Buying a home is probably the biggest financial move you will ever make. Unless you have a mountain of cash sitting in a bank account, you are going to need some help to pay for it. This is where a mortgage comes in. For many people, the idea of a thirty-year debt feels heavy and a bit scary.

The industry uses a lot of big words that make the process seem more complicated than it actually is. Once you peel back the layers of jargon, you will find a simple system of borrowing and repaying.

If you are curious about how home loans work, you have come to the right place. We are going to look at everything from the very first application to the final payment you make decades from now. This guide is designed to give you a clear map so you don’t feel lost when talking to banks or real estate agents. By the time you finish reading, you will understand the math behind your monthly payment and how to get the best deal possible for your future home.

What Exactly is a Mortgage?

A mortgage is essentially a legal agreement between you and a bank or a lender. They give you the money to buy a house, and you agree to pay it back over a set amount of time. What makes it different from a personal loan is the collateral. Your home is the guarantee that you will pay the money back. If you stop making payments for a long time, the lender has the legal right to take the home and sell it to get their money back.

The Difference Between a Loan and a Mortgage

While people use the terms interchangeably, there is a technical difference you should know. A loan is any sum of money borrowed that must be repaid with interest. A mortgage is a specific type of loan used for real estate where the property itself secures the debt. When you sign a mortgage, you are giving the lender a lien on the property. This stays in place until the very last dollar is paid off, at which point the home is officially yours.

Key Components: PITI Explained

Your monthly bill is not just one simple number. It is actually a combination of four different costs grouped together, known as PITI. Principal is the actual money you borrowed. Interest is the fee the lender charges you for that money. Taxes go to your local government for things like schools and roads. Insurance protects your home from damage. Most lenders collect all four parts and handle the tax and insurance payments for you so you don’t have to worry about them separately.

|

Component |

What it Covers |

Who Receives the Money |

|

Principal |

The original loan balance |

The mortgage lender |

|

Interest |

The cost of borrowing |

The mortgage lender |

|

Taxes |

Local property assessments |

Local government |

|

Insurance |

Hazard and theft protection |

Insurance company |

How Home Loans Work: A Step-by-Step Breakdown?

To truly master the home-buying process, you have to understand how home loans work from the inside out. It starts with the money you bring to the table and ends with a long-term repayment plan. Lenders look at your financial life to see how much risk you represent. They want to be sure that you can handle the monthly commitment without falling behind on other bills or daily life expenses.

The Role of the Down Payment

The down payment is the cash you pay upfront to show the lender you are invested in the property. In the past, people thought they needed twenty percent of the home’s price to get a loan. Today, that is not true anymore as many programs let you buy with much less. However, a bigger down payment usually means you get a better interest rate and a smaller monthly bill. It also gives you instant equity, which means you own more of the house right away.

Interest Rates and How They Are Determined

Interest rates are the most important part of the cost because they determine how much you pay over thirty years. These rates go up and down based on the national economy and the decisions of the central bank. On a personal level, your score and your income determine the specific rate a bank offers you. A high credit score usually unlocks the lowest rates because the bank trusts you more. Even a small difference in your rate can save you thousands of dollars over the life of the loan.

Amortization: Why Early Payments Go to Interest

Amortization is a fancy word for the schedule of your payments. When you first start paying your mortgage, most of your money goes toward the interest rather than the actual loan balance. This is because the interest is calculated based on the large amount you still owe. As the years go by and your balance gets smaller, the interest charge drops, and more of your money goes toward the principal. By the end of the loan, almost your entire payment goes toward finishing off the debt.

|

Year Range |

Principal Impact |

Interest Impact |

Total Equity Growth |

|

Years 1-10 |

Very Low |

Very High |

Slow |

|

Years 11-20 |

Moderate |

Moderate |

Steady |

|

Years 21-30 |

Very High |

Very Low |

Rapid |

Common Types of Home Loans

There is no single loan that fits every person. Depending on your job, your credit, and your location, you might choose one over another. Understanding how home loans work involves knowing which bucket you fall into before you start shopping. Some loans are better for people who want to stay in a home forever, while others are great for people who might move in a few years to a bigger house.

Fixed-Rate Mortgages

The fixed-rate mortgage is the most popular choice because it is predictable. Your interest rate stays the exact same for the whole time you have the loan. This means your monthly principal and interest payment will never change, even if the economy goes crazy. Most people choose a thirty-year fixed loan because it offers the lowest monthly payment. If you can afford more each month, a fifteen-year fixed loan will help you pay off the house much faster and save a lot on interest.

Adjustable-Rate Mortgages (ARMs)

An adjustable-rate mortgage starts with a lower interest rate than a fixed loan, but it doesn’t stay that way. After a few years, usually five or seven, the rate begins to change based on the market. If rates go up, your monthly payment will go up too. These are risky if you plan to stay in the home for a long time. However, if you know you will sell the house or refinance before the rate changes, an ARM can save you a lot of money in those early years.

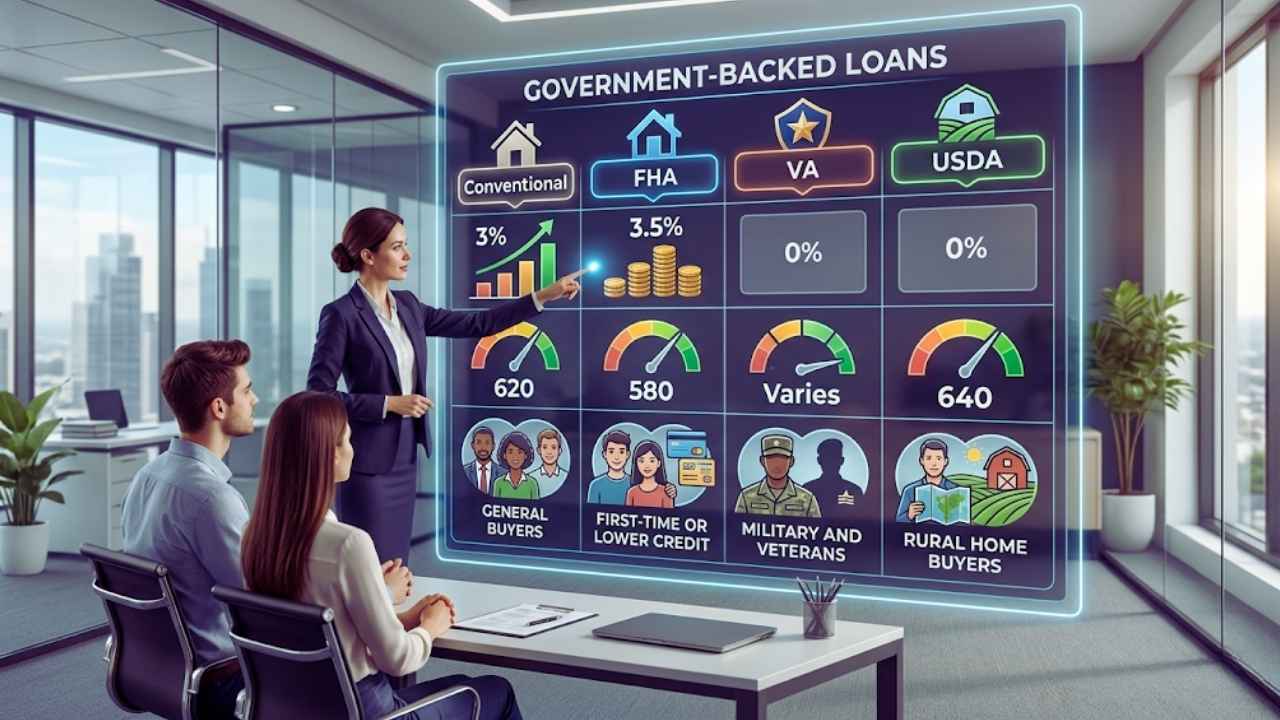

Government-Backed Loans (FHA, VA, USDA)

The government offers special programs to help people who might struggle with traditional bank requirements. FHA loans are great for first-time buyers with lower credit scores. VA loans are an amazing benefit for veterans and active military members because they require no down payment at all. USDA loans help people buy homes in rural areas with zero money down. These programs make it possible for almost anyone with a steady job to become a homeowner if they find the right fit.

|

Loan Program |

Minimum Down Payment |

Minimum Credit Score |

Target Audience |

|

Conventional |

3% |

620 |

General buyers |

|

FHA |

3.5% |

580 |

First-time or lower credit |

|

VA |

0% |

Varies |

Military and Veterans |

|

USDA |

0% |

640 |

Rural home buyers |

The Mortgage Application Process

Getting a mortgage is like a deep background check for your money. You have to prove exactly how much you earn and how much you spend every single month. Lenders are very careful because they are giving you a huge amount of capital. They want to see that you have a history of paying your bills on time and that you aren’t already drowning in other debts like car loans or high credit card balances.

Getting Pre-Approved vs. Pre-Qualified

A pre-qualification is a quick estimate based on what you tell the bank. It doesn’t mean much in the real world of house hunting. A pre-approval is much more serious because the bank actually checks your credit and looks at your tax returns. Most sellers will not even let you look at their house unless you have a pre-approval letter. It proves to everyone involved that you have the financial power to actually buy the home if you make an offer.

Credit Scores and Debt-to-Income Ratio

Your credit score is the first thing a lender sees. It acts like a grade for your financial history. If your score is low, you might have to pay a higher interest rate or put more money down. Lenders also look at your debt-to-income ratio. They add up all your monthly bills and compare them to your monthly income. If your bills take up too much of your paycheck, the bank might worry that a new mortgage payment will be too much for you to handle.

Underwriting: Behind the Scenes

Underwriting is the final stage where a professional at the bank double-checks everything in your file. They make sure the house is worth what you are paying for it by ordering an appraisal. They also verify that you still have your job and that no new debts have appeared on your credit report. This is the most stressful part of the process for most buyers. It is very important not to buy a new car or make any large purchases until after you have the keys to your new home.

|

Stage |

Action Needed |

Typical Timeframe |

|

Pre-Approval |

Verify income and credit |

1 to 3 days |

|

Processing |

Collect all bank docs |

1 to 2 weeks |

|

Underwriting |

Final risk assessment |

3 to 7 days |

|

Closing |

Sign final papers |

1 day |

Understanding the True Cost of Ownership

Knowing how home loans work means looking past the purchase price of the house. There are many hidden costs that can surprise you if you aren’t prepared for them. Some of these are one-time fees paid at the beginning, while others are ongoing costs that will be part of your budget for years. Being a homeowner is about more than just the mortgage; it is about managing all the smaller expenses that come with owning property.

Closing Costs: The Fees You Forget

Closing costs are the fees you pay to the bank, the government, and other professionals to finalize the sale. These usually cost between two and five percent of the total loan amount. They cover things like the home appraisal, the title search, and the work done by attorneys or escrow officers. You have to pay this money in cash on the day you sign for the house. It is a good idea to save up for these costs separately from your down payment so you don’t run out of money at the end.

Private Mortgage Insurance (PMI)

If you put down less than twenty percent on a conventional loan, you will have to pay for private mortgage insurance. This is an extra fee added to your monthly bill that protects the lender if you stop paying. It does not protect you, but it is the price you pay for getting a home with a small down payment. Once you have paid off enough of the loan to reach twenty percent equity, you can usually ask the lender to remove this fee and lower your monthly bill.

Escrow Accounts and Property Taxes

An escrow account is a special bucket of money managed by your lender. Each month, a portion of your payment goes into this account to pay for your property taxes and insurance. This is a great system because it keeps you from getting hit with a massive tax bill once a year. However, you should know that if your taxes or insurance rates go up, your monthly mortgage payment will go up too. This is the most common reason why a fixed-rate mortgage payment might change slightly over time.

|

Cost Category |

Estimated Amount |

How it is Paid |

|

Closing Costs |

2% to 5% of price |

Cash at signing |

|

PMI |

0.5% to 1% of loan |

Monthly in bill |

|

Home Appraisal |

$400 to $700 |

Usually upfront |

|

Title Insurance |

$500 to $1,500 |

Cash at signing |

How to Choose the Right Mortgage for You?

Picking a mortgage is a personal decision that depends on your future plans. If you plan to live in the house for thirty years and raise a family, a fixed-rate loan is almost always the best move. It gives you peace of mind because you know your costs will stay the same. If you are a young professional who expects to move for work in five years, an adjustable-rate mortgage might save you a lot of money in the short term while the rate is low.

You also need to think about how much of your savings you want to use. Putting all your money into a down payment might leave you “house poor,” which means you have a great home but no cash left for repairs or furniture. Sometimes it is better to take a slightly higher monthly payment so you can keep an emergency fund in the bank. Talking to a few different lenders is the best way to see all your options and find a balance between a low rate and a comfortable monthly bill.

|

Goal |

Best Loan Choice |

Why |

|

Long-term stability |

30-Year Fixed |

Payments never change |

|

Lowest interest cost |

15-Year Fixed |

Faster payoff, lower rate |

|

Short-term savings |

5/1 ARM |

Lower initial monthly cost |

|

Low cash upfront |

FHA or VA |

Low or no down payment |

Final Thoughts

When you finally understand how home loans work, the process of buying a house feels like a goal rather than a mystery. It is all about finding a balance between what you can afford today and what you want for your future. A mortgage is a tool that helps you build wealth over time as your home increases in value and your debt slowly disappears. Take your time to fix your credit, save up as much as you can, and always ask questions if something doesn’t make sense.

Keep in mind that the lender is your partner in this transaction, but you are the one in charge of your budget. Don’t let anyone pressure you into a loan that feels too big for your income. By doing your homework and following the steps in this guide, you can walk into your new home knowing you made a smart financial choice. Homeownership is a marathon, not a sprint, and understanding the math behind your mortgage is the best way to cross the finish line successfully.

Frequently Asked Questions (FAQs) About How Mortgages Work

What is a mortgage servicer?

A mortgage servicer is the company that handles the daily management of your loan. They collect your monthly payments, manage your escrow account, and send out your year-end tax forms. Sometimes the bank that gave you the loan is the servicer, but often they sell the servicing rights to another company. This doesn’t change your loan terms at all.

Can I skip a mortgage payment if I have an emergency?

Generally, no. Skipping a payment without permission will hurt your credit score and lead to late fees. However, if you have a major life event like a job loss or a natural disaster, you can call your lender and ask for “forbearance.” This is a temporary agreement to pause or lower payments while you get back on your feet.

What does it mean to “points” on a mortgage?

Buying points means you pay extra money upfront at closing to get a lower interest rate for the life of the loan. One point usually costs one percent of the loan amount. This is a good idea if you plan to stay in the home for a long time, as the monthly savings will eventually outweigh the upfront cost.

How does a cash-out refinance work?

A cash-out refinance is when you replace your current mortgage with a new, larger one. You get to keep the difference in cash. People often do this to pay for home renovations or to consolidate high-interest debt. You can only do this if your home has increased in value and you have enough equity built up.

Is homeowner’s insurance the same as mortgage insurance?

No, they are different. Homeowner’s insurance protects you and the lender from physical damage to the house like fires or storms. Mortgage insurance (PMI) only protects the lender if you stop making your payments. You will almost always need homeowner’s insurance, but you only need PMI if your down payment is small.

{kind=link}