You tap your phone against a terminal, grab your coffee, and walk out. You swipe a card for gas. You hit the checkout button on a targeted ad while stuck in traffic. Money moves so incredibly fast today that it barely feels real.

I track digital business trends and fintech platforms daily, and I love a good automated workflow. But honestly, sometimes technology makes spending entirely too frictionless. That endless swiping is exactly why thousands of people are ditching their digital wallets and going backward. They want cold, hard paper.

If you need to stop mindless spending and take your paycheck back, you need physical boundaries. That is exactly what the cash envelope system delivers right to your fingertips. It forces you to look at what you have, feel what you spend, and stop when you hit zero. So, in a world dominated by contactless payments and seamless banking apps, does relying on paper money actually make sense? Let us break down how this retro hack is dominating this year, the psychology behind it, and how you can blend it with modern digital tools to secure your financial future.

What Exactly is the Cash Envelope System?

Building lasting wealth requires the exact same relentless focus and perfect timing you see from a master batsman stepping onto the cricket pitch. You cannot afford a sloppy shot, and you certainly cannot afford careless daily spending. That is exactly where the cash envelope system steps in to act as your ultimate financial defense mechanism. Instead of leaving your money in a checking account where it vanishes into micro-transactions, you pull it out as physical cash.

You divide that cash into specific physical sleeves and label each one with a distinct spending category, like groceries or entertainment. When you go to the store, you exclusively use the cash from that specific category. Once the sleeve is entirely empty, you stop spending immediately and wait until your next payday. You absolutely cannot borrow from your rent money to buy drinks with friends, creating a boundary that is both physical and absolute. This method ensures you give every single dollar a clear purpose before the month even begins.

|

Budgeting Method |

How It Operates |

Who Should Use It |

|

Envelope Method |

Hard physical limits using paper cash |

Chronic overspenders and visual learners |

|

Zero-Based Budget |

Every dollar gets an assigned job on paper |

Detailed planners and spreadsheet fans |

|

60-20-20 Rule |

Broad percentage splits for living, saving, and fun |

Hands-off budgeters needing simplicity |

The Data Behind the 2026 Cash Stuffing Trend

You might think paper money is completely dead, but it actually made a massive comeback over the last couple of years. Younger generations quickly realized that digital budgeting tools were just too easy to swipe away and ignore. The trend exploded on social media under the name “cash stuffing” and rapidly turned into a massive micro-economy. Some creators are pulling in millions a year just selling custom budget binders and aesthetic tracking accessories.

We are actively fighting back against high inflation and highly optimized digital marketing strategies designed to separate us from our money. Research shows modern shoppers make nearly double the impulse purchases compared to older demographics. At the same time, a massive percentage of young adults lack a basic three-month emergency fund to fall back on. People are simply exhausted by digital fatigue and the financial hangover that always arrives at the end of the month.

|

Economic Driver |

The Hard Market Data |

How It Impacts Daily Budgets |

|

Social Media Exposure |

Users make 2x the impulse buys |

High demand for strict spending boundaries |

|

Creator Economy |

Top creators earn massive revenue on tools |

Normalizes paper cash systems globally |

|

Low Emergency Savings |

Over 50% lack a 3-month safety net |

Sparks aggressive and visual saving tactics |

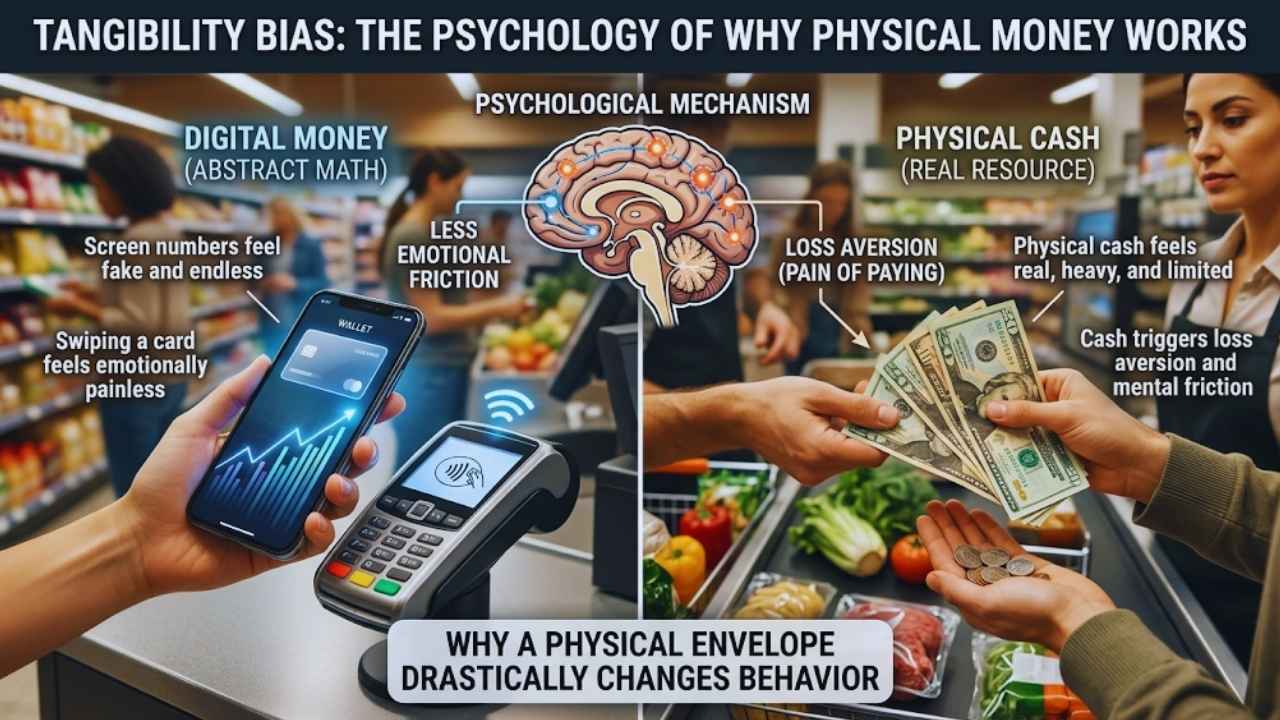

The Psychology: Why Tangibility Bias Works?

Why does a physical envelope drastically change your behavior when an app notification gets easily ignored? It all comes down to how our brains are fundamentally wired to process loss. Money sitting in a bank account is just abstract math on a glowing screen. When you hold physical paper, your brain treats it as a real, highly limited resource that requires protection. Economists call this psychological phenomenon “tangibility bias,” and it dictates how we value our resources.

A famous university study found that shoppers spend up to double the amount when using a credit card compared to spending actual cash. Swiping a plastic card is completely painless and registers zero emotional friction. But handing over a crisp bill and getting back loose change triggers immediate loss aversion in your brain. You naturally track prices closely as you load up your grocery cart, prioritizing what you actually need.

|

Psychological Trigger |

The Problem with Digital Money |

The Physical Cash Solution |

|

Tangibility Bias |

Screen numbers feel fake and endless |

Physical cash feels real, heavy, and limited |

|

Pain of Paying |

Swiping a card feels emotionally painless |

Cash triggers loss aversion and mental friction |

|

Frictionless Buying |

One-click checkouts drive rapid impulse |

Counting bills physically slows down the transaction |

Step-by-Step: Starting Your Cash Envelope System

Setting this framework up takes a little upfront effort, but running it on a daily basis is incredibly straightforward. You absolutely cannot set realistic limits if you do not know where your money currently goes. Pull your bank statements from the last three months, add up what you spent on variable costs, and find your monthly average. Do not ever pull out cash for fixed, recurring bills.

Leave your rent, car payment, internet, and any essential software subscriptions on digital auto-pay. Only use the physical sleeves for the high-friction categories where you usually overspend, keeping it to four or five categories to start. On payday, head directly to the bank or ATM and withdraw the exact cash you budgeted. Divide it up into your labeled sleeves, and when you leave the house, only bring the cash you plan to spend.

|

Implementation Step |

Action You Need to Take |

Professional Tip |

|

1. Run an Audit |

Review your past 90 days of spending data |

Spot your top three problem spending categories |

|

2. Set Categories |

Pick high-friction, daily variable expenses |

Leave all your fixed monthly bills on auto-pay |

|

3. Withdraw & Stuff |

Fill your physical sleeves with the exact cash |

Use durable, clear binders so they do not tear |

|

4. Enforce the Limit |

Cease all spending when the cash hits zero |

Never borrow from another category to cheat |

Managing Online Shopping and Digital Apps

We live in a digital-first economy where ordering online is an unavoidable part of daily life. I know plenty of professionals who refuse to carry physical bills for security reasons. Furthermore, studies show almost half of us overspend on online purchases every single week. If you want to stick to physical paper, you must use a manual tracking trick for online platforms.

Write your starting budget directly on the outside of the sleeve, and when you buy something online with a card, take the physical cash out. Deposit it back into the bank later, or simply use the sleeve as a written ledger to deduct the total. If manual tracking sounds completely awful, you can run a fully digital cash envelope system using modern fintech apps. These banking platforms let you create distinct software pods inside one checking account to mimic the physical limits perfectly.

|

Platform Feature |

Physical Paper Envelopes |

Digital Envelopes and App Pods |

|

Friction Level |

Very High (Requires weekly bank trips) |

Low (Features completely automated tracking) |

|

Online Shopping |

Annoying (Requires manual math and deposits) |

Seamless integration with digital checkouts |

|

Security Risk |

High (Lost or stolen cash is gone forever) |

Low (Protected by bank-level data encryption) |

|

Setup Cost |

Free (Just requires paper and pens) |

Often requires a monthly or annual SaaS fee |

Pros and Cons of a Cash-Only Budget in 2026

Like any financial strategy you implement, this specific framework has massive benefits and a few highly annoying drawbacks. It completely changes how you view your daily income, but it is certainly not for everyone. The biggest advantage is immediate feedback, meaning you never have to log into an app to see if you can buy a coffee. When you hit zero, the spending stops instantly, eliminating any chance of overdraft fees or fresh credit card debt.

It makes daily budgeting feel incredibly satisfying and concrete, forcing a total reset of your spending habits. However, keeping massive amounts of cash at home is risky, and insurance companies constantly warn about increased liabilities for theft or fire. Additionally, if you manage digital businesses, travel frequently, or work remotely, carrying labeled envelopes through airports becomes a logistical nightmare.

|

Assessment Factor |

The Major Upside |

The Noticeable Downside |

|

Spending Limits |

Impossible to accidentally overspend past zero |

Annoying to manage for online digital subscriptions |

|

Mental Mindset |

Uses tangibility bias to successfully curb spending |

Requires an incredibly high level of personal discipline |

|

Personal Security |

Stops digital identity theft and online fraud |

High risk of physical home theft, loss, or fire damage |

Best Practices to Keep the Habit Alive

Strict budgets almost always fail when people quit out of frustration after one single bad month. If you truly want this financial habit to stick long-term, you must build flexibility into your plan. First, you need to keep a small buffer envelope for completely unexpected daily surprises. A quick fifty-dollar buffer keeps one bad day, like a flat tire or a forgotten lunch, from blowing up your entire weekly plan.

Second, you must proactively plan for irregular, massive expenses that you know are coming. Create sinking funds for annual costs, like car maintenance or holiday gifts, by putting a tiny amount of cash away each month. Finally, you have to actively reward your financial success to stay highly motivated. If you have cash left in your grocery sleeve at the end of the month, roll it over or transfer it straight to a high-yield savings account.

|

Daily Scenario |

Best Practice Solution to Implement |

|

Leftover cash at month-end |

Roll it over, transfer to savings, or aggressively pay debt |

|

Irregular annual bills |

Use sinking funds to systematically save a little each month |

|

Unexpected minor costs |

Keep a dedicated buffer sleeve to prevent budget breaking |

Final Thoughts

Technology makes our daily spending completely invisible, but you absolutely do not have to fall into the brutal trap of frictionless debt. Whether you choose to use crisp physical bills, a sleekly designed fintech app, or a smart hybrid of both, the core rule remains the same. You must give every single dollar a dedicated job and build rock-solid boundaries around your daily consumption habits.

The cash envelope system still works flawlessly right now because human psychology simply has not changed in decades. We instinctively respect physical limits far more than we respect abstract numbers glowing on a smartphone screen. By combining the friction of paper money for your daily variable spending with the automation of modern banking for your fixed bills, you build a strategy that aggressively protects your wealth. Try it for the next 30 days. You will be genuinely shocked by how much of your own money you actually get to keep.

Frequently Asked Questions (FAQs) About Cash Envelope System

Does the cash envelope system work if I do not use physical cash?

Yes. You can run a digital version using a budgeting app or bank account buckets. The software acts exactly like cash, updating automatically as you swipe your debit card.

Is keeping this much cash at home safe?

It carries obvious risks. Insurance providers actively warn against keeping loose cash at home. If you go this route, store your main envelopes in a fireproof safe and only carry what you need for the day.

How many envelopes should I start with?

Start small. Trying to track 15 categories on day one will burn you out. Stick to three or four main problem areas—like groceries, gas, dining out, and fun. Expand later once the habit sticks.

What happens if I have an emergency and my envelope is empty?

Keep a separate, fully funded digital emergency savings account at your bank. Paper money is for daily variable spending. If your car breaks down, use your debit card to tap into your digital emergency fund.

{kind=link}