Planning for the years after you stop working looks entirely different today than it did for previous generations. The days of simply clocking into a factory for forty years and walking away with a guaranteed gold watch and a steady check are mostly behind us. Economic inflation, changing tax codes, and longer life expectancies force every worker to seriously rethink how they stash cash away for the future.

Understanding the landscape of Pension vs 401k 2026 rules is the first necessary step toward building a financial safety net that actually holds up under pressure. We are seeing massive legislative shifts this year that will immediately impact your paycheck today and dictate your comfort tomorrow. Whether you are navigating your first corporate job or closing in on your final working years, grasping how these retirement vehicles operate will determine if you spend your later years traveling or stressing over utility bills. You have to take control of your financial destiny right now.

|

Planning Area |

Current Status in 2026 |

Impact on Workers |

|

Tax Legislation |

SECURE 2.0 Act fully active |

Changes how catch-up contributions are taxed |

|

Economic Climate |

Higher costs of living |

Requires larger nest eggs to survive comfortably |

|

Employer Trends |

Phasing out old models |

Shifts more saving responsibility onto the employee |

|

Life Expectancy |

Steadily rising |

Demands a portfolio that can last thirty years |

The Core Basics: Defining the Two Major Retirement Vehicles

Before diving into the complex tax laws of 2026, we need to strip these two accounts down to their bare mechanics. Employers offer these programs to help you survive after you clock out for the last time, but they function like completely different machines under the hood. One operates like a massive communal trust fund managed by financial professionals, while the other acts like a personal vault you have to fill and guard yourself. Knowing the structural DNA of each system clarifies exactly why they behave so differently when the economy takes a wild turn. By understanding the core definitions, you can better prepare for the financial realities of your retirement years.

|

Feature |

Defined Benefit Plan |

Defined Contribution Plan |

|

Technical Name |

Pension |

401(k) |

|

Core Promise |

A set monthly income for life |

A tax-advantaged account to save money |

|

Management |

Run by institutional investors |

Run by the individual employee |

|

Modern Availability |

Mostly public sector and unions |

Dominant in the private corporate sector |

What Exactly is a Pension Plan?

A pension is legally classified as a defined benefit plan, meaning the benefit you receive at the end is strictly defined by a written formula. This formula usually multiplies your years of service by a specific percentage of your final average salary. When you hit a predetermined retirement age, the company or government agency starts sending you a check every single month until you pass away. Your employer does all the heavy lifting behind the scenes to make this happen.

The company takes its own operating cash, pools it with funds dedicated to all other eligible workers, and hands it over to professional asset managers. These managers invest in real estate, private equity, bonds, and stocks to ensure the trust fund grows large enough to cover everyone. You never have to worry about which specific stock is up or down on any given Tuesday. Your only job is to keep working for the company, put in your required years of service, and collect your check. You will mostly find these plans today if you work for the federal government, state agencies, public schools, or specific unionized manufacturing trades.

What Exactly is a 401(k) Plan?

A 401(k) is legally known as a defined contribution plan, and it gets its strange name from a specific subsection of the federal tax code. This plan does not promise you a single dime in retirement income. Instead, it strictly defines how much money you are allowed to contribute to the account while you are actively working. You tell your employer to slice off a percentage of your paycheck and route it directly into this personal account before you get a chance to spend it. Many companies throw in a financial sweetener called an employer match to encourage you to participate.

If you put in a dollar, they might chip in fifty cents, up to a certain limit of your total salary. Once the money hits your account, you log into an online portal and decide exactly where that cash goes. You might choose a target date fund that aligns with the year you turn sixty-five, or you might pick your own aggressive mix of stock and bond funds. The final amount of money you have when you finally quit working depends entirely on how much you saved, how much your company matched, and how well your chosen investments performed over the decades.

Key Differences Between Pensions and 401(k)s

To truly grasp the Pension vs 401k 2026 landscape, you have to look closely at the specific pressure points of each system. We have five main areas where these plans clash entirely in their approach to your money. They handle market risk, employee control, and future tax burdens in fundamentally opposite ways. If you understand these five distinct categories, you will be able to navigate any retirement conversation without getting lost in the financial jargon.

|

Comparison Point |

Pension Plan Mechanics |

401(k) Plan Mechanics |

|

Funding Source |

Mainly employer contributions |

Mainly employee paycheck deductions |

|

Market Risk |

Employer absorbs all losses |

Employee absorbs all losses |

|

Investment Control |

Zero employee control |

Complete employee control |

|

Payout Style |

Lifetime monthly annuity |

Lump sum you must manage yourself |

|

Job Portability |

Very poor; tied to one company |

Excellent; moves with you seamlessly |

Who Funds the Plan and How?

In a traditional defined benefit setup, the company writes the biggest checks to keep the system afloat. Professional actuaries calculate exactly how much cash the company must deposit every quarter to ensure there is enough money in the vault to pay all current and future retirees. While some government jobs do require workers to contribute a small, mandatory percentage of their pay toward the system, the overall health of the trust fund relies almost entirely on the employer.

In a defined contribution setup, your own personal discipline funds the account. If you never log into the human resources portal and set up a payroll deduction, your account will sit at zero forever. Even if a company offers a highly generous match, they will not give you the free money unless you put your own skin in the game first. You have to actively sacrifice your spending power today to build your own wealth for tomorrow.

Who Carries the Investment Risk?

This is the most intimidating part of financial planning for the average worker. Markets crash, global recessions hit, and inflation constantly eats away at your purchasing power. In a defined benefit system, the company or government takes all the punches. If the stock market tanks right before you retire, your promised monthly check stays exactly the same. The company is legally bound to inject more of its own operating cash into the trust fund to cover any severe investment losses.

In a personal retirement account, you stand entirely alone against the market. If a massive crash wipes out thirty percent of your portfolio the year you plan to retire, you have a massive problem on your hands. You might have to work three or four extra years just to recover those unexpected losses. You bear the entire burden of market volatility and sequence of returns risk.

Control Over Investments

Because your boss carries the ultimate financial risk with a defined benefit plan, they also hold all the power over the money. You cannot call the plan administrator and demand they move your specific share of the trust fund into emerging market tech stocks or real estate. The money is locked in a massive institutional strategy that you cannot touch, direct, or even see on a daily basis.

Your personal account, however, offers total freedom. You can log into your mobile app on a Sunday night and completely reallocate your entire portfolio. You can choose highly aggressive growth funds in your twenties and smoothly pivot to conservative government bonds in your sixties. For people who enjoy managing money and tracking their net worth, this level of total control is a massive psychological benefit.

Payout Structures and Tax Implications

When the finish line finally arrives, a defined benefit plan turns into a steady, reliable paycheck. You get a direct deposit into your checking account every single month for the rest of your natural life. Because this money was never taxed when it went into the communal trust fund, you pay ordinary income tax on every check you receive in retirement. Your personal account hands you a massive pile of money all at once when you hit age fifty-nine and a half.

You have to sit down and figure out how much you can safely withdraw each year without going entirely broke before you die. Withdrawals from a traditional pre-tax account are taxed as ordinary income just like a regular paycheck. However, modern accounts often offer a Roth option, which changes the tax math entirely by letting you pay taxes up front for completely tax-free withdrawals later in life.

Portability When Changing Jobs

People do not work for the same exact company for forty years anymore. We frequently jump from job to job to negotiate better salaries, chase better titles, or find remote work flexibility. Defined benefit plans actively punish this modern behavior. They require you to work for a set number of years just to earn the right to a partial payout, a concept legally known as a vesting schedule.

If you leave the job early, you get absolutely nothing. Your personal account travels with you effortlessly. The money you contribute out of your own paycheck is yours from day one. When you quit to take a better job, you simply roll the entire balance into an Individual Retirement Account or move it directly to your new employer’s plan. You never lose your compounding momentum just because you decided to change employers.

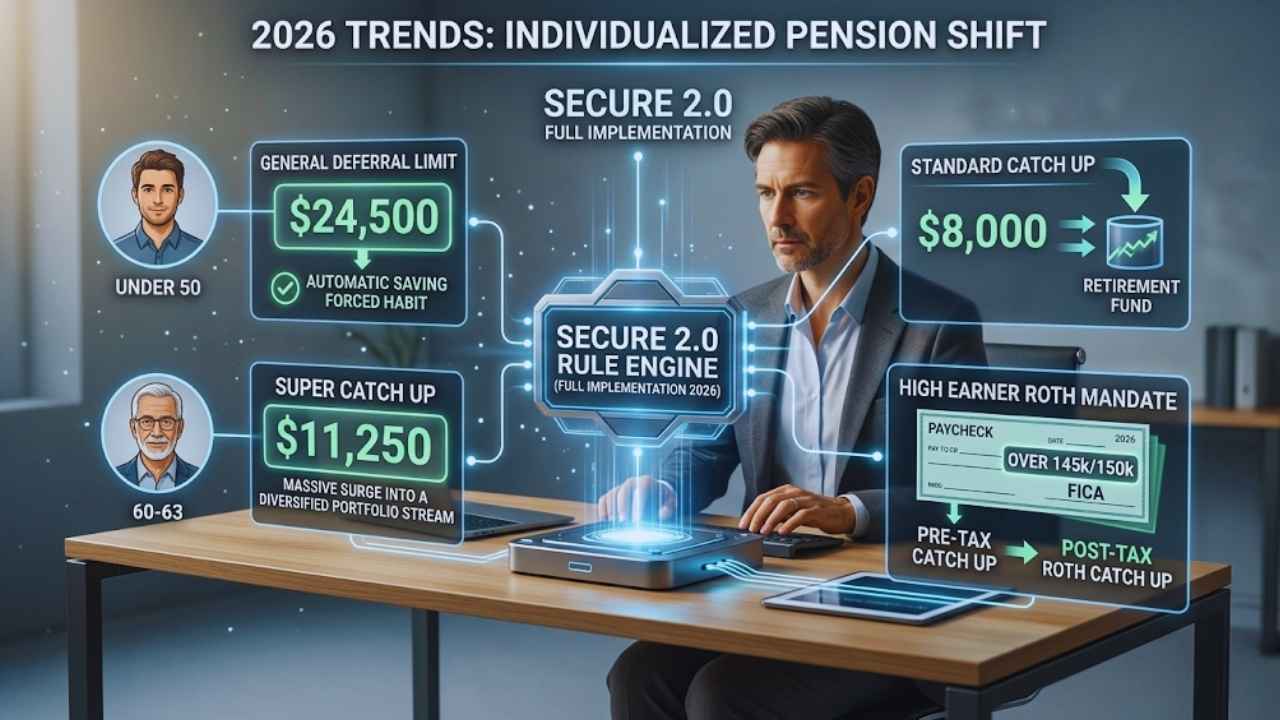

2026 Trends: The Shift Toward Individualized Pensions

The year 2026 brings massive changes to how ordinary people save their money. The federal government realizes that average citizens are struggling to build enough wealth on their own, so they have updated the rules to force better habits. We are seeing a distinct new trend where financial companies are trying to make your personal account act a little more like an old-school defined benefit plan. The fully implemented SECURE 2.0 Act is the main engine driving these sweeping adjustments across the corporate landscape. Understanding these changes is critical for anyone trying to maximize their Pension vs 401k 2026 strategy.

|

2026 Update |

Specific Rule Change |

Target Audience |

|

General Deferral Limit |

Increased to 24,500 dollars |

All active workers under fifty |

|

Standard Catch Up |

Increased to 8,000 dollars |

Workers aged fifty and older |

|

Super Catch Up |

Increased to 11,250 dollars |

Workers exactly aged 60 through 63 |

|

Roth Mandate |

High earner catch ups must be post tax |

Workers earning over 145k/150k FICA |

Higher Contribution Limits for 2026

Raging inflation over the past few years has forced the Internal Revenue Service to bump up exactly how much cash you can shelter from taxes. For 2026, an employee under the age of fifty can defer a massive 24,500 dollars into their workplace plan. This includes traditional pre-tax money, post-tax Roth money, or any combination of both up to the hard limit.

If you are lucky enough to get a generous company match or an annual profit-sharing bonus, the total combined limit of what you and your boss can shove into the account hits 72,000 dollars for the year. This gives highly disciplined and aggressive savers an incredible opportunity to stockpile wealth rapidly. Hitting these new limits consistently will virtually guarantee a comfortable, multi-million dollar retirement.

The SECURE 2.0 Act and Its Current Impact

The SECURE 2.0 Act passed a few years ago, but its most aggressive provisions finally bite hard in 2026. The most drastic change affects catch-up contribution limits for high earners. Normally, anyone over the age of fifty can throw an extra 8,000 dollars into their account to make up for lost time. But starting in 2026, if you made more than 145,000 dollars in FICA wages in the prior year, the government says your catch-up money must go directly into a Roth account.

You cannot claim a pre-tax deduction for that extra money anymore. The law also introduces a highly lucrative super catch-up window. If you are exactly 60, 61, 62, or 63 years old in 2026, you get a special deal. You can contribute an extra 11,250 dollars on top of the base limit, allowing older workers to sprint across the finish line right before they retire.

Lifetime Income Options Inside Your 401(k)

Wall Street knows perfectly well that regular people are absolutely terrified of running out of cash before they die. To fix this widespread fear, plan administrators are starting to embed insurance annuities directly into workplace plans in 2026. Instead of just buying standard stock and bond mutual funds, you can now check a box that funnels a portion of your paycheck into an insurance contract.

When you finally retire, this specific contract guarantees you a steady monthly check for life. It is the financial industry actively attempting to recreate the safety of a defined benefit plan inside a defined contribution shell. This individualized pension concept gives modern workers the absolute best of both worlds: total control over their growth savings and guaranteed baseline income for their strict living expenses.

The Pros and Cons of a Traditional Pension

Even though they are incredibly rare in the modern private sector, we need to look at why people still fight fiercely for jobs that offer these old-school benefits. They offer a specific type of psychological peace of mind that you cannot easily replicate on your own. But they also come with heavy strings attached that can trap you in a geographical location or a job you do not actually want. You have to weigh the massive security against the severe lack of personal freedom.

|

Factor |

Description |

Impact on Retiree |

|

Guaranteed Income |

Monthly checks never stop |

Eliminates fear of outliving money |

|

Market Immunity |

Wall Street crashes do not matter |

Massive reduction in financial anxiety |

|

Rigidity |

Locked into one company for decades |

Prevents career mobility |

|

Legacy |

Money disappears when you die |

Cannot leave the trust fund to your kids |

Advantages of Pensions

The biggest single perk is absolute financial certainty. You know exactly what your monthly income will be decades before you even decide to quit your job. This firm certainty allows you to budget your future life with extreme precision. You do not have to watch the financial news networks every morning and panic when interest rates change or the global economy dips into a severe recession.

Another massive advantage is the total lack of mental effort required on your part. Managing your own asset allocation, balancing risky bonds against aggressive tech stocks, and executing tax-loss harvesting are highly complicated chores. With a defined benefit plan, you do zero financial chores. The institutional money managers handle all the heavy lifting and stress for you.

Disadvantages of Pensions

The main fatal flaw is a complete lack of cash liquidity. If your house roof caves in or you suddenly face a terrifying emergency medical bill, you cannot ask the trust fund for a fifty-thousand dollar lump sum of cash. You are entirely stuck with your fixed monthly drip of income, which means you still need a massive separate emergency savings account to survive surprises. They also completely ruin your career flexibility.

To get a highly decent payout, you often have to dedicate twenty or thirty solid years to the exact same employer. If you get a terrible boss ten years in, you might feel financially trapped in a toxic building. Finally, these plans are historically terrible for building any sort of generational wealth. When you and your spouse eventually pass away, the monthly checks permanently stop. You cannot hand the institutional money down to your children or grandchildren.

The Pros and Cons of a 401(k) Account

The modern workplace savings plan has completely democratized the act of investing. It effectively turned millions of regular employees into part-owners of the biggest and most profitable companies on the planet. But it forcefully requires every worker to become their own chief financial officer, a complex job not everyone wants or knows how to successfully do. Managing this account properly requires intense discipline and a solid stomach for market volatility.

|

Factor |

Description |

Impact on Retiree |

|

Wealth Potential |

Uncapped growth via stock market |

Can create multi-million dollar nest eggs |

|

Legacy Building |

Account balance passes to heirs |

Excellent for generational wealth transfer |

|

Longevity Risk |

You might outlive your cash pile |

Requires careful withdrawal planning |

|

Hidden Costs |

Administrative and fund fees |

Quietly erodes your total return over time |

Advantages of 401(k)s

The potential to build massive, life-changing wealth is the absolute number one reason these accounts are incredible tools. Because you invest your cash directly in the broad stock market over several decades, your money compounds heavily upon itself. A disciplined saver who starts actively contributing in their early twenties can easily walk away with two or three million dollars by their sixties.

You also have total, unhindered access to your cash. While pulling money out early triggers nasty tax penalties, the reality is the money belongs strictly to you. If you reach full retirement age and want to buy a massive recreational vehicle with cash, you can simply withdraw eighty thousand dollars and just do it. Plus, whatever cash you do not spend gets passed directly to your kids or favorite charity when you die.

Disadvantages of 401(k)s

The incredibly heavy burden of getting it right rests entirely on your shoulders. If you panic and sell all your index funds during a terrifying market crash, you permanently lock in your losses and ruin your own future. Nobody is coming to magically save you if you make terrible financial choices along the way. Fees are also a quiet, brutal killer of your wealth. Many workplace plans hide excessive administrative fees and expensive mutual fund ratios deep inside their investment menus.

Paying just an extra one percent in obscure fees over thirty years will literally rob you of hundreds of thousands of dollars in compounded growth. You also face the terrifying math of human longevity. Figuring out how to safely make a pile of money last for thirty unknown years requires guessing market returns and future inflation rates almost perfectly.

Can You Have Both a Pension and a 401(k)?

Finding a standard job that offers both systems is like finding a mythical unicorn in the wild. It is incredibly rare in the modern private sector, but it absolutely does happen. Usually, federal government workers, public school teachers, or senior executives at massive legacy corporations get to enjoy this dual setup. If you find yourself in this highly specific situation, you have hit the absolute jackpot of personal finance and should guard that job closely.

|

Dual Setup |

How It Works |

Strategic Benefit |

|

Baseline Security |

Defined benefit covers survival costs |

Ensures you never go hungry or lose your house |

|

Growth Engine |

Personal account chases high returns |

Pays for luxury travel and leaves a legacy |

|

Tax Planning |

Mix of taxable checks and Roth money |

Gives you total control over tax brackets later |

|

Peace of Mind |

Best of both historical eras |

Reduces stress entirely |

The Ultimate Hybrid Scenario

Government employees frequently have easy access to a defined benefit trust fund along with a supplemental 457 or 403 plan, which behave exactly like a corporate defined contribution plan. In the private sector, some highly profitable companies offer a smaller cash balance plan alongside a standard matching account.

This hybrid model gives you an impenetrable, stress-free fortress of financial security. The guaranteed monthly check covers your exact mortgage, your weekly groceries, and your utility bills. Because your baseline survival is entirely secured by the employer’s promise, you can afford to take massive, calculated risks with your personal account to chase aggressive growth.

How to Manage Both Accounts Simultaneously

If you hold both accounts, you should firmly treat your personal account as pure risk capital. You do not need to buy slow, conservative bond funds inside your personal account because your guaranteed monthly check already acts like a massive, stable bond. You can confidently allocate your entire personal account to highly aggressive stock index funds.

You strictly use the guaranteed money to live on day-to-day, and you let the stock market money compound aggressively in the background. Later in life, you use that massive personal pile to pay for expensive vacations, help your kids buy their first houses, or fund high-end long-term medical care if you get sick.

Strategies for Maximizing Your Retirement Income Today

Whether you are fully locked into a rigid trust fund or navigating the wild west of the stock market entirely on your own, you need a battle plan. The new 2026 rules give you incredible, powerful tools to shelter your money, but you have to actively deploy them. Sitting back and lazily hoping for the best is a guaranteed path to old-age poverty. You must take aggressive action with every single paycheck to ensure your future self is comfortable.

|

Strategy |

Action Required |

Financial Benefit |

|

Employer Match |

Contribute enough to capture all free money |

Instantly doubles your initial investment |

|

Maximize Catch Ups |

Use the 8,000 or 11,250 limits if eligible |

Rapidly accelerates wealth in your final working years |

|

Roth Integration |

Pay taxes today for tax free growth |

Protects you against future tax rate hikes |

|

Fee Auditing |

Review your mutual fund expense ratios |

Keeps more compounded growth in your pocket |

Take Full Advantage of Employer Matches

If your current boss offers a match, capturing every single penny of it must become your absolute top financial priority. If they offer to match four percent of your salary, contributing only three percent literally means you are leaving part of your total promised compensation sitting on the table.

It is entirely free money that instantly guarantees a one hundred percent return on your investment before the stock market even opens for the day. In a modern economy where guaranteed payouts are rare, the employer match is the absolute closest thing you get to real corporate support for your retirement.

Utilize Catch-Up Contributions if Eligible

If you are behind on your saving goals, the new 2026 limits are your absolute lifeline. Turning fifty automatically unlocks the 8,000 dollar standard catch-up limit. If you fall perfectly into that golden 60 to 63 age bracket, finding a way to shove that extra 11,250 dollars into your account can drastically alter your final portfolio balance.

You must aggressively redirect your annual corporate bonuses, your federal tax refunds, and your yearly pay raises directly into these specific catch-up buckets. Utilizing these limits allows you to shelter massive amounts of income during your highest-earning years right before you stop working.

Diversify Your Tax Burden with Roth Options

Historically, almost everyone just used pre-tax accounts to simply lower their current tax bill for the year. But federal tax rates might go up drastically in the future to pay off the climbing national debt. Almost all modern workplace plans now offer a post-tax Roth option.

You willingly pay the income tax today, but every single dollar of market growth and every future withdrawal is completely tax-free forever. Building a calculated mix of pre-tax money and Roth money gives you incredible tactical flexibility when you finally retire. It allows you to pull cash from different buckets depending on exactly what the federal tax rates do over the next twenty years.

Final Thoughts

Navigating the complicated rules of Pension vs 401k 2026 requires understanding a very harsh truth. Nobody cares more about your financial future than you do. The historical era of massive companies taking complete care of their workers from hire to grave is mostly over. The heavy burden of survival rests firmly on the decisions you make with your paycheck today. You absolutely must embrace the tools the government currently gives you.

Maximize the new 2026 contribution limits, capture every single dime of your company match, and heavily consider using Roth options to shield yourself from future tax hikes. If you are lucky enough to have a guaranteed monthly check waiting for you, use it as a solid foundation to take smart, aggressive risks with your other investments. Build a highly proactive strategy today that guarantees you will never run out of options tomorrow.

Frequently Asked Questions (FAQs) About Pension vs 401k

What happens to my pension if my company goes bankrupt?

Private sector trust funds are heavily insured by a federal government agency called the Pension Benefit Guaranty Corporation. If your exact employer goes completely bankrupt and the trust fund is left totally empty, the government agency steps in to pay your monthly checks. However, the government strictly caps exactly how much they will pay out. Highly paid corporate executives might lose a massive chunk of their promised money, but average everyday workers usually get exactly what they expected.

What happens to my 401(k) if my company goes bankrupt?

Your personal account is completely insulated from your actual employer’s financial failures. The money absolutely does not sit in the company operating bank account. It securely sits in a separate legal trust managed by a massive third-party custodian like Fidelity or Vanguard. If your company closes its doors forever, your boss’s creditors legally cannot touch your retirement money. You simply roll the entire balance over to an Individual Retirement Account and keep moving forward with your life.

Can I cash out my pension early?

Some highly specific plans offer a massive lump-sum buyout option when you leave the company or hit a certain age marker. Instead of taking the monthly drip of checks, you take a giant pile of cash all at once. You can roll this cash directly into an IRA without paying any severe tax penalties. This move gives you total control over the money and your investments, but you completely forfeit the absolute safety of the guaranteed lifetime income.

Should I stop contributing to my 401(k) if the market drops?

Absolutely not under any circumstances. Stopping your automatic payroll deductions during a severe recession is the worst financial mistake you can possibly make. When the stock market crashes hard, the mutual funds you are buying are effectively on a massive fire sale. Continuing to invest your cash means you are forcefully acquiring more shares at much lower prices. When the broader economy eventually recovers, those incredibly cheap shares will drive the explosive, long-term growth of your total wealth.

Do I pay taxes on a pension vs 401k in 2026?

Yes, the Internal Revenue Service always makes sure they get their cut of your money. Guaranteed monthly checks from a trust fund are strictly taxed as ordinary income at your current tax bracket. Withdrawals from a traditional pre-tax personal account are also taxed completely as ordinary income. The absolute only way to escape taxes in retirement is if you specifically chose to use a Roth account and paid all the necessary taxes up front while you were still actively working.

Can I transfer my 401(k) into a pension plan?

Usually, the answer is a firm no. You cannot simply take your personal stock market money and dump it into an institutional trust fund to artificially buy a bigger monthly check. However, some specific state and local government plans do allow workers to purchase extra years of service credit using outside retirement funds. This is a very highly niche rule that applies only to certain public workers and practically never applies to the broad private corporate sector.

{kind=link}