Choosing between the standard vs itemized deduction is usually the first big hurdle you hit when filing your taxes. It feels like a high-stakes game of “pick a path,” where one choice leads to a smaller tax bill and the other might leave your money on the table.

Most people want the biggest discount possible on their taxable income, but the “right” choice isn’t the same for everyone. Whether you are a homeowner with a massive mortgage or a renter with zero debt, understanding how these two options work is the best way to keep more of your paycheck.

What Is the Standard Deduction?

The standard deduction is essentially a flat-rate discount that the IRS gives you automatically. You don’t have to prove anything, keep any receipts, or list out your expenses to get it. It is a set dollar amount that reduces your taxable income based on your filing status. For the vast majority of Americans, this is the most beneficial path because it is simple and usually higher than what they could scrape together by listing individual expenses.

|

Filing Status |

2026 Projected Amount |

Ideal Candidate Profile |

Key Benefit |

|

Single |

$15,350 |

Renters, young professionals |

No paperwork or receipts required |

|

Married Filing Jointly |

$30,700 |

Two-income households |

Large “automatic” tax break |

|

Head of Household |

$23,000 |

Single parents with dependents |

Extra financial buffer for care providers |

|

Married Filing Separately |

$15,350 |

Spouses keeping finances split |

Matches the single filer baseline |

The 2026 Thresholds and Inflation

Every year, the IRS adjusts the standard deduction amounts to keep up with the rising cost of living and inflation. In 2026, we are seeing some of the highest standard deduction amounts in history due to recent economic adjustments. This means the “bar” you have to clear to make itemizing worth your time is higher than it has ever been. The IRS uses a specific metric called the Chained Consumer Price Index to calculate these precise bumps.

If you are a single filer, you need more than $15,350 in highly specific, IRS-approved expenses before you even think about itemizing. For married couples, that hurdle sits at a massive $30,700. Because inflation pushes these numbers up annually, fewer taxpayers find themselves needing to itemize year over year. Ultimately, this built-in inflation adjustment protects your purchasing power and keeps your baseline tax liability manageable without extra effort.

Why Simplicity Usually Wins?

The standard deduction is the ultimate “set it and forget it” tax strategy for the modern taxpayer. You do not need a shoebox full of paper records, and you never have to panic about finding a faded pharmacy receipt from nine months ago. You just check a simple box on your tax software, and the system automatically drops your taxable income.

Since the Tax Cuts and Jobs Act passed several years ago, the standard deduction nearly doubled overnight, pushing roughly 90% of taxpayers into this straightforward category. It is highly efficient, entirely safe from documentation audits, and requires absolutely zero math on your part. For people with busy lives, the value of saving hours of tax preparation time often outweighs the handful of extra dollars they might squeeze out of itemizing.

Additional Deductions for Seniors and the Blind

If you are age 65 or older, or if you are legally blind, the federal government gives you a valuable extra discount on your taxes. You get an additional standard deduction amount seamlessly added to your base number. This is a common area where older adults miss out on extra savings because they do not realize they qualify automatically.

You do not have to itemize or provide extensive medical records to get this “bonus” amount; it just stacks right on top of your standard deduction. If you and your spouse are both over 65, you both get the extra amount added to your joint return. It acts as a safety net to recognize the higher living and healthcare costs that often accompany aging. Checking the right boxes for your age and vision status can literally shave thousands off your final tax bill.

Understanding Itemized Deductions

Itemizing is the process of building your own tax break entirely from scratch using your actual financial records. Instead of taking the flat-rate automatic amount, you list out every single eligible expense you had during the year on a form called Schedule A. This is only worth the effort if the total of these items is legitimately larger than the standard deduction for your filing status.

|

Expense Category |

Potential Tax Impact |

Required IRS Documentation |

Common Limitations |

|

Mortgage Interest |

Very High for new homeowners |

Form 1098 from your lender |

Capped at $750k in total loan principal |

|

State/Local Taxes |

High in expensive states |

W-2s, property tax invoices |

Hard cap of $10,000 annually |

|

Charitable Gifts |

High for consistent donors |

Bank records, official charity letters |

Limits based on a percentage of AGI |

|

Medical Bills |

Moderate to High |

Itemized hospital/pharmacy invoices |

Must exceed 7.5% of your AGI first |

When Should You Consider Itemizing?

You should seriously look into itemizing if you had a year filled with “big ticket” deductible financial events. Maybe you just bought your first home and paid a massive amount of upfront mortgage interest, or perhaps you had a major surgery that your insurance flat-out refused to cover. You might also consider it if you live in a state with punishingly high property and income taxes.

If you look at your rough financial footprint and suspect your total expenses will easily beat the $15,350 or $30,700 marks, it is time to start gathering your paperwork. Major life changes, like inheriting money and making huge charitable gifts, also trigger the need to evaluate this method. The standard vs itemized deduction debate really heats up when your real-world spending starts outpacing the government’s generic estimates.

The Paperwork Requirement

Unlike the standard deduction, the IRS demands strict, written proof for absolutely everything you claim when you itemize. This means you need to be incredibly organized throughout the entire calendar year. If you claim $5,000 in charitable donations, you must have the official acknowledgment letters from those specific charities tucked away in your files.

Digital copies, bank statements, and scanned receipts are perfectly acceptable, but you must have them ready. If you are audited and cannot produce the proper paperwork, the IRS will completely disallow the deduction. They will then send you a revised tax bill for the difference, plus hefty penalties and interest. Keeping a dedicated tax folder on your computer or a physical envelope on your desk is the smartest way to survive this requirement.

The Impact of the $10,000 SALT Cap

One of the biggest, most frustrating hurdles for itemizers is the State and Local Tax (SALT) deduction limit. Currently, federal law dictates that you can only deduct up to $10,000 total for state income tax and local property taxes combined. For people living in high-tax states like California, New Jersey, or New York, this cap acts as a massive roadblock.

Before this cap existed, high earners in these states could easily itemize based almost entirely on their state tax burden. Now, you hit that $10,000 ceiling remarkably fast, often just from the property taxes on a modest home alone. This specific cap makes it exceptionally hard for the standard vs itemized deduction comparison to favor itemizing unless you have huge medical or mortgage expenses to bridge the gap.

Comparing the Two: A Side-by-Side Look

When you finally sit down to do your taxes, you are essentially running a race between two distinct numbers. On one side, you have the guaranteed standard deduction, and on the other, you have your “real world” itemized expenses. Whichever number is higher is the one you legally want to use on your return.

|

Feature Comparison |

Standard Deduction Path |

Itemized Deduction Path |

|

Taxpayer Effort Level |

Minimal (Just check a box) |

High (Requires intense organization) |

|

Records & Receipt Rules |

None required by the IRS |

Keep receipts for at least 3 to 7 years |

|

Financial Predictability |

Extremely High and stable |

Low (Fluctuates based on annual spending) |

|

Overall Audit Risk |

Very Low |

Moderate (Higher scrutiny on large claims) |

Deciding Based on Homeownership

Homeownership is far and away the number one reason ordinary people switch from the standard path to itemizing. The interest you pay on your mortgage loan is heavily front-loaded in the early years and is often the largest single deduction available to a taxpayer. If you just bought a home with a $500,000 mortgage at a 6% interest rate, you are paying roughly $30,000 in pure interest during that very first year.

That number alone instantly makes itemizing the clear winner for a single filer, and it puts married couples right on the borderline. However, as you pay down your loan over ten or twenty years, the interest drops, and the standard deduction often becomes the better deal again. You have to re-evaluate this amortization math every single year.

The Role of Charitable Giving

If you are someone who routinely gives a significant portion of your income to a church, a local food bank, or a registered non-profit, itemizing becomes a much more attractive financial prospect. Under the standard deduction, you generally do not get any extra tax credit for those generous donations. By taking the time to itemize, every single dollar you give potentially lowers your final tax bill.

This is provided you have already cleared the baseline standard deduction threshold with other heavy expenses like state taxes or mortgage interest. You can even deduct non-cash donations, like dropping off bags of old clothes at Goodwill or donating a used vehicle, provided you get a receipt detailing the fair market value.

Evaluating Your Tax Bracket

While the gross deduction amount stays exactly the same on paper, the actual cash value of that deduction changes wildly based on your income level. The United States uses a progressive tax system, meaning your top dollars are taxed at a higher marginal rate. If you are sitting in a hefty 32% tax bracket, a $10,000 itemized deduction literally saves you $3,200 in cold, hard cash.

If you are sitting in the lower 12% bracket, that exact same $10,000 deduction only saves you $1,200. This stark math is exactly why high-income earners are often much more aggressive and meticulous about finding legal ways to itemize their returns. The higher your income climbs, the more valuable every single deductible expense becomes.

Deep Dive: The Major Itemized Expenses Explained

To really master the standard vs itemized deduction choice, you have to know exactly what actually counts as a write-off. You cannot just casually deduct your daily car payment, your utility bills, or your weekly groceries. The IRS has incredibly strict, nuanced rules about what qualifies under the law.

|

Itemized Category |

The Vital “Fine Print” |

Why It Matters for Your Strategy |

|

SALT (Taxes) |

Hard $10,000 maximum limit per return |

Serves as the base, but rarely enough alone |

|

Mortgage Interest |

Limit applies to debt up to $750k |

The primary engine driving most itemized returns |

|

Medical Expenses |

Must beat the 7.5% of AGI floor |

Extremely hard to utilize without major health events |

|

Charitable Gifts |

Subject to AGI percentage caps |

Offers the most flexibility for strategic “bunching” |

The Nuances of Mortgage Interest

You can legally deduct the interest paid on up to $750,000 of mortgage debt, provided the loan was used to buy, build, or substantially improve your primary or secondary home. If you have a massive million-dollar mortgage, you can strictly only deduct the interest generated on the first $750,000 of that balance.

Additionally, the rules regarding Home Equity Lines of Credit (HELOCs) have tightened significantly in recent years. If you took out a home equity loan to go on a lavish vacation, buy a sports car, or pay off credit card debt, that interest is completely non-deductible. The borrowed money must be pumped directly back into the physical house itself to qualify for the write-off.

Most healthy people never get to deduct their medical bills because of a punishing rule known as the AGI “floor.” You can only deduct the specific portion of your medical costs that exceeds 7.5% of your adjusted gross income. If you earn $100,000 a year, the first $7,500 of your medical bills are essentially “lost” from a tax savings perspective.

Only if you spend $12,000 on major surgeries, expensive prescriptions, or long-term care would you get to add the remaining $4,500 to your itemized list. You can include things like mileage driven to the hospital, out-of-pocket insurance premiums, and necessary home modifications like wheelchair ramps. However, cosmetic surgeries and general wellness expenses like gym memberships absolutely never count.

State and Local Taxes (SALT)

This massive category includes your state income tax (or your state sales tax, but never both) and your local property taxes. In years past, there was absolutely no limit on this category, making it a goldmine for coastal residents. Now, constrained by the $10,000 cap, it merely serves as a foundational “base” for modern itemizers.

If you pay $12,000 in local property taxes and $6,000 in state income tax, you lose $8,000 of potential deductions because you max out at $10k. Some states allow you to deduct the value-based portion of your vehicle registration fees here as well. Choosing between deducting state income tax versus state sales tax is highly beneficial if you live in a state like Texas, Florida, or Nevada that lacks a state income tax entirely.

Strategy: The Bunching Technique

If you find that your annual financial expenses are consistently landing just a few hundred dollars below the standard deduction amount, you are trapped in a frustrating tax limbo. You aren’t getting any extra tax benefit from your real-world spending. This is precisely where a clever, legal strategy called “bunching” comes into play.

|

Tax Year |

The Bunching Strategy Applied |

Financial Result and Outcome |

|

Year 1 (Odd Year) |

Take the Standard Deduction |

Enjoy the flat $15,350 or $30,700 base |

|

Year 2 (Even Year) |

“Bunch” expenses and Itemize |

Claim $40,000+ by doubling up payments |

|

Long-Term View |

Alternate strategies annually |

Achieve maximum total tax savings over time |

How to Bunch Charitable Gifts?

Instead of habitually giving $5,000 to your favorite charity every December, you could easily shift your strategy to give $10,000 every other January. By consciously concentrating two years’ worth of your charitable giving into a single calendar tax year, you artificially inflate your deductions. This vastly increases the chances that your total itemized deductions will finally exceed the massive standard amount.

The charity still gets the exact same amount of money from you over a 24-month period, so their operations are unaffected. However, this slight shift in timing completely changes how much money you get back from the IRS in a given year. Many wealthy taxpayers use Donor Advised Funds to accomplish this, allowing them to take the massive tax break today while slowly distributing the cash to charities later.

Timing Medical Procedures

If you know for a fact that you need an expensive dental implant or a costly, non-emergency joint surgery, carefully timing the procedure can be a brilliant tax move. If you have already managed to hit your 7.5% medical floor earlier in the year due to an unexpected illness, the window of opportunity is wide open.

Any additional medical or dental procedures you can squeeze in and pay for before December 31st will be fully, 100% deductible. If you lazily wait until January 1st to have the surgery, the IRS clock resets entirely, and you have to fight to hit that steep 7.5% floor all over again from scratch. Consolidating your family’s major medical expenses into one painful, but tax-efficient, year is a phenomenal strategy.

Prepaying Property Taxes

Depending on the specific laws in your local county, you may be legally allowed to pay your property tax bill for the following year a few days early in late December. If you haven’t yet hit your $10,000 SALT cap for the current year, paying next year’s taxes early is a fantastic way to instantly boost your itemized total. You just have to ensure the payment fully clears your bank account before the ball drops on New Year’s Eve.

However, you must tread carefully and consult a tax professional to ensure this doesn’t trigger the Alternative Minimum Tax (AMT). Furthermore, if your mortgage lender pays your taxes through an escrow account, you have to coordinate with them carefully to pull this strategy off without double-paying.

How to Choose: A Step-by-Step Guide

Making the final, confident call between the standard vs itemized deduction doesn’t have to induce a migraine. You simply need a logical, systematic way to review your household finances.

|

Step Number |

Required Action |

The Ultimate Goal |

|

Step 1 |

Gather all 1098s, W-2s, and receipts |

Discover your “real” itemized number |

|

Step 2 |

Check the exact 2026 IRS limits |

Know the strict “bar” you must legally clear |

|

Step 3 |

Run the numbers using both methods |

Visualize the actual dollar difference in taxes |

|

Step 4 |

Audit your personal time and stress |

Decide if $50 in savings is worth 5 hours of work |

Start with Your Largest Expenses

Do not immediately start sweating the small stuff or digging through your car for a $5 toll receipt. Look straight at your massive mortgage interest statements and your total state taxes paid. For the vast majority of normal people, these two massive categories make up over 80% of their potential itemized deductions.

If you add your mortgage interest and your $10,000 SALT cap together, and you are still somehow $15,000 away from beating the standard deduction, you can stop right there. You probably do not need to spend hours meticulously logging your minor out-of-pocket medical co-pays or your small clothing donations to Goodwill. The math is already telling you that the standard deduction is going to win easily.

Consider Your Filing Status

Your legally defined filing status is arguably the biggest single factor in this entire mathematical decision. If you are legally Married Filing Jointly, your target “hurdle” to beat is a whopping $30,700 for the year. That is an incredibly high financial bar to clear, requiring serious mortgage debt or massive medical tragedies.

Conversely, if you are single, your target is much lower at $15,350, making it statistically much easier for you to itemize successfully. Always make absolutely sure you are comparing your tracked expenses to the correct, updated target number for your specific household structure.

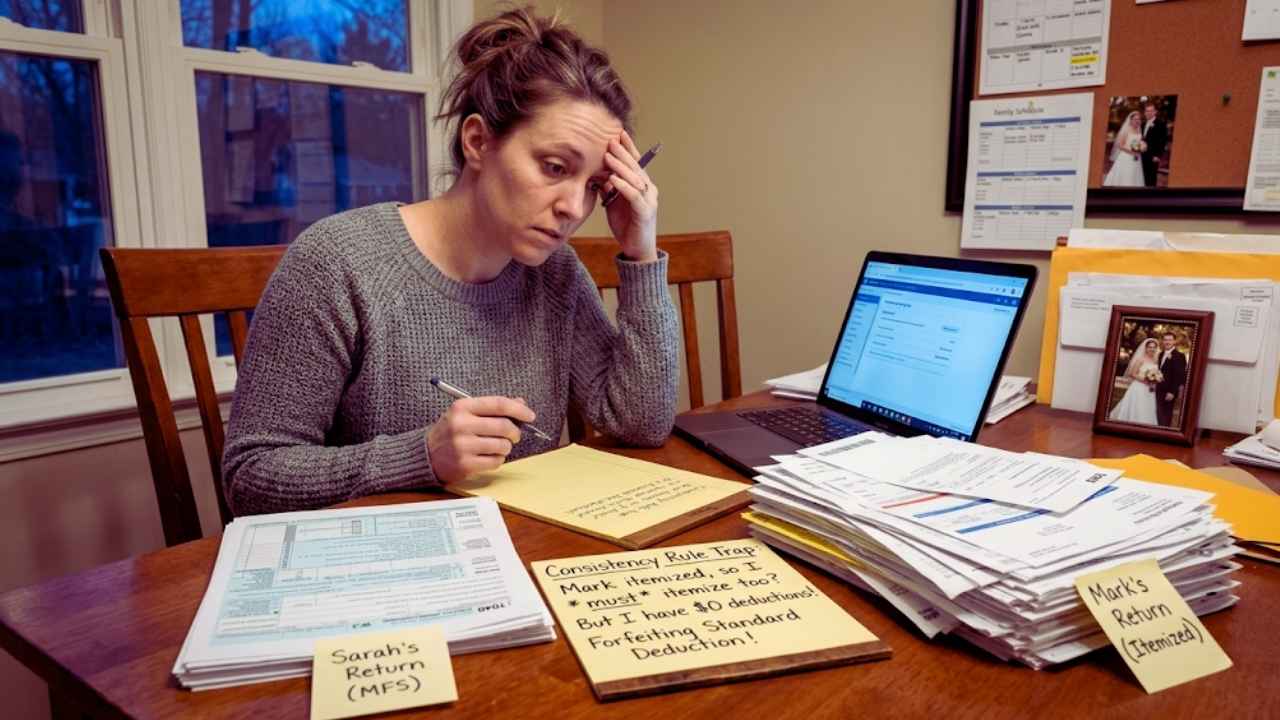

The Consistency Rule for Married Couples

Here is a very dangerous tax trap that catches thousands of people off guard every year: If you are legally married but choose to file your returns separately, you both must absolutely choose the exact same deduction method. If your spouse decides they have to itemize because they incurred huge, separate medical bills, you are legally forced to itemize on your return as well.

You have to do this even if your own personal itemized deductions total exactly zero dollars, meaning you forfeit the standard deduction entirely. This harsh consistency rule is a primary reason why the “Married Filing Separately” status is frequently the absolute worst, least beneficial way to file your taxes. Couples must communicate effectively to ensure one spouse’s choice doesn’t financially ruin the other’s return.

The Impact of Tax Law Changes

The landscape of federal taxes is entirely entirely written in pencil, never in stone. The rules and thresholds we are operating under in 2026 are largely the direct result of temporary laws passed years ago.

|

Tax Law or Provision |

Current 2026 Status |

Potential Future Outlook |

|

TCJA Standard Deduction |

Currently historically high |

Subject to drastic reduction if laws sunset |

|

The SALT Cap |

Strictly capped at $10,000 |

Heavily debated, constantly targeted by coastal states |

|

Mortgage Interest Cap |

Limited to $750,000 of debt |

Likely to remain stable to protect middle-class housing |

|

Medical Expense Floor |

Locked at 7.5% of AGI |

Generally remains consistent across administrations |

Why 2026 is a Pivotal Year?

As we push deeper into 2026, we are standing at a massive crossroads for American tax policy. Many of the generous standard deduction provisions from the 2017 Tax Cuts and Jobs Act (TCJA) were explicitly written with a built-in expiration or “sunset” date. If Congress completely fails to act or extend these provisions, the tax code could revert back to older, much more complex rules.

This would mean the standard deduction could be slashed nearly in half overnight. If that dramatic shift happens, millions of average middle-class families will suddenly find themselves desperately needing to itemize their taxes once again just to survive the tax hit. Keeping a close eye on financial news this year is critical for long-term planning.

The Role of the IRS and Inflation

The IRS mathematically uses the Chained Consumer Price Index to tweak deduction amounts upward every single year. In years plagued by stubbornly high economic inflation, the standard deduction naturally jumps up significantly to match. This mechanism is incredibly great for younger renters because they get a much larger, automatic “discount” on their taxes without doing any extra administrative work.

But for established homeowners whose primary mortgage interest payments are locked in and steadily dropping, a rapidly rising standard deduction actually makes their specific housing tax break feel less valuable. Essentially, inflation slowly erodes the relative power of your fixed itemized deductions while simultaneously boosting the baseline standard option.

Staying Prepared for Audits

Regardless of how the tax laws shift in the future, the IRS absolutely loves meticulous documentation. If the laws do abruptly change and you decide you need to itemize for the very first time in a decade, you must make sure your record-keeping skills are up to the task. You should absolutely not fear an IRS audit if you are simply telling the truth and claiming legally valid expenses.

Digital photographs and cloud-based copies of receipts are perfectly acceptable under current IRS guidelines. Therefore, you should seriously consider utilizing a simple smartphone scanning app to keep your records beautifully organized throughout the year. Taking five minutes a week to scan receipts is infinitely better than enduring a terrifying scramble in early April.

Common Myths About Deductions

There is so much incredibly bad, entirely inaccurate financial advice floating around on social media regarding taxes. Some overly enthusiastic influencers think itemizing is a “secret” wealthy loophole to get rich, while anxious folks think it is a guaranteed one-way ticket to an aggressive IRS audit.

|

Common Tax Myth |

The Actual IRS Reality |

|

“Itemizing is only for the rich.” |

It is for absolutely anyone with highly specific, qualifying costs. |

|

“I can deduct my family pet.” |

You can only deduct certified service animals strictly required for medical needs. |

|

“All charity counts for taxes.” |

You can only deduct verified gifts given directly to registered 501(c)(3) organizations. |

|

“Itemizing is too hard to do myself.” |

Modern tax software makes the math completely automatic and incredibly simple. |

You Can’t “Double Dip”

One of the most persistent, wildly common misconceptions is that you can happily take the massive standard deduction and then just randomly add a few extra things—like your favorite charitable gifts—right on top of it. Unfortunately, the federal tax code absolutely does not work that way. It is a strictly rigid “either/or” choice with very few exceptions.

Once you firmly choose to take the standard deduction, your individual, real-world expenses essentially stop mattering for your federal tax return entirely. You cannot get the massive automatic discount and also ask for special treatment on your out-of-pocket medical bills; you must pick a lane and stay in it.

The Audit Fear Factor

Far too many honest people deliberately avoid itemizing because they are utterly terrified of triggering an IRS audit. While it is technically true that itemized returns feature more line items and are therefore scrutinized slightly more by IRS algorithms, it is absolutely not something to fear if you are being truthful.

The IRS’s internal computers assign a “DIF score” to every return, looking for bizarre anomalies—like a person making $40,000 claiming $30,000 in charity. The IRS is not aggressively looking to punish you for taking legitimate, legal deductions. As long as you have the physical or digital receipts to prove you actually spent the money you claimed, an audit is just a boring paperwork hassle, not a criminal investigation.

Work Expenses for Employees

A massive number of people still operate under the outdated belief that they can broadly deduct their steel-toe work boots, their home office internet, or their monthly union dues. For standard W-2 employees, those specific “miscellaneous” deductions were entirely wiped out of the tax code several years ago. If you receive a standard paycheck from an employer, those daily work expenses do absolutely nothing to help you itemize.

There are rare exceptions for active-duty armed forces or K-12 educators, but the general rule stands. However, if you are an independent freelancer or a 1099 business owner, those costs are considered standard business expenses and are deducted entirely separately from this standard vs itemized debate.

Final Thoughts

At the end of the day, the fundamental choice between the standard vs itemized deduction comes down to one distinctly clear goal: keeping your legally taxable income as low as humanly possible. For the vast majority of ordinary people, the utter simplicity and historically high cash value of the standard deduction make it the undisputed winner. It functions as a massive, entirely automatic financial gift from the IRS that saves you precious time, eliminates paperwork stress, and protects you from audit anxiety.

However, life happens fast, and financial situations change. If you recently bought an expensive home, faced a tragic year of high out-of-pocket medical bills, or decided to be exceptionally generous with your charitable donations, itemizing is your legal mechanism to ensure you aren’t overpaying the government. You should absolutely not be afraid of the extra forms or the minor record-keeping required. Sit down, run the basic math, rigorously compare your totals to the updated 2026 IRS limits, and confidently choose the exact path that safely leaves the most money sitting in your personal bank account.

Frequently Asked Questions (FAQs) About Standard vs Itemized Deduction

Can I itemize on my state return but take the standard deduction on my federal return?

In a lot of states, yes, you absolutely can. However, a handful of specific states strictly require you to use the exact same method for both returns. It is incredibly important to verify your specific state’s revenue rules, especially since the state-level standard deduction is frequently much lower than the massive federal one, making state-level itemizing a highly common strategy.

Does taking the standard deduction make me less likely to be audited?

Statistically speaking, yes, it does, primarily because there is significantly less “custom” financial information for the IRS computers to verify. Standard deduction returns are incredibly straightforward and leave very little room for creative accounting errors. That being said, as long as you retain your receipts, an audit on an honest itemized return is truly nothing more than a minor, temporary paperwork hurdle.

What if I find a massive receipt after I have already filed my taxes?

If you stumble across a receipt that is large enough to mathematically change your choice from the standard path to itemizing (or significantly boost your existing itemized total), you are not out of luck. You can legally file an amended return using IRS Form 1040-X to claim the extra cash. You generally have a generous three-year window from the original date you filed to make this retroactive correction.

Are my monthly student loan interest payments part of my itemized deductions?

No, they are not. Student loan interest functions as a highly beneficial “above-the-line” deduction. This means you can legally claim it to lower your taxable income even if you choose to take the flat standard deduction. It is one of the very few tax breaks that completely bypasses the standard vs itemized deduction debate entirely.

Can I deduct my daily gas and commuting costs if I choose to itemize?

Generally speaking, absolutely not. The IRS very strictly considers the financial cost of traveling from your home to your regular, daily place of work to be a purely personal living expense. Even if you meticulously itemize every other part of your life, you cannot deduct your daily gas, bridge tolls, or office parking fees for a standard W-2 job commute.

{kind=link}