Getting your money to work for you starts with one step: picking the right platform. When you sit down to choose brokerage account 2026, you’re looking at a market that looks totally different from what your parents used. Zero-commission trades are table stakes today.

Fractional shares let you buy into massive tech companies with spare pocket change, and mobile interfaces look sleeker than your favorite social media apps.

But a slick design doesn’t mean the platform fits your actual financial goals. You need an account that lines up with how you plan to trade. Are you buying basic index funds every payday and ignoring them? Or do you want to actively buy and sell individual stocks on your lunch break? I constantly see beginners make a massive mistake—they download a heavy-duty trading terminal when all they need is a simple “buy” button. Or worse, they grab a basic app only to realize later they’re paying huge hidden fees for options trading.

Let’s cut the Wall Street jargon and flashy marketing. Here is exactly what to look for, the hidden traps you need to dodge, and how to pick the perfect home for your cash this year based on real 2026 market data.

Know Your True Investing Style

Before comparing platforms, take a hard look at your own habits. Brokers design their software for specific types of people. If you pick a broker built for day traders but you just want to buy a few mutual funds, you’ll end up frustrated and overwhelmed by the dashboard.

You generally fall into one of three groups:

- The Set-and-Forget Investor: You want to deposit cash, answer a few questions about your risk tolerance, and let an algorithm do the heavy lifting. If that sounds like you, a robo-advisor like Betterment or Wealthfront is your best bet. They take a tiny management fee (usually around 0.25%) and automatically rebalance a diversified portfolio for you.

- The DIY Long-Term Investor: You want to pick your own Exchange Traded Funds (ETFs) or solid blue-chip stocks, but you aren’t staring at price charts all day. You just need a clean, reliable app that doesn’t spam you with notifications. Standard brokers like Vanguard or Fidelity fit perfectly here.

- The Active Trader: You want detailed Level II market data, advanced options trading capabilities, margin accounts, and lightning-fast execution speeds. You need a powerhouse platform that gives you deep analytics, like Interactive Brokers or Charles Schwab’s thinkorswim suite.

|

Investing Style |

Effort Level |

What You Actually Do |

Best Platform Type |

|

Hands-Off |

Very Low |

Deposit cash, algorithms handle the rest. |

Robo-Advisor (Betterment, Wealthfront) |

|

DIY Long-Term |

Medium |

Pick ETFs/stocks, hold for years. |

Standard Broker (Fidelity, Vanguard) |

|

Active Trader |

High |

Read charts, trade frequently, use options. |

Advanced Platform (thinkorswim, Webull) |

Types of Accounts You Actually Need

Once you understand your style, you have to figure out the actual account type you want to open. This is where people make expensive mistakes. The government taxes different accounts in drastically different ways. Put your cash in the wrong bucket, and you might hand a massive chunk of your hard-earned profits straight to the IRS.

A taxable brokerage account is the default option. You link your bank account, transfer money, and buy stocks. There are no limits on how much money you can put in, and you can pull your money out whenever you want without penalty. The catch? You owe taxes every year on the dividends you receive and on any profits you make when you sell a stock for more than you paid for it (capital gains).

If you want to invest for retirement, you need an Individual Retirement Account (IRA). A Traditional IRA lets you deduct your contributions from your taxes right now, but you pay taxes when you withdraw the money decades later.

A Roth IRA is the golden ticket for most beginners. You fund it with money you already paid taxes on. Your money grows completely tax-free forever. When you pull it out after age 59½, you don’t owe the government a single dime on the profits. The IRS bumps contribution limits regularly to account for inflation. For 2026, the maximum you can put into an IRA is $7,500 if you’re under 50, and $8,600 if you’re 50 or older. If you plan to choose brokerage account 2026 options for long-term wealth, make sure the broker supports IRAs with zero annual maintenance fees.

|

Account Type |

Tax Advantage |

Withdrawal Rules |

Best Use Case |

|

Taxable Account |

None. Pay taxes on gains/dividends. |

Pull money out anytime without penalty. |

General wealth building, short-term goals. |

|

Traditional IRA |

Tax-deductible contributions now. |

Penalties before age 59½. Taxed on exit. |

High earners wanting lower taxes today. |

|

Roth IRA |

Tax-free growth and tax-free withdrawals. |

Penalties on earnings before 59½. |

Long-term retirement, tax-free millions. |

|

529 Plan |

Tax-free growth for education expenses. |

Must be used for qualified education costs. |

Saving for a child’s college or trade school. |

The Truth About “Zero Fee” Trading in 2026

You’ll see “commission-free trading” plastered across almost every financial website today. Don’t fall for the marketing trap. Businesses exist to make money. If they aren’t charging you a flat $4.95 fee every time you buy a stock like they did a decade ago, they’re making their money somewhere else.

The biggest way they profit is through Payment for Order Flow (PFOF). When you click buy, your broker sends your order to a massive market maker to actually execute the trade. The market maker gives your broker a tiny fraction of a penny for routing the trade to them. For basic, long-term investors buying 10 shares of an ETF, PFOF doesn’t really impact you. But if you day trade, you might get a slightly worse execution price on your stock because of it.

You also must watch out for margin rates. If you borrow money from your broker to trade, interest rates will eat your profits alive. Based on current 2026 data, margin rates range wildly. For balances under $25,000, major brokers like Fidelity charge 11.825% annually. Meanwhile, platforms catering to active traders like Interactive Brokers offer base rates as low as 4.12% to 6.12% depending on your tier. Borrowing $10,000 at 11.8% costs you nearly $1,200 a year in interest.

Finally, hunt down the hidden exit fees. Look closely at mutual fund transaction costs. A broker might charge you $50 every time you buy a mutual fund that isn’t on their “preferred” list. Also, check for transfer (ACAT) fees. If you hate your broker and want to move your portfolio to a competitor, the old broker might slap you with a $75 or $100 exit fee.

|

Fee Type |

What It Actually Is |

Average 2026 Cost |

How to Avoid It |

|

Trade Commissions |

Cost to buy/sell U.S. stocks or ETFs. |

$0 |

Stick to modern online brokers. |

|

Margin Interest |

Interest on money borrowed to trade. |

4% to 12% annually |

Trade with cash only, or compare top tiers. |

|

Options Fees |

Cost per options contract. |

$0.50 – $0.65 per contract |

Hard to avoid, but compare base rates. |

|

Mutual Fund Fees |

Cost to buy third-party mutual funds. |

$20 – $50 per trade |

Buy ETFs instead, or use broker’s own funds. |

|

Transfer (ACAT) Fee |

Cost to move your whole account elsewhere. |

$75 – $100 |

Ask the new broker to reimburse you. |

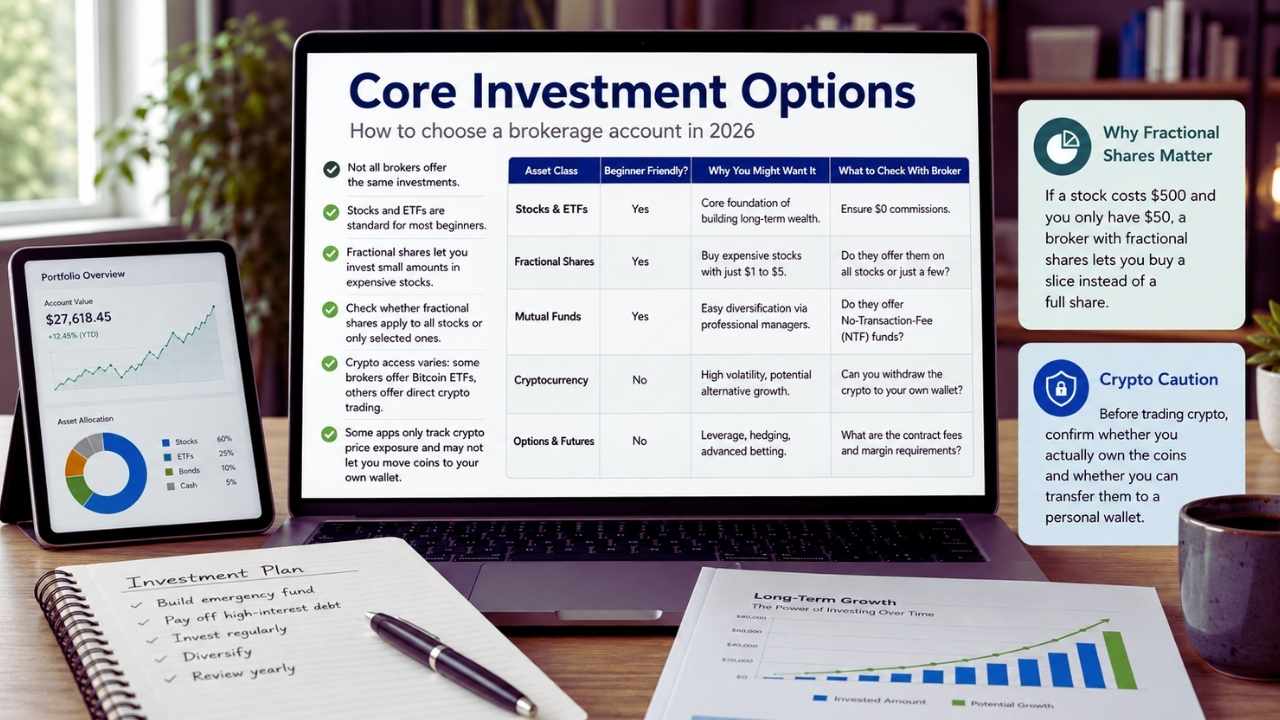

How to choose a brokerage account in 2026: Core Investment Options

Not all platforms sell the exact same products. A major factor that should guide you as you choose brokerage account 2026 candidates is whether they actually offer the assets you want to own.

Virtually everyone offers basic US stocks and ETFs. But what about fractional shares? Let’s say a stock you want costs $500 a share, but you only have $50 to invest this week. A broker with fractional shares lets you buy exactly $50 worth of that company. You own a “slice” of the pie. If you’re starting with a small amount of cash, fractional share availability is an absolute dealbreaker. Read the fine print, though. Fidelity offers fractional buying for almost any company, while Schwab only allows it on S&P 500 stocks.

If you want to trade cryptocurrency, check the platform’s policies. Traditional brokers generally let you buy Bitcoin ETFs, while others like Robinhood or eToro have separate crypto trading desks. Be careful here: some apps let you trade the price of crypto, but you don’t actually own the coins and can’t move them to a cold hardware wallet.

|

Asset Class |

Beginner Friendly? |

Why You Might Want It |

What to Check With Broker |

|

Stocks & ETFs |

Yes |

Core foundation of building long-term wealth. |

Ensure $0 commissions. |

|

Fractional Shares |

Yes |

Buy expensive stocks with just $1 to $5. |

Do they offer them on all stocks or just a few? |

|

Mutual Funds |

Yes |

Easy diversification via professional managers. |

Do they offer No-Transaction-Fee (NTF) funds? |

|

Cryptocurrency |

No |

High volatility, potential alternative growth. |

Can you withdraw the crypto to your own wallet? |

|

Options & Futures |

No |

Leverage, hedging, advanced betting. |

What are the contract fees and margin requirements? |

Platform Tech and the Mobile App Experience

We live on our phones, and your brokerage app needs to be bulletproof. A clunky interface causes expensive mistakes. If it takes you five menus and three confirmation screens just to find a ticker symbol, you’ll give up.

Download the apps of your top choices before you fund an account. Most let you look around or open a “paper trading” account first. Paper trading is a simulator that lets you practice buying and selling with fake money using live market data. Pay attention to how the app presents information. Does it push you toward risky, highly volatile stocks? Some apps use heavy gamification to encourage you to trade more often. Remember, the more you trade, the more money they make. Stick to platforms that feel professional and put your long-term goals first.

Check out the research tools. Do they give you free access to independent Morningstar reports? Can you easily see a company’s earnings history, P/E ratio, and dividend yield? Great brokers want you to succeed, so they offer free webinars, detailed articles, and video courses explaining everything from basic budgeting to complex options strategies.

|

Platform Feature |

What It Does |

Why You Need It |

|

Clean Mobile App |

Lets you trade easily from your phone. |

Prevents mistakes; saves time. |

|

Paper Trading |

Simulates the stock market with fake cash. |

Practice strategies without losing real money. |

|

Free Research |

Provides professional analyst reports. |

Helps you evaluate a stock’s actual worth. |

|

Educational Hub |

Videos and articles on financial literacy. |

Builds your investing knowledge over time. |

|

Dividend Reinvestment |

Automatically uses dividends to buy more shares. |

Compounds your wealth effortlessly over decades. |

Customer Service, Security, and SIPC Protection

When everything goes well, you never think about customer support. But imagine waking up, checking your app, and seeing a zero balance because of a technical glitch. In that moment, you want a real human being on the phone immediately.

Test the customer service before you commit. Try calling their support line or using their live chat. If you sit on hold for an hour just to ask a basic account question, walk away. Brokers like Fidelity consistently score high in consumer sentiment (3.7 out of 5 in recent Forbes 2026 data) for their reliable support. Some traditional brokers still maintain physical branch offices in major cities. If you prefer sitting down with someone face-to-face to sort out complicated paperwork, prioritize legacy brokers.

Security is non-negotiable. Ensure the broker is a member of the Securities Investor Protection Corporation (SIPC). SIPC protects your account up to $500,000 (including $250,000 in cash) if the brokerage firm itself goes bankrupt. Understand that this doesn’t protect you if you make a bad stock pick and lose money—it only protects you from the broker closing its doors permanently.

|

Security & Support Feature |

What It Means |

Red Flags to Avoid |

|

SIPC Insurance |

Protects your assets if the broker fails. |

Broker is not SIPC insured. Run away immediately. |

|

2FA (Two-Factor Auth) |

Requires a second step beyond your password. |

App only uses email/SMS, not authenticator apps. |

|

Live Phone Support |

Speak to a real human when things break. |

Only offers automated AI chatbots for help. |

|

Physical Branches |

Local offices you can walk into. |

(Not a red flag, but an optional nice-to-have). |

Reviewing the Top 2026 Brokerage Heavyweights

Based on 2026 market data, consumer sentiment ratings, and feature sets, a few major players dominate the landscape right now. Choosing the right one depends heavily on whether you want simplicity or raw power.

Fidelity Investments

Ranked highly for overall satisfaction, Fidelity offers $0 commissions, zero-expense-ratio index funds, broad fractional shares, and excellent customer service. They don’t accept Payment for Order Flow on stock trades, meaning you often get better pricing. The main downside is their steep margin rates (11.825% for balances under $25k).

Charles Schwab

Schwab pioneered the discount broker model. They excel in IRA management and offer a fantastic ecosystem that ties your checking account to your brokerage. If you want to grow into active trading, their thinkorswim platform is widely considered the best analytical software on the market.

Robinhood

The undisputed king of mobile-first investing. Robinhood is incredibly easy to use, offers seamless fractional share buying, and allows direct crypto purchases. While active traders might find the charting tools lacking, beginners love the zero-clutter interface.

Interactive Brokers

If you want to trade on over 170 different global markets, this is your home. Interactive Brokers offers some of the lowest margin rates in the entire industry (as low as 4.12% for Pro accounts). However, their flagship trading terminal has a massive learning curve and will easily intimidate a brand-new investor.

To see how these variables interact depending on your deposit size and trading style, try adjusting the parameters below:

|

Broker |

Best For |

Standout Feature |

Drawback |

|

Fidelity |

Best Overall / Beginners |

Zero-expense-ratio index funds. |

Margin rates are very high for small balances. |

|

Charles Schwab |

IRA Investors / Growth |

thinkorswim advanced trading platform. |

Fractional shares limited to S&P 500 stocks. |

|

Robinhood |

Mobile Users / Small Deposits |

Best-in-class simple mobile app. |

Customer support is harder to reach quickly. |

|

Interactive Brokers |

Active / Global Traders |

Rock-bottom margin rates. |

Steep learning curve for the software. |

Final Thoughts

The investing landscape has never been friendlier to absolute beginners. You have access to the exact same data, research tools, and mobile platforms that institutional traders use. But that power means you have to be intentional. Don’t just pick an app because it ran a flashy ad or because a financial influencer dropped a referral link in their bio.

Your job right now is to figure out your exact investing style. Nail down the account type, maximize your tax advantages through an IRA, and relentlessly hunt down hidden fees like high mutual fund loads or massive margin rates. The right move is to choose brokerage account 2026 providers that will scale with you as your net worth grows. Take the time to compare your options, open the account, set up automated monthly deposits, and let the market do the heavy lifting for you.

Frequently Asked Questions (FAQs) About Brokerage Accounts

People run into very specific roadblocks when opening their first accounts. Here are the answers to the questions you actually care about, straight from recent search trends.

Can I have multiple brokerage accounts?

Yes. There’s no legal limit to how many taxable brokerage accounts you can have. Many investors use one steady platform like Vanguard for their long-term Roth IRA and a completely different app like Webull for their “fun money” stock picking.

Do brokers run a hard credit check when I apply?

If you just open a standard cash account to buy basic stocks and ETFs, brokers generally run a “soft pull” to verify your identity and comply with anti-money laundering laws. This doesn’t hurt your credit score. But if you apply for a margin account to borrow money, they’ll likely run a hard inquiry.

What is the difference between FDIC and SIPC?

FDIC protects bank accounts (checking/savings) if your local bank fails. SIPC protects brokerage accounts (stocks/bonds) if your broker fails. Neither protects you from normal market volatility. If the stock market crashes, you lose money. SIPC only kicks in if the broker goes bankrupt and loses track of your assets.

Can I buy a fraction of an ETF, or just stocks?

It depends entirely on the broker. Some let you buy fractions of any stock or ETF on the market. Others only allow fractional buying on individual stocks, forcing you to buy full shares of ETFs. Always verify this before depositing cash.

What is the Pattern Day Trader (PDT) rule?

If you buy and sell the same stock on the same day four or more times within five business days, federal regulations flag you as a Pattern Day Trader. If you use a margin account, the law requires you to keep at least $25,000 in your account to continue day trading. If you use a standard cash account, this rule doesn’t apply to you.

{kind=link}