Let’s be real. Logging into a new 401(k) or IRA portal feels like trying to read a foreign language. You stare at a massive list of ticker symbols, totally unsure of where you should park your hard-earned cash. For most of us, the decision quickly boils down to two heavyweights: an index fund vs target date fund.

Both options are wildly popular across the global investment world right now. Both give you instant diversification across thousands of companies. Both aim to build serious long-term wealth so you can eventually stop working. But they take completely different roads to get you to the finish line. One hands you the steering wheel, giving you ultimate control and dirt-cheap fees. The other acts as a financial chauffeur, automatically tweaking your risk as you age so you never have to lift a finger.

Picking the wrong one will not necessarily destroy your retirement. However, it could cost you thousands in hidden fees. It could also expose you to gut-wrenching volatility during a market crash. If you are stuck staring at your retirement dashboard, here is exactly how these two funds work, how they stack up, and which one actually belongs in your portfolio.

What is an Index Fund?

An index fund is a mutual fund or exchange-traded fund that simply tracks a specific financial market index. Instead of paying a guy in a suit to guess which stocks will go up, an index fund just buys all the stocks in a specific group. For example, it might track the S&P 500 or the Total Stock Market. Buy a Total Market index fund, and you instantly own a tiny slice of thousands of public companies.

The ultimate goal is not to beat the market. The goal is simply to match the market. Because the fund runs on autopilot without expensive stock analysts, the internal fees remain practically non-existent. You will find standard index funds charging just a tiny fraction of a single percent.

The catch is that your asset allocation stays exactly the same forever. If you buy a stock fund at age 25, it remains 100 percent stocks when you hit 65. If you want to reduce your risk as you get older, you have to log in, sell some shares, and buy bonds yourself. You are the one who steers the ship.

|

Feature |

Index Fund Details |

|

Core Strategy |

Passively tracks a specific market index |

|

Average Fees |

Extremely low (often under 0.05 percent annually) |

|

Asset Allocation |

Static (never changes unless you intervene) |

|

Effort Level |

Requires manual rebalancing as you age |

|

Risk Level |

Varies strictly based on the specific index you pick |

What is a Target-Date Fund?

A target-date fund is the ultimate set-it-and-forget-it investment vehicle. It revolves completely around a single number, which is the exact year you plan to quit working. If you want to retire around 2055, you just dump all your cash into a “Target Retirement 2055” fund. Behind the scenes, a target-date fund is actually a fund of funds. The fund takes your money and divides it across several underlying index funds.

It automatically splits your cash between domestic stocks, international stocks, and fixed-income bonds. The magic lies entirely in its internal clock. When you are young, the fund buys mostly stocks to capture maximum market growth.

As you inch closer to your target year, the fund manager automatically sells those volatile stocks and buys safer bonds. By the time you actually throw your retirement party, the portfolio is highly conservative. This automated system actively shields your money from sudden market crashes when you need the cash the most.

|

Feature |

Target-Date Fund Details |

|

Core Strategy |

Automated risk management tied to your target retirement year |

|

Average Fees |

Moderate (averages 0.27 percent annually as of 2026) |

|

Asset Allocation |

Dynamic (automatically shifts from stocks to bonds) |

|

Effort Level |

Zero (fully automated portfolio management) |

|

Risk Level |

Starts aggressive, becomes highly conservative over time |

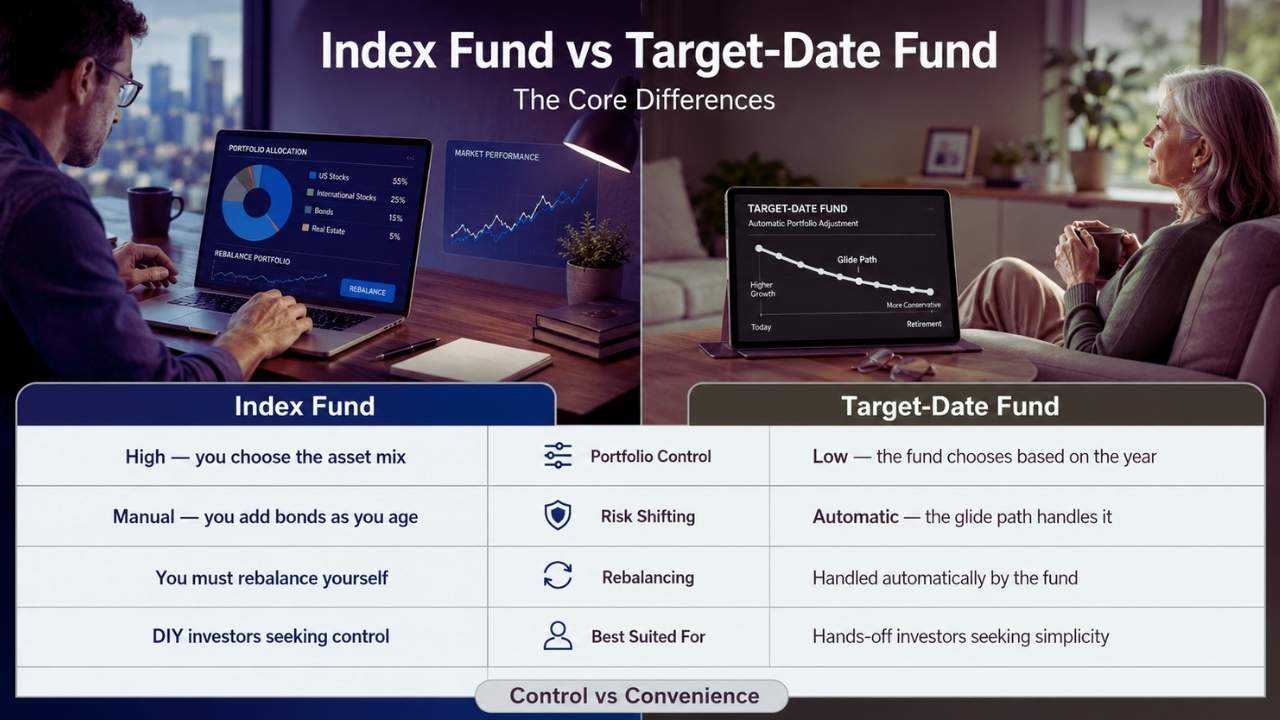

Index Fund vs Target Date Fund: The Core Differences

When sizing up an index fund vs target date fund, the battle really comes down to control versus convenience. An index fund demands that you act as your own portfolio manager. You decide the exact split between domestic stocks, international markets, and bonds. Over time, stocks usually grow much faster than bonds, causing your portfolio to rapidly drift out of balance.

If a bull market pushes your stock allocation too high, you have to log in and sell off the winners. You then buy more bonds to get back on track. We call this rebalancing, and it requires serious financial discipline. A target-date fund handles all of that complicated math for you. It rebalances automatically on a daily basis.

If stocks surge, the fund trims them and buys bonds to maintain the exact risk profile required for your specific age. You pay a slightly higher fee for this, but it completely removes human emotion from the equation. You will not panic-sell during a recession because the fund managers quietly do the heavy lifting in the background.

|

Comparison Point |

Index Fund |

Target-Date Fund |

|

Portfolio Control |

High (you dictate the exact asset mix) |

Low (the fund decides everything based on the year) |

|

Risk Shifting |

Manual (you must buy bonds as you age) |

Automatic (the built-in glide path handles it) |

|

Rebalancing |

Requires your active intervention |

Handled continuously by the fund manager |

|

Best Suited For |

DIY optimizers seeking maximum returns |

Hands-off investors wanting total peace of mind |

The Anatomy of a Glide Path (2026 Trends)

To really understand target-date funds, you have to understand the glide path. Think of it as a carefully scheduled flight plan. It is the exact path the fund uses to shift your money from stocks to bonds over a 40-year window. Right now, this specific market holds a staggering 4.8 trillion dollars in assets. Because inflation keeps eating away at purchasing power, fund managers have actually grown more aggressive lately.

They know you need aggressive growth to survive a 30-year retirement period. Today, if you are 45 years away from retirement, the average target-date fund drops 93 percent of your cash into global equities and just 7 percent into bonds. Once you hit your late 40s, the glide path steepens dramatically.

The fund starts aggressively converting your stock holdings into fixed-income assets. By age 65, you usually sit at an even split between stocks and bonds. Some funds keep gliding downward even after you stop working. They eventually settle around a 30 percent stock mix to safely fund your grocery bills and vacations without excessive risk.

|

Age Phase |

Typical Stock Allocation |

Typical Bond Allocation |

Primary Goal |

|

20s to 30s |

90 to 95 percent |

5 to 10 percent |

Maximize long-term capital growth |

|

40s to 50s |

70 to 80 percent |

20 to 30 percent |

Balance growth with moderate volatility |

|

Age 65 (Target) |

45 to 55 percent |

45 to 55 percent |

Preserve capital and generate income |

|

In Retirement |

30 to 40 percent |

60 to 70 percent |

Shield against market crashes and inflation |

Breaking Down Expense Ratios and Hidden Costs

Fees ultimately determine exactly how much of your money actually goes to work for you. We call this the expense ratio. An expense ratio of 1.00 percent means you pay 100 dollars a year for every 10,000 dollars you invest. Standalone index funds remain the cheapest products on Wall Street right now. Broad-market index funds from heavyweights like Vanguard or Fidelity cost almost nothing.

Vanguard’s S&P 500 ETF charges just 0.03 percent annually. Fidelity’s Total Market fund charges a microscopic 0.015 percent. Target-date funds cost more because you pay for that automated glide path. However, current data shows the average target-date mutual fund fee sits at a reasonable 0.27 percent.

A fraction of a percent sounds completely harmless, but it compounds brutally over a long career. Say you invest 500 dollars a month for 30 years. An ultra-low index fund fee costs you a few thousand dollars over your life. A higher target-date fee drains tens of thousands of dollars from that exact same balance.

|

Fee Level |

Example Fund Type |

Estimated Cost Over 30 Years (on $500/mo) |

|

0.00 to 0.04 percent |

Standard S&P 500 Index Fund |

0 to 2,500 dollars |

|

0.15 to 0.27 percent |

Low-Cost Target Date Index Fund |

9,000 to 16,000 dollars |

|

0.40 to 0.60 percent |

Active Target Date Fund |

23,000 to 33,000 dollars |

|

0.75+ percent |

Legacy Retail Mutual Funds |

40,000+ dollars |

Behavioral Finance: Beating Your Own Brain

Numbers look great on spreadsheets, but investing happens in the real world where we all panic. The absolute best argument for a target-date fund is behavioral protection. When the stock market crashes by 20 percent in a single month, your brain screams at you to sell everything. You want to hide your money in cash to stop the bleeding. With a standalone index fund, you have the total power to hit the sell button and lock in massive losses.

Even worse, a pure index strategy requires you to rebalance during a crash. This means you have to actively buy more stocks while the market is burning to the ground. Very few regular people have the guts to do that.

Target-date funds completely remove you from the cockpit. Because they trade under a single ticker symbol, you do not see your individual stock holdings bleeding red. The algorithm mechanically buys and sells based on the glide path, completely ignoring market panics.

|

Investment Behavior |

Index Fund Investor |

Target-Date Fund Investor |

|

During Market Highs |

Tempted to stop buying bonds and chase stock returns |

Fund forces profits into safer bonds |

|

During Market Crashes |

Tempted to panic sell stocks; struggles to rebalance |

Fund automatically buys cheap stocks to rebalance |

|

Ongoing Maintenance |

Requires logging in, doing math, and placing trades |

Requires literally zero action |

|

Psychological Stress |

High |

Low |

Tax Efficiency and Asset Location

Where you hold your funds matters just as much as what you buy. If you get your asset location wrong, the IRS will make you pay for it heavily. Target-date funds create an absolute nightmare in normal taxable brokerage accounts. Because the manager constantly sells winning stocks to buy bonds, those internal sales generate continuous capital gains.

By law, those financial gains pass straight to you. If you hold a target-date fund in a standard taxable account, you get a surprise tax bill every single year. You owe money even if you never sold a single share yourself. Index funds remain incredibly tax-efficient by comparison. A standard index fund rarely sells any stocks.

It only swaps them out when a company drops out of the designated index list. The golden rule is incredibly simple here. You must keep target-date funds locked inside tax-advantaged accounts like a 401(k) or an IRA. You should put your standard index funds in your taxable brokerage accounts.

|

Account Type |

Target-Date Fund Suitability |

Index Fund Suitability |

|

401(k) / 403(b) |

Excellent (Gains are tax-sheltered) |

Excellent (Gains are tax-sheltered) |

|

Traditional / Roth IRA |

Excellent (Gains are tax-sheltered) |

Excellent (Gains are tax-sheltered) |

|

Taxable Brokerage Account |

Poor (Generates annual tax drag) |

Excellent (Highly tax-efficient) |

The DIY Route: The Three-Fund Portfolio

If you hate paying management fees but still want target-date diversification, you can easily build it yourself. Personal finance experts famously call this the Three-Fund Portfolio. Instead of buying a single Target Retirement fund, you buy three dirt-cheap index funds.

You need a total domestic stock fund, a total international stock fund, and a total bond market fund. You set the mix entirely based on your own gut and risk tolerance. At age 30, you might go with 60 percent domestic stocks, 30 percent international, and 10 percent bonds. Once a year, you log into your account for ten minutes to check the balances.

If domestic stocks had a killer run and hit 75 percent of your portfolio, you simply sell a little bit. You then buy bonds to get right back to your target mix. This setup drops your fees all the way to the floor. You keep thousands of extra dollars in your pocket over the decades.

|

Management Strategy |

Required Holdings |

Primary Advantage |

Primary Drawback |

|

Automated (Target-Date) |

1 Target-Date Fund |

Requires zero time or financial knowledge |

Higher expense ratios drag down overall returns |

|

DIY (Three-Fund Portfolio) |

3 Individual Index Funds |

Lowest possible fees; maximum control |

Requires discipline to manually rebalance annually |

Institutional Shifts: The Rise of CITs in 2026

If you look closely at your employer retirement plan today, you will notice a massive industry shift. The target-date fund structure is rapidly moving away from old-school mutual funds. According to recent market data, Collective Investment Trusts now hold over 54 percent of all target-date assets. A Collective Investment Trust is basically an unregistered investment vehicle built strictly for institutional retirement plans.

Because these trusts dodge the heavy regulatory and marketing costs of retail mutual funds, they offer the exact same glide path at a massive discount. You might see a target-date trust inside your account charging just 0.15 percent instead of a standard mutual fund charging 0.40 percent.

If you have access to one of these low-cost options, you should absolutely jump on it. It perfectly bridges the gap between target-date convenience and index-fund pricing. Five massive financial firms currently control roughly 80 percent of this entire specialized market.

|

Fund Structure |

Availability |

Cost Profile |

Regulatory Oversight |

|

Retail Mutual Fund |

Available to everyone (IRAs, Brokerages) |

Moderate to High |

Regulated by the SEC |

|

Collective Investment Trust (CIT) |

Exclusive to employer plans (401k) |

Very Low |

Overseen by banking regulators |

Which Strategy Fits Your Investing Style?

Choosing the absolute winner in the index fund vs target date fund debate comes down to brutal honesty. You have to know your own habits, your free time, and your panic threshold. You should grab an index fund if you demand absolute control over your money and refuse to pay a single unnecessary fee. You also need the iron stomach to log in and buy stocks during a terrifying recession.

Conversely, you should grab a target-date fund if you find investing incredibly boring. It is perfect if you want to check your account once a year and do absolutely zero math. It is also the right choice if you know you will make terrible choices when the market drops rapidly. A lot of smart folks actually run a hybrid model to get the best of both worlds.

They put their workplace retirement account entirely into a target-date fund so the main nest egg runs on autopilot. Then, they open a separate account to buy pure stock index funds for extra growth.

|

Investor Profile |

Best Investment Choice |

Why It Fits |

|

The Hands-Off Saver |

Target-Date Fund |

Stops decision paralysis; ensures diversification. |

|

The Optimizer / DIYer |

Standalone Index Funds |

Precision tuning; eliminates the management fee. |

|

The Anxious Investor |

Target-Date Fund |

Removes the emotional burden of market crashes. |

|

The Taxable Account Holder |

Standalone Index Funds |

Dodges the annual tax hit from internal rebalancing. |

Final Thoughts

Picking a clear winner in the index fund vs target date fund debate should not keep you up at night. Both vehicles completely crush trying to pick individual stocks on your own. Both options absolutely leave standard savings accounts in the dust. If you want total control, zero tax drag, and the lowest fees on earth, you should build a DIY portfolio of index funds.

If you want a perfectly diversified machine that manages risk while you sleep, the target-date fund is arguably the best invention in modern finance. Look at your own personal habits, check the exact fees in your employer plan, pick a designated path, and keep buying every single month.

Frequently Asked Questions (FAQs) About Index Fund vs Target Date Fund

Can I lose money in a target-date fund?

Absolutely. They rely heavily on the stock market. Even on the day you retire, the fund still holds 40% to 50% in stocks to outpace inflation. If the market crashes the week you retire, your target-date fund drops too—just not as hard as a pure index fund.

Can I buy a target-date fund for a totally different year?

Yes, and people do it all the time to “hack” the glide path. If you plan to retire in 2040, but you want a highly aggressive portfolio, just buy a 2060 fund. The manager treats you like a 25-year-old and keeps your money in high-growth stocks way longer.

Should I buy multiple target-date funds to diversify?

No. Please don’t do this. A single target-date fund already owns thousands of stocks and bonds globally. Buying a 2045 fund and a 2050 fund doesn’t make you more diversified; it just makes your portfolio a disorganized mess. Pick one year.

Are Vanguard index funds better than Fidelity target date funds?

You are comparing apples to oranges here. Both companies rock. Vanguard practically invented low index fees. Fidelity offers literal zero-fee index funds and stellar target-date options. Ignore the brand name on the label and look straight at the expense ratio. Find a fund charging less than 0.15% if you can.

{kind=link}