Planning for your financial future often feels like trying to hit a moving target while wearing a blindfold in the middle of a storm. You spend decades working incredibly hard, saving money, and investing heavily so you can eventually step away from your career and enjoy your life. Once that day finally arrives, a massive and highly stressful question hangs over your head.

How much money can you actually pull out of your investment accounts each year without going broke before you pass away? For several decades, the financial advisory industry handed out a very simple, one-size-fits-all answer to calm the nerves of anxious investors. They told absolutely everyone to just rely on the standard four percent withdrawal strategy and stop worrying about the math.

But times change rapidly, and we live in a completely different global economic reality today than we did thirty years ago. We now have to deal with unpredictable inflation spikes that destroy purchasing power, wild stock market swings driven by algorithmic trading, shifting tax brackets, and the simple fact that modern medicine is helping people live much longer than they used to. All these modern factors force retirees and financial planners to completely rethink this classic piece of advice. This brings up the core question regarding the 4 percent rule retirement 2026 guidelines that everyone is searching for right now. Does this old mathematical trick still hold up today, or is it outdated advice that might completely ruin your golden years and force you back to work?

Let us break down everything you need to know to protect your wealth right now. We will look at exactly where the rule came from and why current market conditions test its absolute limits on a daily basis. We will thoroughly review the absolute latest data from top financial institutions regarding safe withdrawal rates in the modern economy. Most importantly, we will explore advanced alternative strategies to make sure your hard-earned money lasts exactly as long as you need it to, regardless of what the stock market decides to do tomorrow.

What Is the 4 Percent Rule?

Before we can accurately judge if this financial concept still works in the modern economy, we have to understand exactly what it is and where it originated. The idea is incredibly straightforward on the surface, which completely explains why it became so universally popular among both financial advisors and everyday investors. The basic premise assumes you can withdraw exactly four percent of your total retirement savings during your very first year of not working.

You then adjust that exact dollar amount upward for inflation every single year after that, completely ignoring what the stock market is doing. If you follow this math strictly without deviating, your money should theoretically last for at least thirty years. We will look at the origins and the exact mathematical breakdown below to see how the mechanics operate in a real-world scenario.

|

Concept Area |

Core Details |

|

Core Idea |

Withdraw four percent in year one and strictly adjust for inflation annually |

|

Time Horizon |

Specifically designed to make a portfolio last exactly thirty years |

|

Original Source |

Created by financial planner William Bengen in the early nineteen nineties |

|

Portfolio Mix |

Assumes a rigid and even split between equities and intermediate bonds |

The Origins of the 4 Percent Rule

You might naturally assume this massive financial guideline came from a giant Wall Street bank or a prestigious university economics department. It actually came from one single, independent financial advisor named William Bengen working in Southern California. Back in the early nineteen nineties, Bengen simply wanted to give his clients a mathematically sound answer when they constantly asked how much they could safely spend without going broke. He gathered historical market data going all the way back to the nineteen twenties to run his own rigorous tests.

He studied how portfolios survived during major market crashes, the Great Depression, and the massive inflation spikes of the nineteen seventies. Bengen discovered that a retiree holding a portfolio split evenly between large-cap stocks and intermediate government bonds could safely withdraw four percent initially. By adjusting for inflation annually, the retiree never ran out of money over a thirty-year span in any historical scenario he tested. In every single simulation he ran based on past data, the money survived perfectly. Thus, the classic withdrawal guideline was born, and it quickly became the absolute gold standard of retirement planning across the entire global financial industry.

How the Math Actually Works?

The math behind the strategy is beautifully simple, which is perfect for doing quick mental calculations on a notepad. Imagine you reach your official retirement day with a well-diversified portfolio valued at exactly one point two million dollars. According to the original rule, you withdraw four percent of that initial starting balance in year one. That calculation gives you forty-eight thousand dollars in cash to live on for the next twelve months. When year two rolls around, you do not calculate four percent of your new portfolio balance, which is where most people get confused. Instead, you take your original forty-eight thousand dollars and increase it by the current rate of official inflation.

If inflation hits three percent over that first year, you simply add three percent to your original forty-eight thousand dollars. Your required withdrawal for year two becomes forty-nine thousand four hundred and forty dollars. In year three, if inflation drops back down to two percent, you add two percent to the previous amount, bringing your new withdrawal to fifty thousand four hundred and twenty-eight dollars. You repeat this precise process every single year to keep your purchasing power exactly the same, regardless of what the stock market is doing on any given day.

Why 2026 Market Conditions Are Challenging the Rule?

While the original historical research was completely groundbreaking thirty years ago, the financial landscape looks vastly different today in almost every measurable category. The classic mathematical formula was tested entirely against past market data, but people retiring today have to survive future economic conditions that look nothing like the twentieth century.

Several critical factors in our modern economy are putting serious strain on traditional withdrawal models and breaking the old calculators. Inflation acts differently now, markets move much faster due to technology, and the out-of-pocket cost of healthcare continues to rise far beyond normal baseline inflation rates. These modern economic realities absolutely require a fresh look at how we pull money from our investment portfolios.

|

Market Challenge |

Direct Impact on Retirement Portfolios |

|

Inflation Spikes |

Forces higher absolute dollar withdrawals during severe down markets |

|

Sequence Risk |

Early market crashes permanently damage long-term portfolio compounding |

|

Life Expectancy |

Living longer means the saved money has to stretch significantly further |

|

High Valuations |

Highly expensive stocks today often lead to much lower future return rates |

The Ongoing Threat of Inflation and Cost of Living

One of the biggest lessons learned over recent years is that inflation is rarely a smooth, predictable line on a chart. While the traditional model technically accounts for inflation through annual adjustments, massive unexpected spikes in the cost of living can deeply damage an investment portfolio. When the prices of daily groceries, specialized healthcare, and property taxes skyrocket, adjusting your withdrawal amount upward means you are pulling significantly more money out of your accounts just to survive the month. If this sudden spike happens while the stock market is simultaneously performing poorly, you face an absolute nightmare scenario mathematically.

You are forced to sell off a much larger number of underlying shares simply to maintain your baseline standard of living and pay your bills. Once those shares are sold to buy groceries, they are gone forever and can never benefit from a future market recovery. This compounding negative effect permanently destroys your wealth base from the inside out. It is one of the primary reasons modern financial planners get incredibly nervous when clients blindly rely on automatic inflation adjustments without considering their actual investment performance.

Market Volatility and Sequence of Returns Risk

The specific timing of your retirement date matters just as much as the actual amount of money you managed to save over your career. This terrifying concept is known as sequence of returns risk, and it is easily the single most dangerous threat to a brand new retiree. Imagine two different people who both retire on the exact same day with one million dollars in the bank. The first person retires right before a massive five-year bull market takes off. Their portfolio grows so rapidly that even with regular monthly withdrawals to pay for their lifestyle, their total account balance continues to increase year after year. The second person retires right before a major, unexpected global market crash hits the economy.

Their portfolio drops by a massive twenty percent in the very first twelve months. Because they still absolutely need to withdraw their forty thousand dollars to survive and buy food, they drain their account at an accelerated pace while the balance is already severely depressed. Even if the broader market eventually recovers and averages a solid historical return over the next thirty years, the second person might still go entirely broke. They run out of money simply because the bad years happened at the very beginning of their timeline when they were most vulnerable. In the current interconnected global economy, this sequence risk remains incredibly high for everyone.

The Reality of Increasing Life Expectancy

The original research framework was built entirely around a strict thirty-year retirement horizon to keep the math clean. Assuming someone retires at the traditional age of sixty-five, the money theoretically only needs to last until they reach age ninety-five. However, modern advancements in medical technology, pharmaceuticals, and healthier daily habits are pushing life expectancies much further out than anyone predicted in the nineteen nineties. Recent actuarial studies in the medical community heavily suggest that an increasing number of healthy people retiring today will easily live past the age of one hundred.

If you decide to join the early retirement movement and quit working at age fifty-five or sixty, or if you simply live an exceptionally long life due to good genetics, a thirty-year timeline is nowhere near enough to keep you financially safe. When you stretch the time horizon to thirty-five or forty full years, the mathematical safety of withdrawing a flat four percent drops off a cliff. A longer life automatically means more years of compounding inflation eating away at your purchasing power. It also mathematically guarantees you will experience more severe economic recessions and devastating market crashes along your journey.

Lower Bond Yields and High Equity Valuations

The original math relied heavily on a portfolio split evenly between large stocks and government bonds to smooth out the bumpy ride. Back in the mid-nineties when the rule was written, bonds paid incredibly generous and reliable yields. It was extremely common to see safe government bonds yielding six or seven percent without taking on any real risk at all. Today, the economic situation is drastically different across the entire fixed-income landscape. While bond yields have fluctuated up and down recently, they remain generally lower than historical averages from the last century, failing to keep up with true inflation.

At the exact same time, the stock market has enjoyed tremendous historical growth, leading many top financial analysts to argue that equities are currently priced for absolute perfection. If stocks are priced exceptionally high today based on current earnings, financial history tells us quite clearly that future returns over the next decade might be much lower than average. A combination of low bond yields that fail to generate enough cash and muted future stock returns creates a very difficult environment for generating sustainable passive income.

What the Latest Research Says for the 4 Percent Rule Retirement 2026

Because the economic environment shifts so dramatically from decade to decade, major financial institutions continuously update their research on safe withdrawal rates to protect their wealthy clients. They run millions of simulated market scenarios using massive supercomputers to see exactly how different spending levels hold up against modern economic projections.

These advanced stress tests are called Monte Carlo simulations, and they give us a very clear, mathematically sound picture of what is actually safe right now. Let us look incredibly closely at what the absolute best financial experts are saying about spending your money safely today.

|

Research Source |

Recommended Starting Rate |

Core Strategy Note |

|

Morningstar Data |

3.9 Percent Baseline |

Strictly assumes a thirty-year fixed inflation withdrawal plan |

|

Bill Bengen Update |

4.7 Percent Maximum |

Absolutely requires a highly diversified asset allocation model |

|

Vanguard Research |

4.0 to 5.0 Percent |

Requires heavy flexible spending during severe bear markets |

Morningstar’s 3.9 Percent Baseline

Morningstar is widely considered one of the absolute most authoritative voices on retirement income planning anywhere in the global financial sector. They publish a highly anticipated annual State of Retirement Income report that professional planners use constantly to guide their clients. In their deep research updated specifically for the 2025 and 2026 planning cycles, they suggest that the new absolute baseline safe withdrawal rate is roughly 3.9 percent. This specifically assumes a strict thirty-year timeline, a demanding ninety percent probability of complete success, and a traditional balanced portfolio of stocks and bonds.

While 3.9 percent looks very close to the original historical four percent, Morningstar stresses a highly critical point that most people miss entirely. This number is merely a safe starting point for stubborn people who demand a completely fixed, inflation-adjusted income every single year without exception. They note heavily that taking a slightly more conservative approach upfront helps protect against the much lower future market returns their internal analysts currently predict for the upcoming decade.

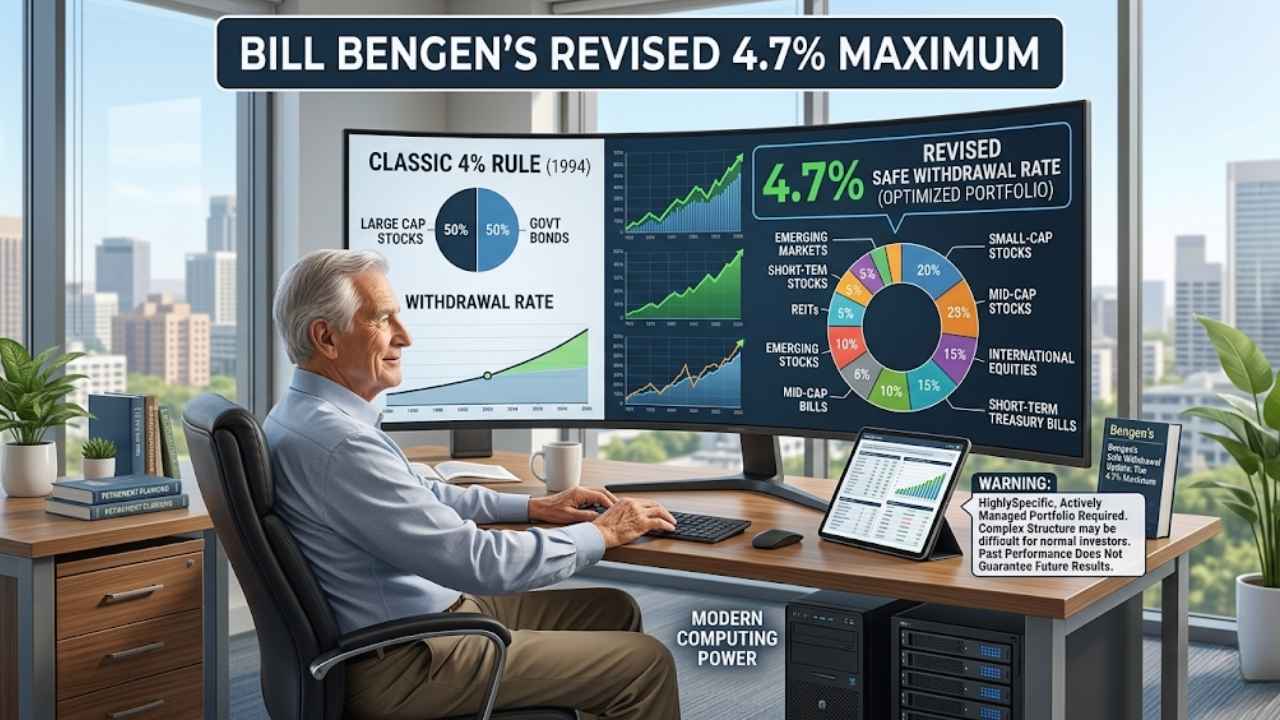

Bill Bengen’s Revised 4.7 Percent Maximum

Interestingly enough, the original creator of the traditional rule actually took the time to update his own historical findings recently using modern computing power. In his later research and writing, William Bengen boldly argued that retirees can actually afford to withdraw more money if they diversify their portfolios much better than the original fifty-fifty split. By intentionally adding different asset classes like small-cap stocks, mid-cap stocks, international equities, and short-term treasury bills to the standard mix, Bengen calculated a much higher safety net.

Under his newly revised calculations with a perfectly optimized portfolio, the absolute worst-case scenario safe withdrawal rate actually rises to roughly 4.7 percent. However, Bengen is very quick to point out in his interviews that this elevated rate relies entirely on a highly specific and actively managed portfolio structure that most normal people struggle to maintain. It also depends entirely on looking at historical data, which may not perfectly predict our future economy. Still, his highly updated math offers a brilliant beacon of hope for people who feel heavily squeezed by overly conservative estimates.

Vanguard’s 4.0 Percent Flexible Approach

The massive and highly respected investment firm Vanguard recently published its own incredibly deep analysis of modern withdrawal strategies for retirees. They concluded firmly that the original four percent concept is still perfectly viable today, but only if you accept one massive and uncomfortable caveat. They argue the math only works if retirees are entirely willing to be highly flexible with their monthly spending habits when the economy turns sour.

According to Vanguard analysts, the idea of blindly increasing your withdrawal amount every single year simply because of inflation is fundamentally flawed and highly dangerous. If the stock market drops by a painful twenty percent, taking an inflation raise is the absolute worst possible thing you can do to your shrinking money. Instead, they strongly suggest that retirees who are willing to temporarily cut their discretionary spending during bad market years can comfortably start at four percent or even higher. Being flexible with your lifestyle choices practically guarantees you will never run out of funds.

The Biggest Flaws of the Traditional 4 Percent Rule

Regardless of whether the exact correct mathematical number should be three point nine or four point seven, the entire framework of the traditional rule has several glaring and dangerous flaws. You absolutely have to understand these hidden traps clearly before you ever decide to quit your job and rely on your investments.

Relying on an old, rigid formula as absolute gospel without looking deeply at your personal daily life is a fast recipe for total disaster. The simple math unfortunately ignores some of the absolute most expensive realities of growing older in the modern world.

|

Flaw Category |

Why It Completely Breaks the Math |

|

Hidden Costs |

Completely ignores federal income taxes and advisor management fees |

|

Lifestyle Changes |

Falsely assumes you spend the exact same amount at age 90 as age 65 |

|

Investment Mix |

Fails completely if you emotionally hold too much cash or too many stocks |

It Completely Ignores Taxes and Investment Fees

One of the most shocking and dangerous omissions in the traditional mathematical framework is that it acts as if income taxes and investment fees simply do not exist in the real world. When you attempt to withdraw forty thousand dollars from a standard pre-tax traditional retirement account, you do not actually get to spend forty thousand dollars at the local grocery store. The federal government and your state government are going to take their mandatory share in the form of ordinary income tax right off the top.

Furthermore, if you are paying a human financial advisor one percent of your total portfolio value each year, or if your chosen mutual funds carry high internal expense ratios, that money quietly drains from your account continuously behind the scenes. If you actually need a full forty thousand dollars in pure cash to cover your basic living expenses, you might honestly need to withdraw forty-eight thousand dollars from the account to cover all the associated taxes and hidden fees. That reality pushes your actual portfolio withdrawal rate far beyond the safe theoretical threshold, secretly putting your entire financial future in extreme jeopardy.

It Assumes a Rigid, Unchanging Spending Plan

Human beings absolutely do not spend money in a perfectly flat, inflation-adjusted straight line from the day they retire until the day they die. The traditional math foolishly assumes you will spend the exact same real dollar amount at an active age sixty-five as you will at a highly sedentary age ninety. Real-life retirement spending usually looks much more like a smiling curve when plotted on a visual graph by researchers. During your early years of freedom, often called the go-go years, you are highly likely to spend heavily on international travel, expensive hobbies, and massive home renovations.

As you eventually enter your middle retirement or slow-go years, your overall spending typically drops significantly as you prefer to stay closer to home and settle into a quiet, inexpensive routine. Finally, in your very late retirement or no-go years, spending often spikes back up rapidly and aggressively due to expensive end-of-life healthcare and assisted living facility costs. A completely flat withdrawal strategy fails completely to accommodate these totally natural and highly predictable lifestyle shifts.

It Relies on a Strict Asset Allocation

The original historical math is entirely predicated on holding a very specific, unchanging mix of roughly fifty to sixty percent large stocks and forty to fifty percent government bonds. If you deviate from this specific recipe based on your personal feelings, the underlying math breaks down entirely and leaves you highly vulnerable. If you are a highly conservative investor who stubbornly holds eighty percent of your money in cash and bonds out of sheer fear of the stock market, the baseline rule absolutely will not work for you over thirty years.

Without enough aggressive, compounding growth from equities, daily inflation will eventually eat your cash pile alive until nothing remains. Conversely, if you are a highly aggressive investor holding one hundred percent in high-growth stocks, the extreme volatility you experience during inevitable market downturns will completely blow up your safety net. You cannot safely use the basic four percent math unless you are also fully willing to adopt the exact balanced portfolio structure it was originally built upon.

Alternative Withdrawal Strategies for a Modern Retirement

Given the severe and obvious limitations of a rigid percentage formula, modern financial advisors have developed far more sophisticated strategies to help their clients generate income safely today. These modern methods prioritize extreme flexibility, psychological comfort, and heavy downside protection against severe market crashes.

They allow you to happily enjoy your wealth when economic times are incredibly good while fiercely protecting your core nest egg when the global economy inevitably crashes.

|

Strategy Name |

Exactly How It Works |

|

Dynamic Guardrails |

Automatically adjusts your income up or down based strictly on market performance |

|

Bucket Strategy |

Physically divides money into short-term cash pools and long-term growth pools |

|

Income Floor |

Uses highly guaranteed sources to cover all absolute basic survival expenses |

The Dynamic Guardrails Approach

The dynamic guardrails approach is easily arguably the absolute most popular modern alternative to traditional, rigid percentage rules used by top planners today. Instead of a fixed annual amount that ignores reality, you establish strict upper and lower percentage limits on your spending based entirely on current stock market performance. You might decide to start by withdrawing an elevated five percent of your balance to enjoy your early years. If the market performs exceptionally well and your portfolio grows substantially, your withdrawal rate naturally drops down to three percent of the new, much higher balance.

When it hits that predetermined lower guardrail, you give yourself an automatic raise and take out more money to enjoy life and travel. On the flip side, if the stock market crashes violently and your required withdrawal suddenly represents six percent of your depleted portfolio, you hit the predetermined upper guardrail. This immediately triggers a mandatory pay cut to protect your future. You tighten your belt, reduce spending on luxury vacations or eating out, and allow the portfolio time to recover safely. This dynamic system practically eliminates the mathematical risk of running out of money, though it absolutely requires you to be perfectly okay with a fluctuating monthly income.

The Time Segmentation or Bucket Strategy

The highly popular bucket strategy focuses heavily on psychological comfort just as much as it focuses on mathematical safety during bad economic times. Instead of viewing your life savings as one giant, terrifying pool of cash tied to the stock market, you purposely divide it into three distinct buckets based on exactly when you plan to spend the money. Bucket one safely holds all the money you need for the next one to three years of daily living expenses. This money is kept entirely in ultra-safe, highly liquid assets like pure cash, high-yield savings accounts, and short-term certificates of deposit that never lose value.

Bucket two holds the money you will need in years four through ten, invested cautiously in moderate-risk assets like high-quality corporate bonds. Bucket three holds the money you will absolutely not touch for a decade or more, and it is heavily invested in aggressive growth stocks. When the stock market inevitably crashes and burns, you never panic because your immediate living expenses are fully covered by the safe cash in bucket one. You simply wait for the stock market to eventually recover before refilling your cash reserves from your growth bucket.

Maximizing the Value of Guaranteed Income

The absolute best way to completely relieve the daily pressure on your volatile investment portfolio is to build up a massive base of guaranteed, lifetime income that never stops paying. Think of this brilliant strategy as building a sturdy, unbreakable financial floor under your daily life. If your basic, non-negotiable living expenses for housing and food equal four thousand dollars a month, and you receive three thousand dollars a month from Social Security and a small pension, you only need your investment portfolio to generate one thousand dollars a month to survive.

By strategically delaying your government Social Security benefits until age seventy, you can drastically increase your guaranteed monthly payout by exactly eight percent for every year you wait past your full retirement age. Some conservative retirees also choose to purchase simple fixed indexed annuities with a small portion of their savings to essentially create a personal pension plan. When your basic survival needs are completely covered by highly guaranteed sources, your portfolio withdrawal rate becomes much less critical to your survival. This gives you the ultimate psychological freedom to invest more aggressively or weather terrible market storms without ever losing sleep.

How to Calculate Your Personal Safe Withdrawal Rate?

The biggest and most important takeaway for anyone looking deeply at the 4 percent rule retirement 2026 data is that there is absolutely no single universal number that applies to every human being. You have to sit down with a calculator and figure out a highly personalized rate based on your totally unique life circumstances, health history, and financial goals.

|

Planning Step |

Specific Action Required |

|

Determine Horizon |

Honestly estimate total years in retirement based on family health and age |

|

Subtract Income |

Carefully deduct Social Security and expected pensions from your needed total |

|

Assess Risk |

Purposely lower your withdrawal rate if market drops cause severe panic |

Assess Your True Time Horizon

You absolutely must take a brutally realistic and honest look at your current physical health, your family history of overall longevity, and the exact age at which you plan to stop working forever. If you are proudly joining the financial independence movement and walking away from your highly paid corporate job at age forty, a four percent rate is incredibly dangerous because your money has to survive fifty or maybe even sixty full years.

You absolutely might need to aim for a much more highly conservative starting rate closer to three or three point two five percent to ensure total safety. Conversely, if you absolutely love your daily job and decide to work happily until you are seventy-two, you can easily afford to withdraw five percent or much more because your expected time horizon is dramatically shorter.

Factor in Social Security and Pensions

You should honestly never try to calculate your required portfolio withdrawal rate until you have fully mapped out all your other potential sources of incoming cash. Government Social Security benefits, military or corporate pensions, rental property income, and part-time consulting work all massively reduce the daily burden placed on your investment accounts.

Sit down at the kitchen table and outline exactly how much absolute money you need to live a comfortable, happy life every year. Subtract all your highly guaranteed income streams from that total number to find the gap. Whatever specific dollar amount remains in that gap is what your portfolio actually needs to generate on a yearly basis to keep you afloat.

Adjust for Your Personal Risk Tolerance

Ultimately, smart and highly effective financial planning is mostly about sleeping incredibly well at night without stressing over the daily stock market ticker on television. If the terrifying thought of losing twenty percent of your total portfolio value in a single terrible year makes you physically ill, you are naturally going to invest very conservatively in mostly bonds.

Because highly conservative bond-heavy portfolios simply do not grow nearly as fast as aggressive stock portfolios, you absolutely have to accept a much lower withdrawal rate to survive the long term. If you are highly disciplined, totally emotionally detached from wild market swings, and totally willing to aggressively cut your daily spending during severe recessions, you can easily afford to start your retirement with a much higher initial withdrawal rate.

Final Thoughts

Retirement planning today absolutely requires serious nuance, extreme mental flexibility, and a deep, honest understanding of your own personal lifestyle goals. The complete 4 percent rule retirement 2026 guidelines absolutely prove that while the old math remains a fantastic back-of-the-napkin trick to see if you are generally on track, it should never serve as the final permanent blueprint for your daily life.

Take the required time to build a highly dynamic spending plan, purposely use the bucket strategy to fiercely protect your short-term cash, and prepare yourself mentally to adapt as the global markets naturally fluctuate. Stay highly flexible with your discretionary spending during bad economic years, and your ultimate financial freedom will be just as secure as you always hoped it would be.

Frequently Asked Questions (FAQs) About 4 Percent Rule Retirement

People constantly search online for clear answers regarding how to safely pull money from their investment accounts without making a massive mistake. We gathered the absolute most common and completely uncommon questions from recent global search trends to give you highly clear, factual answers based heavily on current economic data regarding the 4 percent rule retirement 2026 discussions.

Is 4 percent still a safe withdrawal rate in 2026?

Yes, for many totally average people it is still a very reasonable and historically safe starting point, provided you hold a properly balanced portfolio and plan for a standard thirty-year timeline. However, current deep research from top global institutions like Morningstar strongly suggests leaning slightly more conservative to protect against inflation. They highly recommend starting around 3.9 percent if you absolutely demand a rigid, unchanging income stream that adjusts only upward for inflation without ever requiring you to cut back your lifestyle.

How much money do I need to retire using the 4 percent rule?

You can easily figure this precise number out by using the classic and highly popular rule of twenty-five on a standard calculator. Simply determine your total annual expected living expenses, subtract any completely guaranteed income like Social Security, and multiply the remaining required number by exactly twenty-five. For a simple example, if you need exactly forty thousand dollars a year exclusively from your investments to survive, you multiply forty thousand by twenty-five. This math means you absolutely need a total portfolio of one million dollars to retire safely under this specific framework.

Does the 4 percent rule include inflation?

Yes, strict annual inflation adjustment is the absolute core mathematical component of the original historical concept designed in the nineties. The rule dictates heavily that you withdraw exactly four percent of the total portfolio value only in the very first year you stop working. In all subsequent years of your life, you completely ignore the current market value of your portfolio entirely. You simply take your previous year’s actual cash dollar amount and increase it by the official government rate of inflation to maintain your exact purchasing power at the grocery store.

What is the new 4 percent rule?

There is absolutely no single new mathematical rule replacing the old one, but rather a massive advisory industry shift toward highly flexible withdrawal strategies based on current market conditions. Instead of locking into a rigid permanent percentage, modern financial advisors use highly dynamic guardrails to protect their clients. This essentially means your initial withdrawal rate might actually start higher around five percent, but you formally agree to reduce your monthly discretionary spending slightly during bad economic bear markets. You then happily give yourself a lifestyle raise during strong stock market bull runs, ensuring your portfolio balance never drops to zero.

How does the 4 percent rule apply to early retirement?

It generally does not apply safely or accurately to early retirement scenarios under any circumstances. Because the original historical math was built entirely on a thirty-year timeline, someone retiring at age forty desperately needs their money to last fifty years or possibly more. Most highly credentialed financial planners strongly suggest that early retirees absolutely must use a much lower starting withdrawal rate, typically landing somewhere between 3.0 and 3.25 percent. This much lower rate is mathematically required to account for the extra decades of compounding daily inflation and multiple highly guaranteed market crashes they will experience.

What happens if I want to leave an inheritance behind?

The original math was explicitly designed to exhaust the portfolio entirely by the end of year thirty, meaning leaving an inheritance was never part of the original equation. If your absolute primary goal is to leave a massive financial legacy or fully fund a trust for your children, you cannot use a four percent withdrawal rate safely. You must lower your withdrawal rate significantly, often down to two or two point five percent, to absolutely ensure the principal balance continues to grow untouched over your entire lifetime.

{kind=link}