The American approach to healthcare does not operate like a single, government-run machine that you see in many other countries. Instead, it is a massive, somewhat messy patchwork of private insurance companies, employer-sponsored benefits, and government safety nets.

When you buy a policy, you aren’t just getting a service; you are essentially joining a massive financial pool where everyone chips in to cover the extreme costs of those who get sick. In 2026, this system is leaning much more heavily on the private markets because temporary federal boosts have finally dried up. This massive shift makes understanding your specific policy more important than it has been in a decade. If you do not know the rules of the game, you will inevitably end up paying more out of your own pocket.

|

Key Aspect |

Description |

Real-World Impact |

|

System Type |

Mixed (Private and Public) |

You have to shop around; coverage isn’t automatic. |

|

Primary Goal |

Risk mitigation and cost sharing |

Protects you from bankruptcy after a major accident. |

|

Main Players |

Private insurers, Employers, Gov |

Your options depend heavily on your job and age. |

|

2026 Status |

Increased premiums across the board |

You must budget more for your monthly healthcare costs. |

At its very core, the entire concept of insurance is basically a financial bet against bad luck. You agree to pay a set monthly fee, and the insurance company gambles that you will not need an expensive surgery anytime soon. If you do end up getting sick, they use the pool of money collected from thousands of perfectly healthy people to pay your massive hospital bills.

This collective pool of money is exactly what keeps a standard $100,000 emergency room visit from becoming a life-ending debt for an average working family. Without this shared risk model, only the extremely wealthy could ever afford modern medical care in the States. Everyone pays a little bit every month so that nobody has to pay an impossible amount all at once. It is a system built entirely on the mathematical law of large numbers.

Why 2026 is a Turning Point for US Healthcare?

This current year serves as a harsh reality check for the millions of people who buy plans on the individual marketplace. The generous “enhanced subsidies” that made marketplace plans incredibly cheap for the last few years have officially expired in 2026. Because the federal government stopped footing that extra bill, many average families are now seeing their monthly premium bills jump by hundreds of dollars.

If you haven’t taken the time to check your plan’s renewed price lately, you might be in for a massive financial shock during this year’s enrollment period. People who used to pay almost nothing for a decent Silver plan are now being forced to completely re-evaluate their household budgets. This turning point means you have to be much more strategic about exactly which plan you choose to carry for the next twelve months.

Key Health Insurance Terminology You Must Know

Before you sign any papers or commit to a monthly payment, you absolutely have to speak the language of the health insurance industry. Insurance companies love using words that sound very similar but mean incredibly different things for your wallet. To truly understand how health insurance works in the US, you have to look right past the monthly sticker price and find the hidden costs.

A policy that looks incredibly cheap on paper might actually cost you thousands of extra dollars if you end up in the emergency room. Let’s break down the most critical terms that will ultimately determine what you actually pay at the doctor’s office.

|

Term |

What It Actually Means for Your Wallet |

2026 Strategy |

|

Premium |

Your “subscription fee” paid every month. |

Shop around; these jumped up this year. |

|

Deductible |

The amount you pay before insurance helps. |

Pick a high one only if you rarely see a doctor. |

|

Copay |

A flat fee for a specific service (like $30). |

Look for plans with $0 copays for basic checkups. |

|

Coinsurance |

Your percentage of the bill (like 20%). |

Avoid high coinsurance if you expect major surgery. |

Premiums, Deductibles, and Out-of-Pocket Maximums

Your monthly premium is simply what you pay just to keep the lights on—it does not actually count toward paying for your medical care. The deductible is where your real healthcare spending starts; it is the steep “entry fee” you must pay out of your own pocket each year before the insurance company steps in to help. The absolute most important number to watch, however, is your out-of-pocket maximum limit.

This number serves as your ultimate financial safety net for the entire calendar year. Once you hit this specific limit through a combination of deductibles and copays, the insurance company has to pay 100 percent of your covered medical expenses. Knowing your out-of-pocket maximum is the only way to accurately calculate your true financial risk.

Copays vs. Coinsurance

These two financial terms are very often confused by consumers, but the actual difference is huge when the medical bills arrive. A copay is a highly predictable, flat fee—you know exactly what it costs to see your doctor or pick up a generic prescription. Coinsurance, on the other hand, is a flat percentage, which means your final bill depends entirely on the total cost of the hospital procedure.

For instance, if you have a 20 percent coinsurance rate on a $50,000 emergency surgery, you are personally on the hook for $10,000 of that bill. You must always check if your specific plan relies more heavily on predictable flat fees or risky percentages before you finalize your decision.

The Network: In-Network vs. Out-of-Network Providers

Insurance companies function basically like giant negotiation firms when dealing with the healthcare system. They strike exclusive, discounted financial deals with specific doctors, local clinics, and major hospitals to provide your care at a cheaper rate. These approved doctors make up your plan’s “In-Network” list.

If you decide to wander “Out-of-Network” because you like a different doctor, you are essentially paying the full luxury “sticker price” for your healthcare. In many modern 2026 plans, the insurance company simply will not pay a single cent if you see an unapproved, out-of-network doctor. You must always verify that your absolute favorite doctor is still in the network every single year, as these lists change without warning.

Types of Health Insurance Plans in 2026

Not all insurance policies behave the exact same way when you actually need to go see a medical professional. Some plans act like very strict gatekeepers, while others give you total freedom if you are willing to pay a premium price for it. In 2026, the market is seeing a massive rise in “Exclusive” plan types that limit your doctor choices but help keep your monthly premiums slightly lower.

Choosing between the different letter combinations is basically a balancing act between how much you value your personal freedom and how much you value your bank account savings. Here is exactly how the most common plan structures stack up against each other this year.

|

Plan Type |

Do You Need Specialist Referrals? |

Out-of-Network Coverage? |

Overall Price Point |

|

HMO |

Yes (Strictly Required) |

No (Only in true emergencies) |

Lowest Premium |

|

PPO |

No (Total Freedom) |

Yes (But it costs more) |

Highest Premium |

|

EPO |

No (You book directly) |

No (Strictly forbidden) |

Moderate Premium |

|

POS |

Yes (Required by PCP) |

Yes (But highly expensive) |

Moderate Premium |

Health Maintenance Organization (HMO)

An HMO is arguably the most structured and restrictive type of insurance plan you can possibly buy today. You are strictly required to pick a Primary Care Physician who acts like a dedicated traffic cop for all of your healthcare needs. If you wake up and want to see a skin doctor or a heart specialist, you have to get an official “referral” from your primary doctor first.

If you try to bypass this rule or see someone completely outside the approved network, the HMO simply will not pay the medical bill. While it is the most restrictive option by far, it is also usually the absolute cheapest way to get comprehensive coverage for your family.

Preferred Provider Organization (PPO)

PPO plans are widely considered the absolute “gold standard” for patient flexibility and freedom. You absolutely do not need to pick a primary doctor, and you do not need to wait around for a referral just to see a specialist. If you want to travel to a famous doctor across the state who isn’t officially in your network, the PPO will still help pay a portion of that expensive bill.

Most people vastly prefer PPOs because they offer the most control over who you let treat your body. However, because you get so much luxury and flexibility, you will undoubtedly pay a much higher monthly premium for that privilege.

Exclusive Provider Organization (EPO)

Think of an EPO plan as a very strict hybrid sitting right between an HMO and a PPO. Just like a flexible PPO, you do not need a referral to see a specialist, which ultimately saves you a lot of frustrating waiting room time. However, exactly like a strict HMO, there is absolutely zero financial coverage for out-of-network medical care.

If you decide to use an EPO plan, you have to be extremely careful to guarantee that every single doctor you see is on the “approved” list. It is a highly popular choice in 2026 for people who want quick specialist access without paying the incredibly high cost of a full PPO.

Point of Service (POS) Plans

POS plans are a slightly less common option that blend the defining features of both HMOs and PPOs into one confusing package. You are fully required to select a primary care physician and obtain official referrals before you can visit any specialists, which feels exactly like an HMO.

But somewhat similar to a PPO, you are technically allowed to see out-of-network providers if you really want to. The catch is that if you go out of network, you have to do all the complicated billing paperwork yourself and pay a massive share of the cost. They offer a weird middle ground that only appeals to a very specific type of healthcare consumer.

High-Deductible Health Plans (HDHP) and HSAs

An HDHP is exactly what the name suggests: you willingly agree to a very high deductible in exchange for paying a tiny monthly premium. These specific plans are almost always legally paired with a Health Savings Account (HSA) to help you manage the financial risk. An HSA is a highly specialized bank account where you deposit pre-tax money specifically to pay for your massive medical bills.

The absolute best part about an HSA is that the money stays yours forever—it does not randomly disappear at the end of the year like other accounts. For young, generally healthy people who rarely get sick, this is very often the smartest long-term financial move.

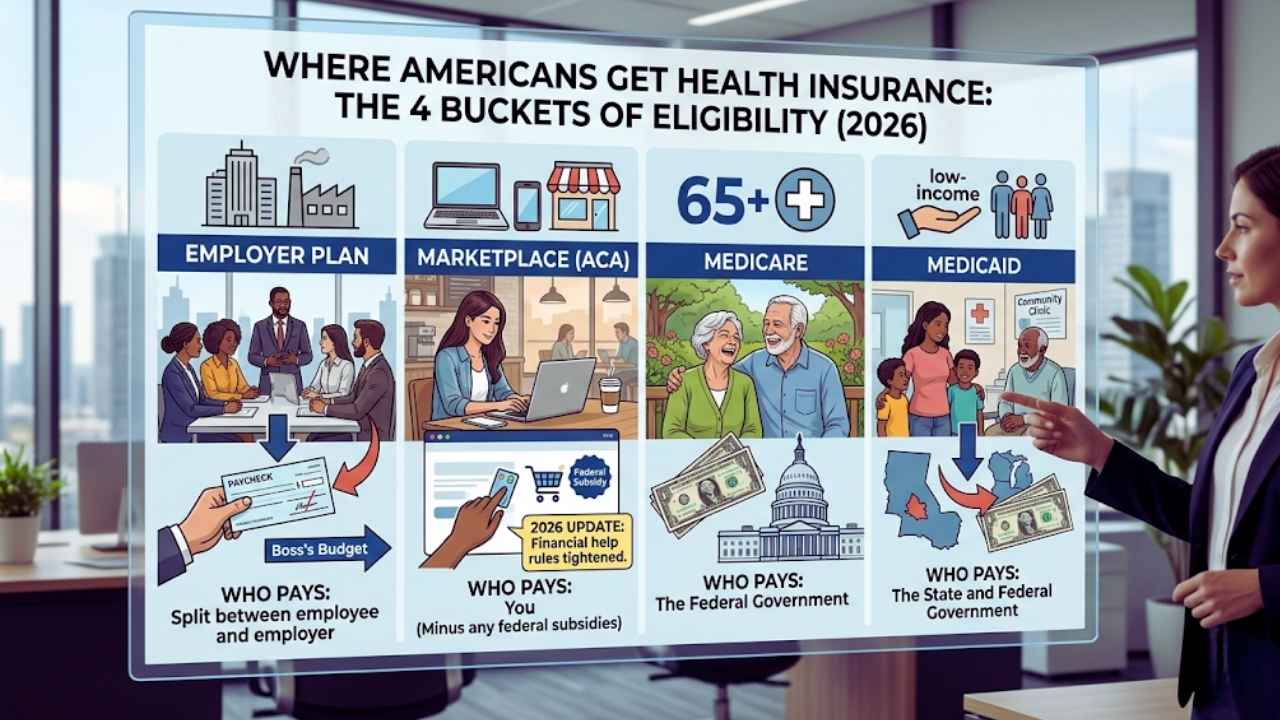

Where and How to Get Health Insurance Coverage?

Most typical Americans do not just walk into an insurance office on Main Street and buy a policy off a dusty shelf. Exactly where you get your insurance usually depends entirely on your current job, your exact age, or how much money you make. The way how health insurance works in the US is strictly divided into very clear “buckets” of legal eligibility.

If you are incredibly lucky, your boss simply pays for it out of the company budget. If not, you are heading straight to the government-run Marketplace to fend for yourself. In 2026, the strict rules for who gets financial help have tightened up significantly, so you need to know exactly which bucket you belong in.

|

Insurance Source |

Who Usually Qualifies? |

Who Actually Pays the Premium? |

|

Employer Plan |

Full-time corporate employees |

Split between you and your boss |

|

Marketplace (ACA) |

Self-employed / Gig workers |

You (minus any federal subsidies) |

|

Medicare |

People aged 65 and older |

The Federal Government |

|

Medicaid |

Very low-income individuals |

The State and Federal Government |

Employer-Sponsored Health Insurance

This is by far the most common way that working-age Americans manage to get covered without going broke. Your employer actively negotiates a massive group rate with a major insurance company and usually pays about 70 to 80 percent of the premium for you. The small portion of money you actually pay comes directly out of your paycheck before your taxes are even calculated.

Because the company is buying coverage in bulk for hundreds or thousands of people, these plans are usually vastly superior. They are almost always significantly cheaper and cover much more than anything you could possibly buy on your own in the private market.

The ACA Health Insurance Marketplace

If you are a freelance worker, a small business owner, or your specific job simply does not offer health benefits, you go straight to the Marketplace. This massive website is where you can openly compare private plans side-by-side to see who offers the best deal. For 2026, the “Enhanced Subsidies” that made things so cheap over the last few years are completely gone.

This terrible news means that if you make a decent middle-class living, your chosen plan is going to be significantly more expensive than it was last year. You can still apply to get financial help, but the government’s income limits are much stricter now.

Government Programs: Medicare and Medicaid

Medicare is the massive federal safety net system designed specifically for older senior citizens. Once you officially hit 65 years old, the federal government basically takes over as your primary insurance provider. It is entirely funded through the heavy taxes you paid during your working years.

Medicaid, on the completely other hand, is a dedicated safety net for people who have very low household incomes. It is run by individual states, so the exact rules for who qualifies can be wildly different depending on where you live. In many generous states, Medicaid is completely free or costs only a few tiny dollars a month.

Private Health Insurance Options

Sometimes, desperate people try to buy insurance outside of the government marketplace directly from an independent insurance broker. These are very often labeled as “short-term” or “catastrophic” emergency plans to attract buyers. You must be very careful here—many of these sketchy plans do not follow the standard ACA rules.

They can legally refuse to cover you if you have a pre-existing condition like asthma or diabetes. They also might not cover basic essential things like expensive prescriptions or routine maternity care. They are incredibly cheap for a very specific reason, and that reason is usually that they simply do not cover very much.

Understanding ACA Metal Tiers and 2026 Costs

When you are finally shopping on the official ACA Marketplace, you will see all the available plans labeled as Bronze, Silver, Gold, or Platinum. These shiny metal names are absolutely not ratings of how “good” the actual doctors or hospitals are. Instead, they simply tell you the basic math of how the cost-sharing is split between you and the company.

A Gold plan does not give you “better” or faster medicine than a Bronze plan; it just means the insurance company pays a lot more of the bill. In 2026, the premium price gap between these metal tiers has widened dramatically, making the choice much more stressful for average families.

|

Metal Tier Name |

Monthly Premium Cost |

Your Out-of-Pocket Cost |

Who Should Buy This Plan? |

|

Bronze |

Lowest Premium |

Highest Deductibles |

Very healthy people / emergency only |

|

Silver |

Moderate Premium |

Moderate Deductibles |

Most average families (best subsidies) |

|

Gold |

High Premium |

Low Deductibles |

People with known chronic illnesses |

|

Platinum |

Highest Premium |

Lowest Deductibles |

Frequent hospital users / pregnant women |

Bronze, Silver, Gold, and Platinum Plans

Bronze plans are specifically designed for the absolute “just in case” emergency scenario. They have the lowest monthly cost, but if you actually get sick, you will have to pay a massive deductible before the insurance helps at all. Silver plans are the standard “middle of the road” option and are uniquely the only plans where you can get special “Cost-Sharing Reductions” if your income is low.

Gold and Platinum plans are specifically built for people who know for a fact they will be at the doctor very frequently. You pay a lot of money every single month, but your routine office visits and daily prescriptions will cost almost nothing when you get there.

Average Health Insurance Costs in 2026

Let’s stop beating around the bush and talk about the real financial numbers. For the year 2026, the absolute average cost for a 40-year-old on a standard Silver plan is hovering aggressively around $550 to $650 per month before any help. If you are older and in your 60s, that painful number can easily double without warning.

Because the dreaded 2026 “Subsidy Cliff” has officially returned, families earning more than 400 percent of the federal poverty level get zero help. They are now paying the full, painful “sticker price” for their monthly insurance. This brutal reality has made health insurance one of the largest and most stressful monthly expenses for middle-class American families this year.

You absolutely cannot just buy health insurance whenever you happen to feel like it. If you wake up with a terrible toothache or a suddenly broken leg in the middle of July, you cannot just log online and sign up for a plan that day. You are strictly forced to wait for the official Open Enrollment Period to come around.

This is a very specific, government-mandated window of time once a year when absolutely anyone can change their plan. Outside of this tight window, the door is completely locked unless you experience a major, life-altering change.

|

Enrollment Type Window |

Exactly When Does It Happen? |

Specific Legal Requirements |

|

Open Enrollment |

November 1 – January 15 |

None (It is completely open to everyone) |

|

Special Enrollment |

Any time of the year |

You must have a verified “Qualifying Life Event” |

|

Medicare Open |

October 15 – December 7 |

You must be 65+ or otherwise fully eligible |

|

Medicaid Access |

Any time of the year |

You must strictly meet state income limits |

The End of Year-Round Enrollment for Low-Income Earners

During the confusing last few years of the pandemic, the government graciously allowed people with very low incomes to sign up for insurance at literally any time of the year. Sadly, for 2026, that highly helpful rule has been completely scrapped by the administration.

Now, absolutely everyone—regardless of exactly how little money you make—must sign up during the standard winter window. This window typically runs strictly from November 1st to January 15th in almost every state. If you accidentally miss this brief window, you could easily be stuck without any insurance for an entire calendar year, which is a massive financial risk.

Special Enrollment Periods and Qualifying Life Events

Life happens very fast, and sometimes you completely lose your good insurance in the middle of the calendar year. If you get officially married, have a brand-new baby, move to a completely new state, or lose your job-based coverage, you trigger a “Special Enrollment Period.”

You usually have exactly 60 days from the precise day of the event to log online and pick a new plan. You have to provide strict legal proof—like a signed marriage license or an official birth certificate—to show the insurance company you aren’t lying. This proves that you actually qualify for this rare mid-year signup exception.

Step-by-Step Guide to Choosing the Right Health Insurance Plan

Picking a medical plan absolutely should not be a blind guessing game or a rushed decision. To truly master how health insurance works in the US, you need to treat the entire process exactly like a complicated math problem. Most average people make the terrible mistake of only looking at the monthly premium and ignoring the rest.

However, the “cheapest” plan on paper can rapidly become the most expensive disaster if you have to see a doctor more than twice a year. Follow these critical steps to guarantee you aren’t severely overpaying for coverage you do not actually need.

|

Step Number |

Critical Action Item |

Why It Ultimately Matters |

|

Step 1 |

Estimate your total annual doctor visits |

It determines if you truly need a low deductible. |

|

Step 2 |

List your current daily medications |

It checks if the new plan will actually pay for your drugs. |

|

Step 3 |

Search the directory for your doctors |

It totally prevents “Out-of-Network” surprise hospital bills. |

|

Step 4 |

Calculate your Maximum Total Cost |

It accurately adds Premiums plus Expected Out-of-Pocket costs. |

Assessing Your Medical Needs and Budget

Start the confusing process by looking directly backward at your medical calendar from the last entire year. If you are generally healthy and only go to the doctor for a quick yearly checkup, a cheap Bronze plan is probably your best financial bet.

But if you have a known chronic condition like bad diabetes that requires regular visits, you really should look at expensive Gold plans. Even though the monthly bill is much higher, you will save thousands of dollars on the back end. This happens because the insurance company covers a much bigger share of your very frequent, highly expensive regular medical costs.

Comparing Plan Networks and Prescription Formularies

Every single insurance plan has a complex “Formulary,” which is basically just a fancy legal word for a list of drugs they agree to pay for. Before you blindly sign up, search that exact list for any pills you take on a daily basis. Some tricky plans might list your drug as “Tier 1” (very cheap), while others might push it to “Tier 4” (incredibly expensive). Similarly, you must use the plan’s online search tool to find your specific hometown doctor. If your doctor isn’t in that specific network, you’ll either have to find a complete stranger for a doctor or pay the entire massive bill yourself.

Final Thoughts

Navigating the US healthcare system isn’t about finding a “perfect” plan; it’s about finding the one that sucks the least for your specific situation. As we move through 2026, the era of ultra-cheap, subsidized plans is fading, and consumers have to be much more strategic. Whether you’re choosing an employer plan or browsing the marketplace, always look at the out-of-pocket maximum first. That’s the only number that truly protects you from bankruptcy.

Understanding how health insurance works in the US takes a bit of effort, but it pays off when you avoid a $5,000 surprise bill. Stay in your network, keep an eye on your deductible, and don’t miss the Open Enrollment window. If you do those three things, you’re already ahead of 90% of the population.

Frequently Asked Questions (FAQs) How Health Insurance Works Us

Can I get health insurance if I’m not a US citizen?

Yes, but it heavily depends on your exact legal immigration status. Lawfully present immigrants can easily buy insurance through the Marketplace and are fully eligible for federal subsidies. Undocumented immigrants generally cannot legally buy through the Marketplace but can often purchase expensive private plans directly. They can also usually access vital emergency care through Medicaid in certain generous states.

What is a “Summary of Benefits and Coverage” (SBC)?

An SBC is a highly standardized document that every single insurance company is legally required to give you before you buy. It functions exactly like a clear “Nutrition Facts” label for your confusing health plan. It shows you exactly what you’ll pay for common medical scenarios, like having a baby or managing Type 2 diabetes. Always demand to see this before you hand over any money.

What happens if I just don’t buy health insurance in 2026?

There is officially no longer a federal tax penalty for simply being uninsured at the end of the year. However, a few specific states still have their own state-level financial penalties that will hit you at tax time. More importantly, you are 100 percent responsible for your own medical bills if you get hurt. A single bad night in the emergency room can easily cost $10,000 or more, which is why going without coverage is insanely dangerous.

Can my insurance company cancel my plan if I get really sick?

No, they absolutely cannot do that anymore. Thanks to the strict rules of the ACA, insurance companies cannot suddenly cancel your coverage just because you are using it “too much.” They also cannot drop you because you developed a very serious, expensive illness like cancer. As long as you keep paying your monthly premiums on time, they are legally forced to keep your coverage active.

What is a “Balance Bill” and is it actually legal?

A nasty balance bill happens when a doctor charges more than your insurance company’s “allowed amount” and rudely bills you for the remaining difference. Thankfully, under the new No Surprises Act, it is now highly illegal for providers to send you surprise balance bills for emergency services. They also cannot do it for unexpected out-of-network care provided at an otherwise in-network facility.

{kind=link}