Wall Street loves making investing look like rocket science. Guys in tailored suits toss around complex jargon to convince everyday people to hand over massive advisory fees. They want you to believe you need insider knowledge to grow your wealth. But I have a secret for you. You don’t need a finance degree to get rich. You just need a simple, ruthlessly efficient strategy you can actually stick to for the long haul.

A three-fund portfolio gives you exactly that. Think of it as the ultimate lazy approach to investing. History proves this simple method consistently beats the pants off expensive, actively managed mutual funds. By holding just three basic index funds, you instantly buy a tiny slice of the entire global stock market and secure a reliable safety net of bonds. You spread your risk across thousands of companies, keep your fees close to zero, and protect your mind from panic selling when the news gets scary. Whether you are opening your first Roth IRA today or rolling over an old 401(k) before retirement, this straightforward method takes the guesswork out of your money. I’ll show you exactly how to set up, manage, and grow your own three-fund portfolio without losing a wink of sleep.

The Three-Fund Portfolio

If you have ever stared blankly at a brokerage screen, you know the feeling. Thousands of ticker symbols blink at you. Endless mutual funds promise the moon. The sheer volume of choices causes terrible analysis paralysis. The financial industry purposely manufactures this complexity so you will pay them for help.

You can cut right through all that noise. A three-fund portfolio shrinks your entire investment strategy down to just three core assets. These three funds cover everything you will ever need to build a massive nest egg. You just buy them, hold them, and let the global economy do all the heavy lifting while you go live your life. This approach removes emotional decision-making, lowers your tax burden, and frees up your weekends.

|

Concept |

Description |

|

Strategy Origin |

Created by Taylor Larimore, inspired by Vanguard founder Jack Bogle |

|

Core Philosophy |

Keep fees low, diversify globally, and hold your assets forever |

|

Asset Count |

Three total market index funds (Domestic, International, Bonds) |

|

Management Style |

Passive index investing with a simple yearly check-in |

The Beauty of Keeping Investing Simple

Brokers thrive on the illusion of complexity. When financial products look hard to understand, consumers willingly pay professionals a large cut of their wealth every single year. Yet decades of hard data prove that simple, passive index strategies crush expensive portfolios over a twenty-year timeline. You don’t have to guess which artificial intelligence startup will dominate next year. You don’t have to predict which industry will crash next month. Keeping your strategy deliberately boring eliminates the friction and high costs that cause most regular investors to bleed money.

What Exactly is a Three-Fund Portfolio?

Think of it as a lazy portfolio designed to own a piece of everything. Instead of hunting for the needle in the haystack, you just buy the entire haystack. The strategy relies on three broad-market index funds. First, you buy a total domestic stock market fund. Second, you buy a total international stock market fund. Third, you buy a total domestic bond market fund. Combined, these three distinct funds give you fractional ownership in roughly ten thousand individual companies and thousands of stable government bonds.

The Bogleheads Philosophy Explained

This strategy traces its roots directly to Jack Bogle. He founded Vanguard and invented the first retail index fund back in the 1970s. A fiercely loyal online community of his followers, known as Bogleheads, popularized the three-fund approach. They treat it as the ultimate life hack for retail investors. The philosophy relies on a few strict rules. Keep your investment costs as low as mathematically possible. Diversify across all global sectors. Never try to time the market by jumping to cash. Most importantly, stay the course when the market inevitably takes a dive.

Why Choose a Three-Fund Portfolio for Your Investments?

Picking a core investment strategy represents the biggest hurdle for new investors. People get so overwhelmed they just leave their life savings rotting in a standard checking account. Thanks to inflation, that cash loses purchasing power every single year. For context, U.S. inflation hovered around 4.18% annually coming into mid-2026. A basic savings account simply won’t beat that.

A three-fund portfolio solves this problem beautifully. It offers maximum return potential with almost zero ongoing maintenance. It shields you from the devastating loss of a single major corporation going bankrupt. At the same time, it ensures you capture the raw upside of human innovation and economic growth. Once you set the wheels in motion, the math works heavily in your favor.

|

Advantage |

Benefit to Investor |

|

Maximum Diversification |

Protects against single-company bankruptcies and sector crashes |

|

Ultra-Low Fees |

Keeps the massive power of compound interest working for you |

|

Zero Manager Risk |

Removes the danger of a hotshot fund manager making bad bets |

|

Emotional Safety |

Reduces the primal urge to panic sell during bear markets |

Maximum Diversification with Minimal Effort

Buying a single United States total market fund drops shares of over 3,500 American companies right into your lap. You suddenly own tiny pieces of massive tech giants, reliable consumer staples brands, and small regional businesses you haven’t even heard of yet. Adding an international fund captures the rest of the global economy. You get a direct stake in European pharmaceuticals, Japanese automakers, and emerging markets. If a single industry or country experiences a brutal recession, your portfolio barely flinches. The other sectors absorb the shock and keep marching upward.

Crushing Fees with Low Expense Ratios

High fees act as the silent killer of wealth. Actively managed funds often charge upwards of 0.50% to 1% annually. Paying a financial advisor a standard one percent fee every year doesn’t sound terrible today. But over a thirty-year timeline, those fees will devour nearly a third of your total potential wealth. A standard index fund charges practically nothing. As of 2026, the Vanguard Total Stock Market ETF (VTI) charges an incredibly low 0.03% expense ratio. That means you pay just $3 a year for every $10,000 you invest. Keeping your fees near zero allows your money to snowball without interruption.

Zero Manager Risk and Style Drift

Buying a shiny, actively managed mutual fund means you are gambling on the genius of one specific fund manager. If that manager retires, loses their edge, or suddenly shifts their strategy to chase a hot trend, your personal returns suffer. The industry calls this manager risk. A three-fund portfolio relies entirely on passive index funds. These funds just track a set list of companies mechanically. A computer algorithm buys and sells shares to match the index perfectly. This completely removes human error, ego, and greed from your financial equation.

The Core Components of the Portfolio

To build a house that lasts a century, you need the right materials from the ground up. The three-fund portfolio uses three distinct asset classes to construct a financial foundation built to survive massive economic storms. Each component serves a very different purpose in your overall game plan. The domestic and international stock funds act as the high-horsepower engine of your portfolio. They drive massive long-term growth to outpace inflation. The bond fund acts as the heavy shock absorber. It protects your mental health when the stock market goes through its regular cycles of terrifying panic.

|

Component |

Asset Class |

Primary Purpose |

Risk Level |

|

Fund 1 |

Total US Stock Market |

High growth and long-term capital appreciation |

High volatility |

|

Fund 2 |

Total International Stock |

Global diversification and currency risk reduction |

High volatility |

|

Fund 3 |

Total US Bond Market |

Stability, steady income, and crash protection |

Low volatility |

Domestic Equities (Total U.S. Stock Market)

The United States stock market serves as the primary wealth engine of this entire setup. This specific fund tracks basically every publicly traded company within US borders. It gives you immediate exposure to large-cap, mid-cap, and small-cap stocks all wrapped into a single, highly efficient package. Historically, the US market drives phenomenal returns. For example, looking at mid-2026 data, the Vanguard Total Stock Market Index Fund (VTSAX) surged nearly 30% over the previous 12 months. Since you are buying pure equities, this component brings massive long-term growth. Just remember it also brings wild, sometimes scary short-term price swings.

International Equities (Total International Stock Market)

Ignoring businesses outside the United States means ignoring roughly forty percent of the global stock market. An international stock fund gives you direct ownership in developed markets across Europe and the Pacific. You also pick up rapidly expanding emerging markets. International stocks underperformed US stocks over the last decade, but market dominance always runs in cycles. Holding international stocks protects you during the inevitable decades when the US market cools down. It ensures your portfolio captures growth wherever it pops up globally.

Fixed Income (Total U.S. Bond Market)

Think of bonds as the safety net of your overarching investment strategy. When you buy a total bond market fund, you effectively loan your money to the US Treasury and high-quality American corporations. In exchange, they pay you regular interest. Bonds absolutely offer lower long-term total returns than stocks. Their true value lies in their boring stability. During severe stock market crashes, bonds usually hold their ground. A solid bond allocation keeps your account balance from plummeting too deep. This makes it infinitely easier for you to hold on and avoid selling in terror.

How to Build Your Three-Fund Portfolio: Step-by-Step?

Setting up this portfolio takes less than an hour on a lazy Sunday afternoon. But the specific decisions you make today will heavily dictate your financial trajectory for decades. You have to look honestly at your long-term goals, your actual age, and your emotional ability to handle seeing red numbers on a screen.

Once you figure out how much risk you can stomach, you choose your percentages, open the right low-cost account, and buy the funds. It ranks as a highly repeatable process, but it requires some honest self-reflection before you click the buy button.

|

Step |

Action Required |

Importance |

|

Step 1 |

Assess risk tolerance and timeline |

Determines how aggressively you can invest without panicking |

|

Step 2 |

Determine asset allocation |

Dictates your specific ratio of stocks to bonds |

|

Step 3 |

Choose a low-cost brokerage |

Ensures you never pay high platform or trading fees |

|

Step 4 |

Buy the chosen index funds |

Puts your cash to work in the actual global market |

1: Assess Your Risk Tolerance and Time Horizon

Before buying a single share, evaluate your personal financial reality. A younger investor with forty years until retirement easily handles a massive market crash. They have decades to recover and can buy more shares at a steep discount. An older investor approaching retirement simply cannot afford a massive portfolio drop. Ask yourself how you would physically react if your portfolio lost forty percent of its value in three months. If you would panic and sell, your risk tolerance ranks low. Your time horizon simply equals the number of years until you start withdrawing the money to live on.

2: Determine Your Asset Allocation

The ratio of stocks to bonds in your portfolio stands as the absolute most important decision you will make as an investor. It dictates nearly your entire risk and return profile for the rest of your life. You have to perfectly balance the need for high growth against your need for emotional stability. Once you pick a stock-to-bond ratio, you also need to decide how to split your stocks between the US and the rest of the world. Vanguard research typically suggests keeping 20% to 40% of your total stock allocation in international markets to get the full diversification benefit.

Aggressive Growth (Example: 80% Stocks / 20% Bonds)

This heavy stock allocation fits younger investors who want maximum long-term growth. An eighty percent stock and twenty percent bond split requires iron emotional discipline. You have to endure severe bear markets without selling a single share. You will experience massive dollar swings in your account value. But over a twenty-year period, the high stock concentration gives you the greatest mathematical chance of building serious generational wealth.

Moderate Growth (Example: 60% Stocks / 40% Bonds)

Millions of institutional and retail investors use this classic balanced portfolio. Historical data proves that a sixty percent stock and forty percent bond split captures a large chunk of the stock market upside. More importantly, it suffers substantially shallower losses during brutal financial crises. It hits the perfect middle ground for investors in their forties and fifties. They still desperately need growth but want a much softer landing when the global economy hits a recession.

Conservative Income (Example: 40% Stocks / 60% Bonds)

Retirees or highly risk-averse individuals usually choose a bond-heavy path to protect what they already built. A forty percent stock and sixty percent bond allocation shifts the goal line. You stop trying to get rich and focus on staying rich. Prioritizing strict capital preservation and steady bond yields over aggressive stock growth ensures your money lasts through your final years. It provides the literal peace of mind required to sleep well at night, no matter what the news anchors scream about.

3: Choose Your Brokerage Account

You need a reliable place to actually buy and hold these index funds safely. Strictly look for brokerages heavily known for low-cost investing, zero account minimums, and zero commission fees on standard trades. Vanguard, Fidelity, and Charles Schwab rule the industry as the undisputed heavyweights in this space. All three offer fantastic platforms, great customer service, and direct access to the exact funds you need. Your final decision really just comes down to which website interface you like best and whether you already bank with one of them.

4: Select the Right Index Funds or ETFs

Once your brokerage account sits fully open and funded with cash, make the actual purchase. You can build your three-fund portfolio using either traditional mutual funds or exchange-traded funds (ETFs). The underlying investments remain essentially identical. ETFs trade throughout the day like normal individual stocks. They also prove noticeably more tax-efficient in regular taxable brokerage accounts. Mutual funds only trade once a day after the market closes. However, they easily allow you to set up automatic monthly investments down to the exact penny. Pick the format that best fits your desire for automation.

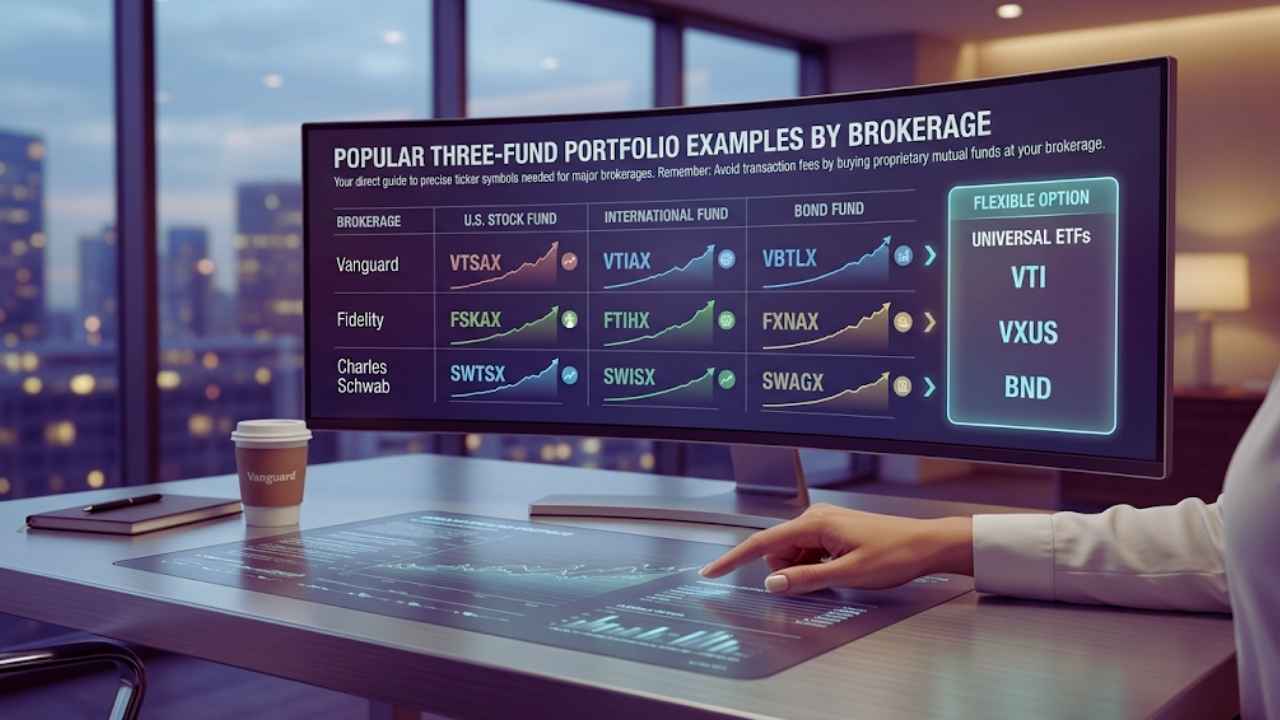

Popular Three-Fund Portfolio Examples by Brokerage

You never have to guess which specific funds to buy for this setup. The investing community mapped out the precise ticker symbols you need for every major brokerage on the market today. You absolutely must buy the proprietary mutual funds offered by your specific brokerage to avoid unnecessary transaction fees. If you use Fidelity, buy Fidelity funds. If you prefer the flexibility of ETFs, you get much more freedom. They usually trade fee-free across all modern platforms and traditional brokers alike.

|

Brokerage |

US Stock Fund |

International Fund |

Bond Fund |

|

Vanguard |

VTSAX |

VTIAX |

VBTLX |

|

Fidelity |

FSKAX |

FTIHX |

FXNAX |

|

Charles Schwab |

SWTSX |

SWISX |

SWAGX |

|

Universal ETFs |

VTI |

VXUS |

BND |

The Vanguard Approach

Vanguard stands as the historic pioneer of low-cost index investing and the spiritual home of this entire strategy. If you use their platform, buy VTSAX for your total United States stock exposure. In 2026, VTSAX carries a tiny 0.04% expense ratio. Use VTIAX for your total international stock exposure (0.09% expense ratio). For the bond portion, grab VBTLX (0.04% expense ratio). These operate as traditional mutual funds with a $3,000 minimum initial investment requirement per fund. Once you hit that minimum, easily set up an automatic transfer from your checking account every payday. Vanguard handles the rest without you lifting a finger.

The Fidelity Approach

Fidelity operates as a massive, highly aggressive competitor that actually beats Vanguard on some specific fund fees. Investors using Fidelity buy FSKAX for domestic stocks, FTIHX for international stocks, and FXNAX for the total bond market. Fidelity shines because their funds generally carry zero minimum investment requirements. They also offer a unique lineup of zero-fee mutual funds (like FZROX) for domestic and international exposure. These zero-fee funds look incredible, but only use them inside tax-advantaged retirement accounts to avoid nasty tax traps if you ever leave the brokerage.

The Charles Schwab Approach

Charles Schwab offers a highly polished web platform and incredibly cheap index funds for the modern investor. For the US stock market, use SWTSX. For the international portion, grab SWISX. Hold your bond allocation safely in SWAGX. Schwab structures its international mutual fund slightly differently than the others. SWISX primarily covers developed international markets and completely excludes emerging markets. If you want true emerging market exposure at Schwab, simply add a small position in an emerging markets exchange-traded fund.

The Universal ETF Alternative

If you strongly prefer the flexibility and tax advantages of ETFs, build the ultimate portable portfolio anywhere you want. Buy Vanguard ETFs at almost any modern brokerage completely free of transaction fees. Simply buy VTI for the total US market, VXUS for the total international market, and BND for the total bond market. These specific funds carry no real minimum investment since many brokers now let you buy fractional shares. This route stands as the absolute best choice if you invest in a regular taxable account and want to keep your tax bill tiny.

Historical Performance and Realistic Expectations

When you adopt a three-fund portfolio, you have to completely align your mental expectations with reality. You mathematically guarantee you will never wildly beat the global market average. Why? Because you effectively are the global market average. By gladly accepting average returns, you ironically destroy the vast majority of professional hedge fund managers over long timelines. Looking at real historical data helps you deeply understand normal market behavior. It keeps you from panic selling when things get a little choppy on the evening news.

|

Market Condition |

Expected Portfolio Behavior |

Investor Mindset |

|

Bull Market |

Steady compound gains across equities |

Stay humble and keep aggressively investing |

|

Bear Market |

Significant drops, but softened by bond yields |

Ignore the news and absolutely do not sell |

|

Decades-long |

Averages around typical market historical rates |

Trust the math of long-term compound growth |

Understanding Average Annual Returns

Financial advisors love to talk about stocks returning high single-digit averages every single year. While this remains a mathematical fact over a thirty-year timeline, almost no single calendar year actually delivers that exact average number. The market might jump massively one year, hit another massive rally the next, and drop heavily the year after that. For instance, in mid-2026, VTI posted a massive 1-year return of roughly 30%. But looking back at 2022, the same fund dropped roughly 19.5%. When you combine those wild swings over decades, it smooths out to a relatively predictable average return of around 8% to 10% before inflation. Mentally prepare yourself for wild, unpredictable swings to reap the final rewards at the end of your journey.

Surviving Drawdowns and Market Crashes

To achieve life-changing long-term growth, you must pay the absolute emotional toll of short-term pain. During historical stress periods like the 2008 global financial crisis, global stock markets lose immense amounts of value rapidly. A three-fund portfolio directly mitigates this destruction. Because you hold bonds, your total portfolio will not fall nearly as far as a pure stock portfolio. A backtest of the classic Bogleheads 80/20 portfolio spanning 1970 to 2026 shows its deepest drawdown hit roughly 44% compared to standard equities falling much further. The primary purpose of your bond allocation just reduces the bleeding. It keeps you from abandoning your investment strategy at the absolute worst possible time.

How to Manage and Rebalance Your Portfolio?

A lazy portfolio requires very little human effort, but it never stays entirely maintenance-free over its lifespan. Over time, the different index funds in your account grow at wildly different rates. This throws your carefully chosen target allocation completely out of whack. You have to perform a tiny amount of basic maintenance to keep your exact risk profile where you originally wanted it. Managing your accounts efficiently also means paying strict attention to where you place specific assets. You never want to give the government more of your money than legally necessary at tax time.

|

Management Task |

Frequency |

Purpose |

|

Rebalancing |

Once a year or at a set drift percentage |

Maintains your strict target risk level |

|

Tax-loss Harvesting |

During major market dips |

Offsets taxable capital gains |

|

Asset Location |

Setup phase and ongoing |

Minimizes your annual tax drag |

What is Rebalancing?

Rebalancing acts as the highly effective practice of selling your winners and buying your losers to maintain your original asset allocation. Imagine setting up an eighty percent stock and twenty percent bond portfolio. If the stock market goes on a massive multi-year run, your stocks might grow so fast they suddenly make up ninety percent of your account. You now carry way more risk than you intended. To fix this, sell some of your high-flying stocks and use that cash to buy more bonds. This resets the balance back to your original target. This brilliant mechanic forces you to buy low and sell high automatically.

When and How Often to Rebalance?

You do not need to constantly tinker with your account to keep it properly balanced throughout the year. In fact, checking your investments every day usually triggers massive anxiety and terrible decision-making. Most financial experts highly recommend checking the portfolio just once a year on a memorable date, like your birthday. Alternatively, use drift bands. This means you only rebalance if a specific fund drifts more than 5% away from its target allocation. If you add new cash every month, easily rebalance just by directing your new deposits toward whichever fund currently lags behind.

Asset Location and Tax Efficiency

Holding investments in both tax-advantaged retirement accounts and standard taxable brokerages lets you heavily optimize your entire setup. The industry calls this asset location. Bonds generate regular income through interest payments. The government taxes these payments heavily at your ordinary income rate. So, keep your bond funds sheltered safely inside a retirement account (like a traditional IRA or 401k) where taxes stay fully deferred. Conversely, highly tax-efficient equity ETFs like VTI generate very little taxable income. This makes them the perfect asset to hold in a standard taxable brokerage account.

Common Mistakes to Avoid

The pure math behind the three-fund portfolio looks flawless. But human beings act as wildly flawed creatures when money gets involved. Investors undeniably operate as their own worst enemies. We get bored easily, headlines scare us, and we constantly think we act smarter than the collective market. When you adopt a strict passive index strategy, your biggest daily job simply means getting out of your own way. Knowing the most common behavioral traps before you fall into them acts as the absolute best way to ensure your money keeps compounding steadily over the coming decades.

|

Common Mistake |

Why It Happens |

How to Avoid It |

|

Tinkering |

Boredom or chasing hot market trends |

Stick strictly to your three core index funds |

|

Panic Selling |

Fear of losing everything in a recession |

Stop looking at your account balance during downturns |

|

Yield Chasing |

Deep desire for immediate cash flow |

Remember that total return matters far more than dividends |

Tinkering and Overcomplicating

The intense temptation to add just one more specialized fund feels incredibly strong for new investors. You hear about a new sector fund. A coworker tells you about an amazing individual tech stock poised to explode. Before you know it, your clean three-fund portfolio morphs into a messy, overlapping fifteen-fund disaster with much higher fees. Reiterate to yourself daily that the immense strength of this strategy lies entirely in its boring simplicity. Every time you try to outsmart the market by adding complexity, you almost always end up hurting your long-term returns.

Panic Selling During Market Downturns

This sits as the ultimate psychological boss fight of long-term investing. You log into your brokerage account and see you lost a large sum of money in a single week. The primal part of your brain screams at you to sell everything and run to the safety of cash. Constantly remind yourself that paper losses only become a permanent reality if you actually hit the sell button. Broad market index funds historically recover from every single war, pandemic, and financial crisis in modern history. Turn off the financial news during turbulent times and trust the global economy.

Final Thoughts

Building generational wealth doesn’t require endless hours of stock charting, an expensive finance degree, or paying massive advisory fees to a wealth manager. By implementing a three-fund portfolio, you immediately take absolute control of your financial destiny using the most mathematically powerful tools available to everyday retail investors. You get maximum global diversification, incredibly low fees, and a rock-solid system that requires almost zero ongoing maintenance.

The absolute key to making this work relies entirely on your own consistency and patience. Start as early as you can, automate your deposits every single month, ignore the terrifying daily news cycle, and let the relentless math of compound interest carry your three-fund portfolio exactly where you want to go.

Frequently Asked Questions (FAQs) About Three Fund Portfolio Guide

Can I lose money in a three-fund portfolio?

Yes, all investing carries real inherent risk. The dollar value of your portfolio will absolutely drop during major economic recessions and global market crashes. You will definitely see negative red numbers in your account at some point in your life. However, over long timelines of ten to twenty years, broad market index funds historically always recover and generate immense wealth. The absolute risk of losing all your money hits virtually zero unless the entire global financial system collapses permanently. If that happens, cash won’t save you anyway.

Does a three-fund portfolio protect against inflation?

Yes, it acts as one of the best defenses against inflation ever created. Leaving your cash in a savings account guarantees you lose purchasing power over time. Owning equities gives you a stake in companies that raise their prices to match inflation. As the cost of living goes up, corporate earnings generally go up right alongside it. This drives your stock index funds higher over the long run, comfortably outpacing standard inflation rates.

Should I worry about currency risk with international funds?

When you buy an international fund, you hold assets priced in foreign currencies. If the dollar gets stronger, your international returns look slightly weaker, and vice versa. Experts call this currency risk. Most agree you do not need to hedge against this. Holding foreign currency exposure actually provides another excellent layer of diversification. It protects you in scenarios where the domestic currency suddenly loses value on the global stage.

What is the Core Four portfolio alternative?

If you spend enough time searching through investing forums, you will eventually see people discussing the “core four” portfolio. This simply takes a three-fund portfolio and adds one extra asset to it: a real estate index fund (REIT). Proponents of this approach argue that adding dedicated real estate exposure provides slightly better diversification against inflation. While it operates as a perfectly fine strategy, the standard approach already holds plenty of real estate companies within the total stock market fund. This makes the fourth fund entirely optional.

Should I include dividend-specific funds?

Many investors feel a strong urge to buy dividend-focused funds for the psychological comfort of regular cash flow. You really do not need to do this. A total stock market fund already includes every single dividend-paying company in the economy. By isolating just the dividend payers, you actually reduce your overall diversification. You miss out on massive growth companies that choose to reinvest their profits instead of paying dividends out to shareholders. Total return matters most, not just the dividend yield.

Why not just use a Target Date Fund instead?

Target-date funds essentially act as a three-fund portfolio managed entirely by the brokerage. They automatically shift your allocation from stocks to bonds as you get older. They represent the ultimate set-it-and-forget-it option. However, target-date funds often carry slightly higher expense ratios than individual index funds. By managing the three funds yourself, you maintain total control over your exact stock-to-bond ratio and minimize your annual fees.

{kind=link}