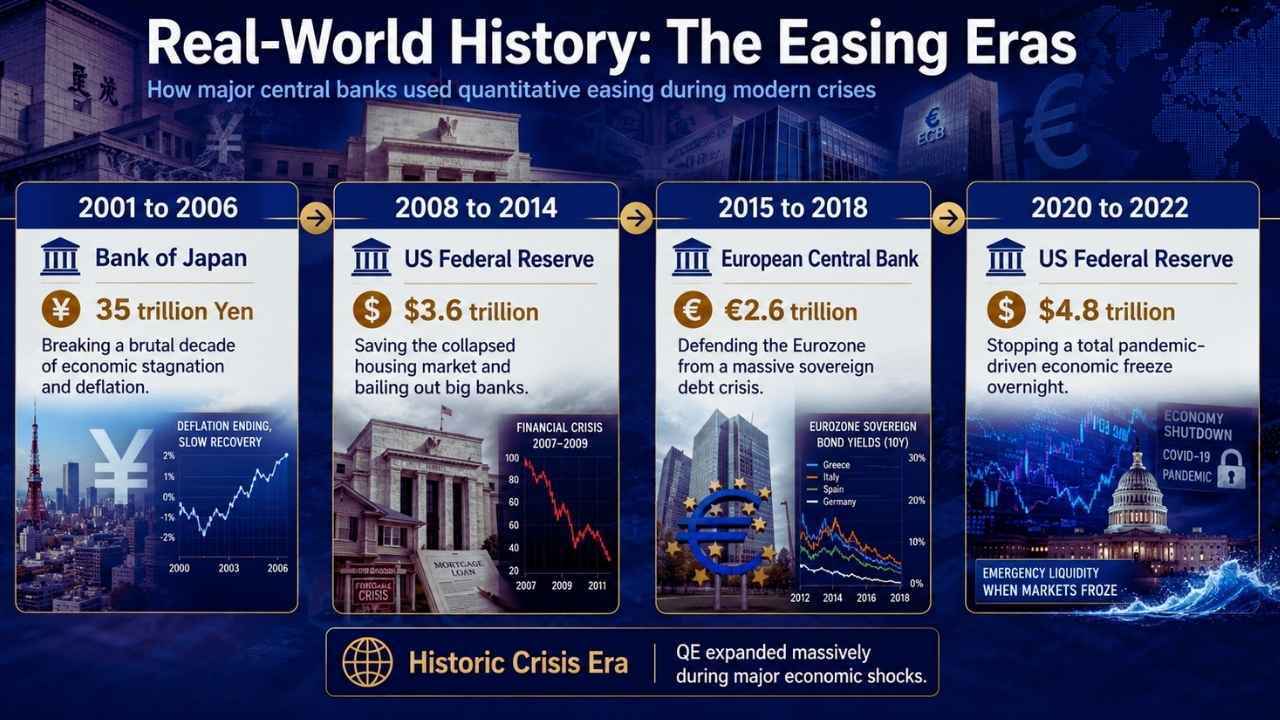

Real-World History: The Easing Eras

You can see exactly how this complex engine functions by looking back at the major economic crises of our lifetime. Japan actually experimented with this policy first in the early 2000s in a desperate attempt to break a brutal decade of economic stagnation. But the strategy truly became a global household term immediately following the 2008 housing crash. In late 2008, the global financial system almost came completely apart at the seams.

The US Federal Reserve launched multiple consecutive rounds of asset purchases, buying up deeply toxic mortgages just to clean up bank balance sheets and prevent a total banking collapse. The Fed’s total asset pile exploded from roughly $900 billion to well over $4.5 trillion by 2014. It successfully stabilized the housing market and lit a massive fire under the stock market. Then came the terrifying spring of 2020. Global pandemic lockdowns forcibly closed businesses and erased millions of jobs in a single week.

The Fed responded with the fastest, most aggressive cash injection ever recorded in human history, buying trillions in assets in just a few months. They pushed their balance sheet near a staggering $9 trillion by 2022, keeping the global economy’s lights on but leaving behind a massive, complicated economic hangover.

|

Historic Crisis Era |

Central Bank Involved |

Total Amount Added |

Main Economic Focus |

|

2001 to 2006 |

Bank of Japan |

35 trillion Yen |

Breaking a brutal decade of economic stagnation and deflation. |

|

2008 to 2014 |

US Federal Reserve |

3.6 trillion Dollars |

Saving the collapsed housing market and bailing out big banks. |

|

2015 to 2018 |

European Central Bank |

2.6 trillion Euros |

Defending the Eurozone from a massive sovereign debt crisis. |

|

2020 to 2022 |

US Federal Reserve |

4.8 trillion Dollars |

Stopping a total pandemic-driven economic freeze overnight. |

The 2026 Reality Check: The Hangover Hits Home

You simply cannot truly understand what is quantitative easing without looking at what happens when the party ends and the bill comes due. All that digital money injected during the pandemic stayed deep inside the global financial plumbing, making the entire system incredibly sensitive to sudden supply shocks. By the start of 2026, the Federal Reserve had spent years desperately trying to shrink its massive balance sheet, successfully rolling it back down from its $9 trillion peak to exactly $6.7 trillion by March 2026.

However, the first half of 2026 threw a massive, unexpected wrench into the gears of global recovery. Serious geopolitical tensions disrupted major global energy corridors, causing global oil and natural gas prices to absolutely skyrocket overnight. Because the financial system was still heavily saturated with leftover liquidity from past interventions, this new energy supply shock triggered sudden, sharp inflation.

In May 2026, official US inflation jumped back up to a painful 4.25 percent, heavily driven by a massive 23.5 percent spike in energy costs. Across the Atlantic, Eurozone inflation hit 3.2 percent. Central banks had to pivot instantly, with the European Central Bank issuing a fresh 25-basis-point interest rate hike in June 2026, bringing its main rate up to 2.40 percent just to keep prices from spiraling entirely out of control.

|

2026 Economic Metric |

Current Official Status |

The Direct Connection to Past Policies |

|

Fed Balance Sheet |

6.7 Trillion Dollars |

Stays incredibly high compared to historical pre-2020 norms. |

|

US Inflation Rate |

4.25 percent (May 2026) |

Lingering cash in the system severely amplified the energy price shock. |

|

Eurozone Inflation |

3.2 percent (May 2026) |

Forced the ECB to completely abandon rate cuts and hike instead. |

|

ECB Benchmark Rate |

2.40 percent (June 2026) |

Higher rates are desperately required to mop up excess global liquidity. |

The Winners and Losers of Easy Money

Top economists fight endlessly over whether this aggressive strategy is a brilliant cure or a dangerous curse. On one hand, it works absolutely perfectly as a short-term shield against total financial ruin. It instantly thaws out frozen credit, saves thousands of businesses from immediate bankruptcy, and keeps everyday people employed when a sudden panic hits the markets.

But the long-term price tag is remarkably heavy, and it actively creates a stark, painful divide between the wealthy and the working class. Because the policy intentionally drives interest rates to the absolute floor, keeping your hard-earned money in a normal savings account pays you absolutely nothing. To get any kind of positive return, conservative savers are aggressively forced to risk their money in the stock market or buy real estate.

This massive, unnatural rush of cash creates giant asset bubbles where stock portfolios surge disconnected from reality and home prices skyrocket. If you already own a house and a dense stock portfolio when the money printer turns on, you get incredibly rich without lifting a finger. But if you are a young professional just trying to buy your very first home, you get completely locked out of the market. It remains one of the single largest drivers of modern wealth inequality in the world today.

|

The Clear Upside |

The Painful Downside |

|

Halts market panics and prevents deep depressions. |

Spikes the serious risk of painful, long-term consumer inflation. |

|

Keeps credit flowing so businesses can pay workers. |

Starves conservative savers by forcing 0 percent interest rates. |

|

Drives down borrowing costs for retail consumer loans. |

Pumps up massive, artificial bubbles in housing and stock markets. |

|

Stabilizes highly volatile global markets during a crisis. |

Drastically widens the wealth gap between asset owners and workers. |

How QE Directly Hits Your Wallet?

Monetary policy often sounds like a highly distant, boring academic topic, but it actively and aggressively alters your everyday financial reality. When a central bank goes all-in on mass asset purchases, mortgage rates completely plummet to historical lows. During the absolute height of the pandemic easing, US mortgage rates sank well below 3 percent, which allowed millions of families to quickly refinance and cut their monthly housing costs significantly.

But there is never a free lunch when it comes to global economics. Because money was basically completely free to borrow, everyone rushed to buy property at the exact same time. Housing demand went completely through the roof, and home prices wildly jumped 20 to 40 percent in just a couple of short years. A remarkably low interest rate does not actually help you much if the base price of the home is suddenly entirely out of reach.

Your basic savings account also feels the immediate pain. Banks simply do not need your retail deposits when the central bank is happily feeding them billions in digital reserves every month. They cut your savings yield to near zero, meaning inflation slowly eats away at your cash value every single day it sits in the bank.

|

Your Financial Sector |

What Actually Happens During Easing |

The Painful Economic Catch |

|

Home Mortgages |

Interest rates aggressively drop to historic lows. |

Home prices explode upward because absolutely everyone can borrow. |

|

Savings Accounts |

Interest yields drop all the way to near 0 percent. |

Unchecked inflation slowly eats away at your actual cash purchasing power. |

|

Stock Portfolios |

Market values trend sharply and quickly upward. |

Creates a highly fragile stock market heavily hooked on cheap credit. |

|

Everyday Goods |

Short-term price stability keeps groceries affordable. |

Sets the dangerous stage for major, systemic price hikes down the road. |

The U-Turn: Quantitative Tightening (QT)

Central banks know they cannot buy bonds forever without totally breaking the fundamental rules of the free market. Eventually, they are forced to completely reverse the flow of money, and this painful process is officially called quantitative tightening. During this highly restrictive phase, the central bank completely stops its massive buying spree.

When the government bonds they already hold finally reach their maturity date, the bank just lets them expire and permanently deletes the digital cash they originally created to buy them. This brilliant but brutal mechanism sucks money right back out of the commercial banking system. It intentionally drives interest rates back up, makes getting a mortgage highly expensive again, and aggressively cools down overheated stock and housing markets.

It is a incredibly slow, deeply uncomfortable process designed specifically to tame runaway inflation. This tightening cycle is exactly why the Federal Reserve balance sheet dropped to 6.7 trillion dollars in early 2026, and it perfectly explains why consumer borrowing costs remain so stubbornly high as policymakers try desperately to mop up the excess liquidity left over from previous financial crises.

|

Defining Feature |

Quantitative Easing |

Quantitative Tightening |

|

The Core Action |

Central bank aggressively buys market bonds. |

Central bank sells bonds or just lets them quietly expire. |

|

The Money Supply |

Expands massively as new cash is injected. |

Contracts heavily as excess digital cash is finally destroyed. |

|

Interest Rates |

Artificially and intentionally suppressed downward. |

Aggressively pushed upward to restrict retail borrowing. |

|

The Ultimate Goal |

Spark quick growth and encourage wild spending. |

Cool down an overheated, deeply inflationary global economy. |

Final Thoughts

Truly understanding what is quantitative easing gives you an incredibly clear window into how the modern financial world operates. It isn’t just dense economic theory; it’s the underlying engine that dictates your mortgage rate, your grocery bill, and your retirement account.

When a crisis strikes, central banks rely on this tool to flood the system with cash, keeping the economy breathing and stopping financial panics in their tracks. But that safety net comes at a steep price. It punishes savers, creates massive wealth gaps by inflating asset prices, and, as we’re seeing with the energy-driven inflation spikes of 2026, makes the global economy highly sensitive to supply shocks.

Knowing how this cycle of easing and tightening works gives you a distinct advantage. It helps you look past the daily headlines and make much smarter decisions about your own money—whether you’re deciding to lock in a mortgage, invest in the stock market, or figure out the best way to protect your savings from inflation.

Frequently Asked Questions (FAQs) About What is Quantitative Easing

Does quantitative easing actually print physical paper cash?

No. The Bureau of Engraving and Printing prints physical cash. QE strictly creates digital reserves that sit on bank balance sheets. It’s electronic money creation.

Who gets the QE money first?

Large commercial banks and massive financial institutions receive the digital cash first in exchange for their bonds. The theory is they will lend it down to regular consumers, but critics heavily criticize this as “trickle-down” monetary policy.

Can a central bank go bankrupt from doing too much QE?

Technically, no. A central bank controls the currency in which its debts are denominated, meaning it can always create more digital money to pay its bills. However, if they do this recklessly, the currency loses all value, leading to hyperinflation.

Is QE just a massive bailout for rich people?

This is one of the most heated debates in economics. Because QE artificially inflates asset prices like stocks and real estate, the primary beneficiaries are the wealthy who already own those assets. Wage earners who don’t own property generally see their cost of living rise faster than their paychecks.

Why doesn’t the central bank just give the money directly to citizens?

That concept is known as “helicopter money.” By law, central banks in most developed nations are restricted from directly funding citizens’ bank accounts. They can only deal with commercial banks and government debt. Sending direct stimulus checks requires legislation from Congress.

{kind=link}