You ditched the 9-to-5 for freedom, flexibility, and the chance to call your own shots. But nobody warned you about the first of the month. Rent is due, the internet bill just hit, and you’re still refreshing your inbox waiting on three different clients to pay their invoices. The stress is exhausting. Welcome to the freelance cash flow rollercoaster.

Right now, over 76.4 million Americans work independently, generating a massive 1.5 trillion dollars annually. Yet, almost all mainstream financial advice assumes you get a neat, predictable direct deposit every two weeks. When you run a freelance business, you might pull in $9,000 one month and scrape by on $1,500 the next. Standard financial rules just don’t work for this reality.

You need an entirely new system. If you want to budget irregular income without losing sleep, you have to build a framework built for the real world. This playbook cuts the fluff. We’re breaking down exactly how to stabilize your cash flow, handle taxes without panic, and pay yourself a steady salary—even when clients pay late.

Why Standard Budgeting Advice Fails You?

Traditional budgeting frameworks like the 50/30/20 rule tell you to put 50 percent of your income toward needs, 30 percent toward wants, and 20 percent toward savings. That advice completely breaks down when your income drops by 60 percent during a slow month. If you tie your spending to fixed percentages of a moving target, you’ll constantly feel like you’re failing. The real enemy here is the feast or famine cycle.

During a feast month, a massive payment clears, and suddenly upgrading your home office feels totally justified. Then the famine hits, leads dry up, and you scramble just to cover basic utility bills. With average independent incomes hitting $108,028 a year for full-timers, this cash flow crunch is a universal problem. Regular employees get predictable deposits and employer-subsidized benefits, but you absorb every financial shock directly. You fix this by completely decoupling what your business earns from what your household actually spends.

|

Financial Reality |

Traditional Employee |

Independent Freelancer |

|

Pay Timing |

Predictable bi-weekly deposits |

Random, fluctuating payments |

|

Taxes |

Handled automatically by the employer |

Your sole responsibility to withhold |

|

Time Off |

Paid vacation and sick leave |

Zero pay unless you saved for it in advance |

|

Benefits |

Subsidized health & retirement |

100 percent self-funded overhead |

How to Budget Irregular Income with a Survival Baseline

Forget fancy spreadsheets for a minute and focus on finding your absolute floor. You need to know the bare minimum amount of cash required to keep the lights on, feed yourself, and keep your business operational. We call this your Survival Baseline. Pull up your last three months of bank statements and highlight only the expenses you literally cannot ignore. Include rent, basic utilities, supermarket groceries, health insurance, and essential business software like hosting fees.

Do not include takeout, gym memberships, or streaming services. Let’s say those core expenses total $3,200. That becomes your magic number and dictates your entire financial game plan. When you plan your month, your one and only job is to secure that $3,200 before you spend a single dime on anything else. Data shows 45 percent of modern freelancers use AI tools to boost their earning potential, making it easy to assume the money will always flow. But dry spells happen, and knowing your exact baseline keeps you perfectly grounded.

|

Expense Category |

What It Includes |

Priority Level |

|

Survival Baseline |

Rent, basic food, home utilities |

Non-negotiable; fund this before anything else |

|

Business Ops |

Essential software, fast internet |

Must-have to keep your business earning |

|

Minimum Debt |

Loan minimums, credit cards |

Pay immediately to avoid harsh penalties |

|

Discretionary |

Eating out, travel, hobbies |

Cut entirely during your slow months |

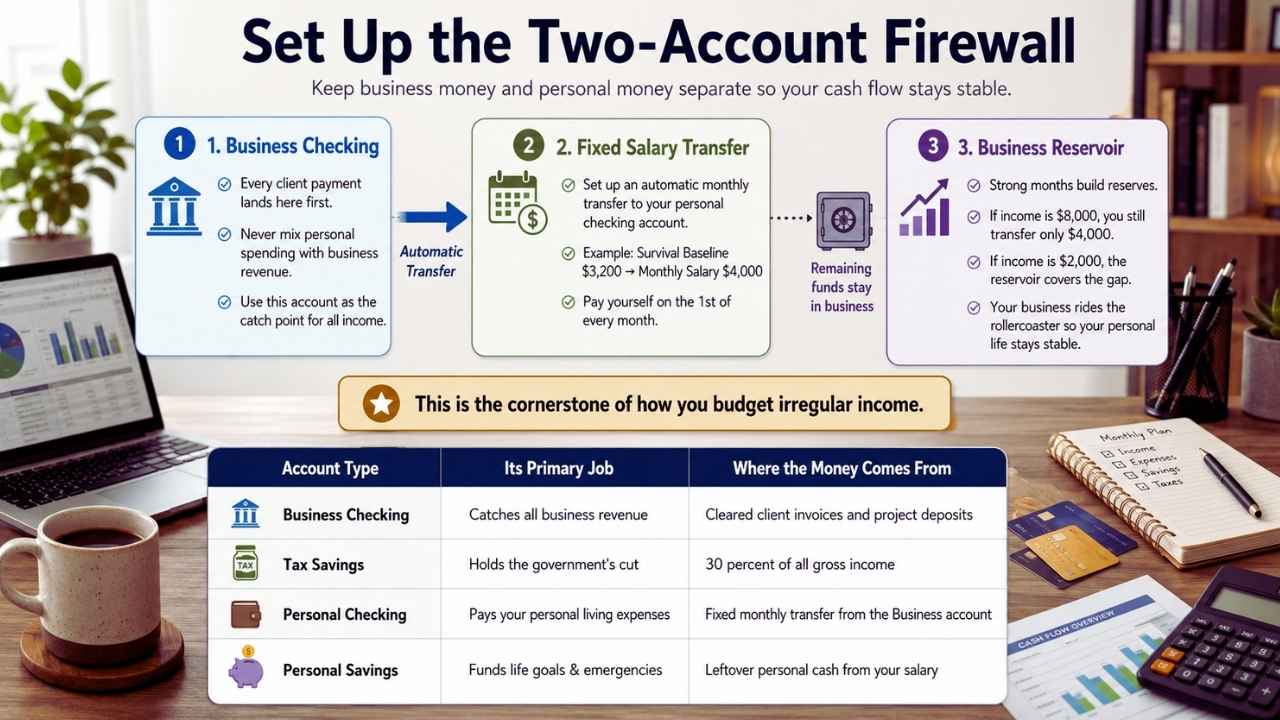

Set Up the Two-Account Firewall

Mixing client funds with your grocery money creates total chaos and guarantees you’ll mismanage your cash. You need a strict financial firewall, which starts by opening a dedicated business checking account today. Every single dollar you earn goes into this account first, and you never hand a client your personal routing number. Once the business account catches all the revenue, you set up an automatic, recurring transfer to your personal checking account.

This transfer becomes your fixed salary. Start with your Survival Baseline plus a tiny buffer for discretionary spending. If your baseline is $3,200, pay yourself $4,000 on the first of every month. Some months the business brings in $8,000, but you still only transfer $4,000. The remaining money stays behind, building a massive reservoir. When a slow month hits and you only bring in $2,000, that reservoir covers the difference. This is the cornerstone strategy when you budget irregular income because your business rides the rollercoaster so your personal life stays entirely stable.

|

Account Type |

Its Primary Job |

Where the Money Comes From |

|

Business Checking |

Catches all business revenue |

Cleared client invoices and project deposits |

|

Tax Savings |

Holds the government’s cut |

30 percent of all gross income |

|

Personal Checking |

Pays your personal living expenses |

Fixed monthly transfer from the Business account |

|

Personal Savings |

Funds life goals & emergencies |

Leftover personal cash from your salary |

Tame the Tax Monster

Nothing destroys an independent business faster than a surprise tax bill from the government. Regular employees have their taxes pulled automatically, but the government trusts you to hold their money until tax season. Break that trust, and the financial penalties will wipe you out completely. Every time a client invoice clears, immediately move 30 percent of that money into a high-yield savings account designated strictly for taxes. Do this before calculating your baseline, before paying your salary, and before buying a coffee.

If you get paid $1,000, you have to act like you only received $700. Track your business expenses obsessively to lower your overall tax burden, deducting home office space, internet, and equipment costs. If you operate internationally, lean hard into local tax-saving tools. Freelancers in India should max out Section 80C investments and fund a Public Provident Fund, while US workers should leverage a Solo 401(k) to legally shrink their tax bill.

|

Tax Action |

What It Actually Takes |

Timing & Execution |

|

Save for Taxes |

30 percent of every cleared invoice |

Immediately upon receiving client payment |

|

Pay Estimated Taxes |

Varies heavily by location and income |

Usually quarterly to avoid government penalties |

|

Track Deductions |

Log receipts, travel, and software costs |

Year-round habit using accounting software |

|

Leverage Accounts |

PPF, Section 80C, or Solo 401(k) |

Annually to drastically reduce taxable income |

Build Your “Valley” Fund

Mainstream financial advisors always tell you to build an emergency fund, but independent workers actually need two separate safety nets. A personal emergency fund handles life’s random disasters, like a blown tire, a broken tooth, or a leaky roof. A Valley Fund is strictly for your business cash flow. Freelance work naturally consists of massive hills and deep valleys.

You need cash specifically designed to cover your salary transfers when client work dries up or a major client takes 60 days to process an invoice. As you budget irregular income to protect your household, this buffer absorbs all the professional shock. Aim to stash two to three months of your Survival Baseline directly inside your business checking account. Once that bucket is completely full, you can start investing your heavy profits or booking long vacations without an ounce of guilt.

|

Fund Name |

Target Savings Amount |

When to Actually Use It |

|

Valley Fund (Business) |

2 to 3 months of your baseline |

Client dry spells, late invoices, lost contracts |

|

Emergency Fund (Personal) |

3 to 6 months of living costs |

Medical bills, car repairs, personal disasters |

|

Equipment Sinking Fund |

$1,000 to $3,000 cash reserve |

Dead laptops, broken cameras, outdated gear |

|

Tax Holding Fund |

30 percent of gross revenue |

Strictly for quarterly and annual tax payments |

Handle Windfalls Like a Pro

Eventually, you’ll hit a massive month where a huge project closes or three late invoices clear on the exact same afternoon. You look at your banking app and see a massive five-figure balance staring back at you. The urge to upgrade your apartment, buy a nicer car, or splurge on expensive office furniture is incredibly intense. Do not touch your lifestyle. Inflating your baseline because of one great month is exactly how high-earning freelancers who fail to budget irregular income go completely broke.

Instead, run that extra cash through a strict financial waterfall. First, pull your 30 percent for taxes immediately. Next, top off your Valley Fund so your business buffer is fully funded for the next 90 days. Then, wipe out any high-interest credit card debt for an instant return on your money. Finally, shove the rest into index funds or retirement accounts, taking just a small 5 percent cut to buy something fun to reward your hard work.

|

Priority |

Action for Windfall Cash |

Why You Must Do It |

|

1 |

Secure the Tax Account |

Prevents massive IRS or local tax penalties |

|

2 |

Top off the Valley Fund |

Guarantees next month’s personal salary is safe |

|

3 |

Crush bad high-interest debt |

Instant financial return on your invested money |

|

4 |

Invest & Reward Yourself |

Builds long-term wealth and prevents burnout |

Final Thoughts

Financial mastery doesn’t happen by accident, especially when you step away from the safety of a corporate payroll. The chaos of a fluctuating paycheck is ultimately just a math puzzle, and you solve it by building thick, unshakeable walls between your business revenue and your personal life. Figure out your absolute baseline floor and split up your bank accounts today.

Pay yourself a flat, boring salary, and let your business account take the brutal hits from slow seasons and late-paying clients. When you systematically budget irregular income, you completely stop surviving month-to-month and start building real, generational wealth. It takes serious discipline to play the long game, but the peace of mind you gain is exactly why you became your own boss in the first place.

Frequently Asked Questions (FAQs) About Budget Irregular Income

Should I budget based on my average or lowest month?

Always budget on your lowest historical month. If you budget on an average, you’ll fall short half the time. Lock in your baseline using your worst-case scenario, and treat everything extra as a bonus.

My best client takes 60 days to pay. How do I survive that?

You build a Valley Fund. If you know they operate on Net-60 terms, rely on your business cash buffer to pay your personal salary on time. The client’s money eventually refills the buffer.

How do I handle massive annual bills?

Use sinking funds. If your business insurance is $1,200 a year, divide it by 12. Transfer $100 every month into a sub-account. When the bill hits, the cash is sitting there waiting.

What if my baseline is higher than my income?

You don’t have a budget problem; you have an income problem. You can’t math your way out of this. You need to slash your living expenses, raise your rates today, or grab a part-time job to stabilize the floor while you hunt for better clients.

{kind=link}