We all want to keep more of the money we earn. Taxes take a massive bite out of your paycheck every single month, and they take another huge bite out of your investment growth over time. But there is a completely legal, government-approved way to shelter your cash: tax-advantaged accounts. If you are trying to build real wealth, understanding these tools is non-negotiable.

Whether you are opening your first workplace retirement plan, trying to figure out what to do with a corporate bonus, or looking to optimize your family healthcare spending, navigating the alphabet soup of finance does not have to be a nightmare. You hear acronyms like HSA, FSA, and IRA tossed around in breakrooms and human resources meetings, but rarely does anyone sit down and explain exactly how to use them together efficiently.

I am going to break down exactly how these accounts work, what the newly released 2026 IRS contribution limits are, and how you can use them to hit your financial goals much faster. By the time you finish reading this guide, you will know exactly where your next dollar should go.

Understanding the Power of Tax-Advantaged Accounts

|

Account Type |

Primary Purpose |

Tax Benefit Timing |

2026 Individual Limit |

Key Advantage |

|

HSA |

Medical and Retirement |

Triple tax-free |

$4,400 |

Funds roll over forever |

|

FSA |

Short-term Medical |

Pre-tax |

$3,400 |

Full funds available Day 1 |

|

401(k) |

Retirement Savings |

Pre-tax or After-tax |

$24,500 |

Employer matching |

|

IRA |

Retirement Savings |

Pre-tax or After-tax |

$7,500 |

Infinite investment choices |

Most people start their investing journey by opening a standard brokerage account at a popular firm. You put your leftover cash in, buy some index funds, and watch it grow over the years. But standard accounts offer absolutely zero tax protection for your money. This means you pay income tax on the money before you invest it, you pay taxes on the dividends it generates every year, and you pay capital gains tax when you eventually sell. Tax-advantaged accounts completely flip this script. By utilizing these specialized accounts, you legally avoid taxes at various stages of your wealth-building timeline, allowing your compound interest to accelerate without a constant drag.

How Tax-Advantaged Accounts Build Wealth?

The real secret behind these accounts is compounding interest combined with extreme tax efficiency. Because the government is either deferring your taxes or eliminating them entirely on the growth of your investments, your money compounds much faster than it would in a standard taxable account. Think of taxes as a heavy anchor attached to a speedboat; if you cut the anchor line, the boat naturally moves faster.

If you invest $500 a month for thirty years at an eight percent return, a taxable account will lose tens of thousands of dollars to annual dividend taxes and eventual capital gains taxes. Inside a sheltered account, every single penny stays yours to compound year over year. Over a working lifetime, maximizing these shelters can literally result in hundreds of thousands of extra dollars in your pocket just by changing the “location” of your investments.

Pre-Tax vs. After-Tax Contributions

To make the absolute most of these accounts, you need to deeply understand the difference between pre-tax and after-tax money. Pre-tax contributions are made with money you have not yet paid any income tax on. When you put money into a pre-tax account, your taxable income for that specific year goes down, giving you an immediate break on your tax return. The catch is that you will eventually owe taxes when you pull the money out during retirement.

After-tax contributions, often called Roth contributions, are made with money that has already been taxed by the government. You get no immediate tax break today, but the massive benefit is that your money grows completely tax-free forever. Choosing between the two usually comes down to a simple guess: do you think your tax bracket is higher right now, or will it be higher in retirement?

Health Savings Accounts (HSA): The Ultimate Savings Tool

|

HSA Feature |

2026 IRS Rules |

Strategic Detail |

|

Individual Limit |

$4,400 |

Covers just the employee |

|

Family Limit |

$8,750 |

Covers employee plus dependents |

|

Age 55+ Catch-up |

$1,000 |

Extra allowance for older workers |

|

Rollover Rule |

Funds never expire |

Stays with you if you quit |

If financial planners had to pick a favorite account, the Health Savings Account would win easily every single time. Despite the boring name, this is not just a temporary place to park cash for your next dental cleaning or prescription refill. It is secretly the most powerful retirement wealth-building tool hiding in the United States tax code. To open one, you just need to be actively enrolled in a qualifying high-deductible health plan. Let us look at why this specific account deserves the top spot in your financial toolkit and why you should fund it aggressively.

How a Health Savings Account Works

An HSA is a specialized account designed to help people save for major and minor medical expenses. However, you cannot be enrolled in Medicare, and you cannot be claimed as a dependent on someone else’s tax return to legally use one. Unlike regular checking accounts at your local bank, the funds inside an HSA can actually be invested directly into the stock market.

Your money does not just sit there losing purchasing power to inflation over the years. You can buy the exact same index funds and stocks that you hold in your standard retirement accounts. Furthermore, the money in your HSA rolls over from year to year indefinitely. You never lose your unspent funds, and the account stays with you permanently even if you quit your job, get fired, or change health insurance plans down the road.

2026 HSA Contribution Limits

The Internal Revenue Service updates contribution limits regularly to keep pace with rising inflation and healthcare costs. For the 2026 tax year, the limits saw a very nice bump for savers. If you have a self-only health coverage plan, you can put up to $4,400 into the account for the entire calendar year. If you have family coverage, the limit jumps massively to $8,750.

Older adults get a bonus benefit to help them prepare for higher medical costs late in life. If you are 55 or older, you are eligible to make an additional catch-up contribution of $1,000 per year. Just remember that if your employer puts money into your HSA as a workplace perk, you must subtract that exact amount from your personal contribution limit so you do not accidentally overcontribute and face tax penalties.

The Triple Tax Advantage of an HSA

The primary reason the HSA is so universally beloved by finance experts is its unique triple tax advantage. Literally no other account in the tax code offers this specific combination of wealth-building benefits. First, your initial contributions are entirely tax-deductible, lowering your overall tax bill for the year. Second, the money inside the account grows tax-free without any annual drag from dividend taxes.

Third, withdrawals are completely tax-free as long as you spend the money on qualified medical expenses like doctor visits, prescriptions, eyeglasses, and even certain over-the-counter medications. If you stay healthy and do not need the money for medical care, the HSA eventually acts exactly like a traditional retirement account. Once you turn 65, you can withdraw funds for non-medical expenses without the normal twenty percent penalty; you just pay normal income tax on those specific withdrawals.

Who Should Consider an HSA?

Anyone who is generally healthy, has a solid emergency fund in the bank, and has access to a high-deductible health plan should strongly consider maxing out an HSA. If you can afford to pay for your minor medical expenses out of pocket right now while leaving your HSA funds invested in index funds, the account will grow into a massive, tax-free medical nest egg for your retirement years.

The ultimate strategy involves saving all your medical receipts for decades. Because there is currently no time limit on reimbursing yourself, you can let your investments grow tax-free for thirty years, and then cash in those old receipts during retirement to pull out massive sums of money completely tax-free to spend on whatever you want.

Flexible Spending Accounts (FSA): Short-Term Medical Savings

|

FSA Feature |

2026 IRS Rules |

Strategic Detail |

|

Standard Limit |

$3,400 |

For standard healthcare costs |

|

Carryover Limit |

$680 |

Maximum allowed to roll over |

|

Dependent Care Limit |

$7,500 per household |

For daycare and preschool |

|

Availability |

Day 1 of plan year |

Full amount ready immediately |

While they sound incredibly similar to Health Savings Accounts, Flexible Spending Accounts serve a very different, much more immediate purpose. An FSA is an employer-sponsored benefit that allows you to set aside pre-tax dollars to pay for immediate, out-of-pocket healthcare costs you expect to incur this year. It is not an investment vehicle, but it is a fantastic way to get an instant discount on your highly predictable medical bills and family care costs.

How a Flexible Spending Account Works?

During the open enrollment period at your job, you decide exactly how much money you want to contribute to your FSA for the upcoming calendar year. Your employer then deducts a portion of that total from each paycheck before your income taxes are calculated. You usually get a designated debit card to use those funds seamlessly for eligible expenses like copayments, daily medications, and necessary medical equipment.

One incredibly helpful and unique feature of an FSA is that your entire elected annual amount is available to you on the very first day of the plan year. Even if you have only made one small paycheck contribution in January, you can spend your entire thousands-of-dollars balance to pay for an early-year surgery or major dental procedure.

2026 FSA Contribution Limits

For 2026, the maximum contribution limit for a standard healthcare Flexible Spending Account is $3,400 per employee. If you are legally married and your spouse also has access to an FSA through their specific job, they can also contribute up to the maximum limit in their own separate account. This doubles your household tax savings on medical costs.

Additionally, there is a completely separate category called a Dependent Care FSA, which carries a much higher limit of $7,500 per household for 2026. This specific account allows you to pay for highly expensive childcare needs like daycare, after-school programs, or preschool with pre-tax money, which can save working parents thousands of dollars annually.

HSA vs. FSA: What is the Difference?

The absolute biggest difference between an HSA and an FSA is the strict expiration date attached to the money. An FSA operates on a rigid use-it-or-lose-it rule enforced by the government. If you do not spend the money in your FSA by the end of the year, you generally forfeit that remaining balance right back to your employer.

For 2026, the IRS does allow employers to let you carry over up to $680 into the next year, but employers are not legally required to offer this grace feature. You also cannot invest FSA money in the stock market. Because of these heavy restrictions, you should only contribute exactly what you know you will definitely spend on medical care within that specific calendar year to avoid throwing your own money away.

401(k) Plans: The Foundation of Retirement Planning

|

401(k) Feature |

2026 IRS Rules |

Strategic Detail |

|

Employee Limit |

$24,500 |

Max personal contribution |

|

Age 50+ Catch-up |

$8,000 |

Extra room for older workers |

|

Age 60-63 Catch-up |

$11,250 |

New super catch-up tier |

|

Total Limit |

$72,000 |

Includes employer match |

The 401(k) plan is the absolute bread and butter of retirement savings in the United States. Sponsored entirely by your employer, it allows you to automatically divert a portion of your regular paycheck into an investment portfolio before you ever even see the money hit your checking account. This psychological automation is the secret to why the 401(k) creates so many everyday millionaires. You set the system up once, and the wealth builds quietly in the background over decades.

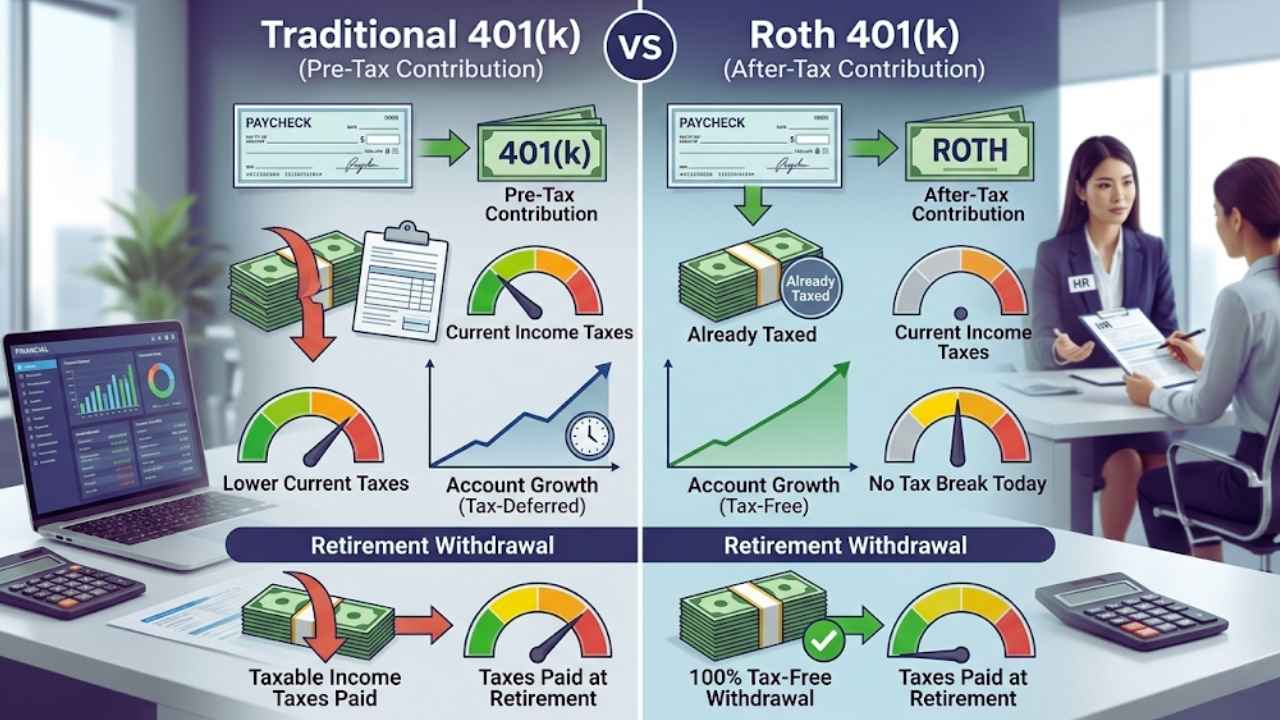

Traditional 401(k) vs. Roth 401(k)

When setting up your workplace plan with human resources, you usually have to choose between a traditional and a Roth option. A traditional 401(k) takes money straight out of your paycheck before your income taxes are applied. This drastically reduces your tax burden today, which is incredibly helpful if you make a high salary right now and want to lower your tax bracket.

Your money grows tax-deferred, and you will pay ordinary income taxes when you finally withdraw it in retirement. A Roth 401(k) operates in the exact reverse manner. You contribute money that has already been taxed by the government. There is no tax break today, but your investments grow completely tax-free, and you will never pay another dime in taxes on the withdrawals later in life.

2026 401(k) Contribution Limits

The IRS sets very strict legal limits on exactly how much you can funnel into your workplace plans to prevent the ultra-rich from hoarding wealth entirely tax-free. For the 2026 tax year, the standard employee contribution limit increased nicely to $24,500. If you are 50 or older, you get a standard catch-up contribution of $8,000 to help you sprint toward the finish line.

But there is a relatively new rule for older workers that you must know. If you are aged 60 to 63, you get a special super catch-up allowance of $11,250 for 2026. The absolute maximum limit, which includes your personal paycheck contributions plus whatever your employer puts in as a match or profit-sharing bonus, sits at a massive $72,000 for the year.

Understanding the Employer Match

The absolute best, most lucrative feature of a standard 401(k) plan is the employer match. Many competitive companies offer to match your personal contributions up to a certain percentage of your base salary. For instance, they might offer a dollar-for-dollar match up to five percent of your total pay. This is quite literally free money placed directly into your portfolio. If you earn $100,000 and contribute $5,000 to your 401(k), your employer injects another $5,000 into your account immediately.

This represents a guaranteed 100 percent return on your investment before the stock market even opens for the day. Failing to capture your full employer match is mathematically identical to rejecting a portion of your salary. You also need to check your vesting schedule to see how long you must stay at the company before that match permanently belongs to you.

Early Withdrawal Penalties and Rules

The government generously provides these massive tax advantages because they desperately want you to leave the money alone until you are truly ready to retire. Because of this intended design, tapping into your 401(k) early comes with incredibly heavy financial consequences. If you withdraw funds before the age of 59 and a half, you will generally face a ten percent early withdrawal penalty.

On top of the harsh penalty, you will owe standard income taxes on the entire amount withdrawn, which could push you into a higher tax bracket for the year. Treating your 401(k) as an emergency fund is one of the most destructive financial mistakes you can possibly make. There is an exception called the Rule of 55, which allows you to withdraw penalty-free if you leave your job in the year you turn 55 or later, but you must keep the money in that specific employer’s plan to use it.

Individual Retirement Accounts (IRA): Expanding Your Investment Options

|

IRA Feature |

2026 IRS Rules |

Strategic Detail |

|

Standard Limit |

$7,500 |

Shared between Trad and Roth |

|

Age 50+ Limit |

$8,600 |

Includes catch-up allowance |

|

Access |

Open at any brokerage |

Complete control over platform |

|

Investment Choices |

Nearly unlimited |

Stocks, ETFs, mutual funds |

While a 401(k) is heavily tied to your specific workplace, an Individual Retirement Account is something you open entirely on your own through a commercial brokerage firm like Vanguard, Fidelity, or Charles Schwab. An IRA gives you complete, unfiltered control over your money. You choose exactly where the account is held, and you get access to thousands of different investment options on the open market. This is a massive upgrade compared to the highly limited, and often expensive, menu of mutual funds usually offered by a standard corporate 401(k) plan.

Traditional IRA vs. Roth IRA

Just like workplace plans, individual retirement accounts come in two very distinct flavors. A traditional IRA allows you to make pre-tax contributions, potentially lowering your tax bill for the current calendar year. A Roth IRA requires you to contribute after-tax money from your bank account. You get no immediate tax deduction when filing your return, but the money grows tax-free forever.

Roth IRAs have an incredible superpower regarding early withdrawals that you need to know. Because you have already paid taxes on the principal money you put in, you are legally allowed to withdraw your original contributions at any time without paying taxes or penalties. You just cannot touch the investment profits or earnings early without triggering a penalty.

2026 IRA Contribution Limits

Because an IRA is a purely individual account unlinked to a corporation, the contribution limits are much lower than workplace plans. For the 2026 tax year, the standard limit is capped at $7,500. This strict limit applies to all your IRAs combined across all brokerages.

You absolutely cannot put $7,500 into a traditional IRA and another $7,500 into a Roth IRA in the exact same year. If you try, the IRS will hit you with an overcontribution penalty. If you are aged 50 or older, you get a small catch-up allowance of $1,100, bringing your total maximum IRA contribution for 2026 to $8,600.

Income Limits and Phase-Out Rules for 2026

It is incredibly vital to understand that the IRS heavily restricts who can fully utilize these individual accounts based on their annual income. If you make too much money, your ability to legally use an IRA starts to quickly disappear. If you or your spouse are covered by a workplace retirement plan, your ability to deduct traditional IRA contributions phases out entirely as your income rises.

For a Roth IRA, there are strict income ceilings that dictate whether you are allowed to contribute at all. High earners are completely barred from making direct contributions to a Roth IRA. However, wealthy investors often use a strategy called the Backdoor Roth conversion. This involves putting after-tax money into a traditional IRA first, and then immediately converting it to a Roth IRA to legally bypass the income limits.

Strategies for Prioritizing Your Tax-Advantaged Accounts

|

Priority Step |

Account Target |

Goal |

Strategic Detail |

|

Step 1 |

401(k) Match |

Get the free money |

100% instant return on investment |

|

Step 2 |

HSA |

Maximize triple tax savings |

Best long-term medical strategy |

|

Step 3 |

IRA |

Access better investment choices |

Lower fees, better stock options |

|

Step 4 |

401(k) Remainder |

Lower taxable income further |

Push toward the $24,500 limit |

Knowing exactly how these complex accounts work is only half the battle of personal finance. The real challenge is knowing exactly what specific order to fund them in to maximize your returns. Most normal people simply do not have enough disposable income to reach the maximum limits on every single account at the exact same time. You need a logical, math-based priority system to ensure every single dollar is working as efficiently as possible for your future self without locking up cash you might need today.

Step 1: Secure Your Free Money

Your absolute first priority should always be your workplace 401(k), but strictly only up to the point of your employer match. There is absolutely no investment in the entire world that will give you a guaranteed 50 or 100 percent return instantly without any risk.

You should view the employer match as a mandatory, non-negotiable part of your total compensation package. Contribute whatever exact percentage of your salary is required to capture every single dollar your company is willing to give you before doing anything else. Leaving the match on the table is the biggest financial error you can make.

Step 2: Maximize Your Healthcare Savings

Once you have firmly secured your employer match, aggressively divert your remaining investment dollars toward a Health Savings Account if you are actively eligible for one. Because of the globally unmatched triple tax advantage, the HSA is mathematically the absolute most efficient wealth-building tool in your entire arsenal.

Aim to push hard to max out the $4,400 individual or $8,750 family limit for 2026. Invest the funds aggressively in low-cost, broad-market index funds and let them grow entirely untouched for decades. Pay for your current copays out of your regular checking account so the HSA can compound without interruption.

Step 3: Fund Your Individual Accounts

After successfully maximizing your HSA, turn your attention toward an Individual Retirement Account. Because a standard corporate 401(k) often comes loaded with high administrative fees and poor fund choices, an IRA provides a highly welcome escape route.

Opening a Roth IRA at a trusted, low-cost brokerage gives you complete freedom to invest in practically any stock, bond, or ETF you want, usually with absolutely zero trading fees. Work diligently toward maxing out the $7,500 limit for 2026. A Roth IRA is particularly attractive and powerful for young workers who expect their salaries and tax brackets to be substantially higher later in life.

Step 4: Maximize the Remaining Workplace Options

If you are a highly diligent saver and have successfully managed to capture your employer match, max out your HSA, and fully fund your IRA, you still have some great options. At this final point, you should return your attention to your workplace 401(k).

You have already secured the match, but you still have tens of thousands of dollars in tax-advantaged space remaining before you hit the strict $24,500 limit for 2026. By continually increasing your 401(k) payroll contributions with every annual raise or bonus you receive, you can drastically reduce your current taxable income while aggressively building an unstoppable nest egg.

Final Thoughts

Building generational wealth is not just about how much money you manage to make at your day job; it is mostly about how much money you actually get to keep out of the hands of the government. By intelligently utilizing tax-advantaged accounts, you give your investments the ultimate legal shield against aggressive tax drag. Start by securing your absolutely free employer match, aggressively fund your HSA if you have the cash flow, and build out your individual accounts to gain ultimate control over your portfolio.

The updated 2026 limits give you vastly more room than ever before to aggressively shelter your cash. Take a quiet hour this weekend to review your human resources payroll settings and make sure you are actively squeezing every possible financial benefit out of your tax-advantaged accounts. Your future self will undoubtedly thank you for taking the time to set this up correctly.

Frequently Asked Questions (FAQs) About Tax Advantaged Accounts

Can I have both an HSA and an FSA at the same time?

Generally speaking, no. The IRS strictly prohibits you from contributing to a standard healthcare Flexible Spending Account and a Health Savings Account at the exact same time. Both accounts are explicitly designed to cover the exact same medical expenses, and the government simply does not want you double-dipping on major tax breaks. There is, however, one small exception to this rule. You are legally allowed to pair an HSA with a Limited Purpose FSA. This is a highly specific account strictly restricted to covering dental and vision expenses only, leaving your HSA alone to cover major medical bills.

What happens to my 401(k) if I leave my job?

Your money always legally belongs to you. When you eventually leave a job, you generally have a few solid choices to make. You can leave the money sitting in your old employer’s plan, though you might get hit with suddenly higher administrative fees as an ex-employee. You can seamlessly roll the money over into your new employer’s plan if they actively allow it. The absolute best option for most people is usually a direct rollover into a personal traditional IRA. This preserves the tax-advantaged status of your money perfectly while giving you total, unfiltered control over the investments and drastically minimizing your ongoing fees.

Can I contribute to a 401(k) and an IRA in the exact same year?

Yes, absolutely. The contribution limits for corporate workplace plans and individual retirement accounts are completely separate from one another under the tax code. In 2026, a focused individual under the age of 50 could theoretically max out their 401(k) at $24,500 and simultaneously max out their IRA at $7,500, successfully sheltering a grand total of $32,000 from taxes in a single year. You just have to carefully remember to monitor the strict income limits for traditional IRA deductions to ensure you still get the tax break.

What happens to my HSA if I pass away?

HSAs have very specific inheritance rules that you need to be aware of for estate planning. If you explicitly name your legal spouse as the designated beneficiary, the HSA simply becomes their HSA tax-free, and they can continue using it for their own medical expenses. However, if you leave the HSA to anyone other than your spouse, like a child or sibling, the account immediately loses its tax-advantaged HSA status upon your death. The entire fair market value of the account becomes fully taxable income to that specific beneficiary in the year you pass away, which can create a massive unexpected tax bill for them.

At what age must I start taking withdrawals from my retirement accounts?

The government will eventually force you to start paying taxes on your pre-tax accounts because they want their cut before you die. These forced, mandatory withdrawals are officially called Required Minimum Distributions. Currently, the law states that you must actively begin taking these calculated mandatory withdrawals from your traditional 401(k) and traditional IRA starting precisely at age 73. This specific age limit is scheduled by law to jump to 75 in the year 2033. It is incredibly important to note that Roth IRAs do not have Required Minimum Distributions during your lifetime, allowing the money to grow tax-free forever.

{kind=link}