When you start building your retirement portfolio, you quickly hit a fork in the road. You have cash ready to invest, but you need to know where to put it. This brings us to a massive debate in the finance world: ETF vs Mutual Fund. Both choices pool your money with other investors to buy a basket of stocks or bonds. They give you instant diversification and lower your risk compared to picking individual companies.

But under the hood, they operate in completely different ways. I want to break down exactly how these two vehicles work so you can make a smart, informed choice for your money. Whether you care about tax efficiency, trading flexibility, or rock-bottom fees, understanding the mechanics of each fund type will save you thousands of dollars over the next few decades. Let’s look at what makes each option unique and how they fit into a serious wealth-building strategy.

Understanding the Basics of Investment Funds

Building sustainable wealth requires you to understand where your money goes before you click the buy button. Investment funds act as a collective bucket where thousands of everyday people pool their capital together. This combined financial power allows a single investor to own a tiny slice of hundreds of different companies simultaneously.

Instead of risking everything on one or two corporate stocks, you spread your risk across the entire marketplace. This method shields your hard-earned savings from the sudden collapse of an individual business. For decades, these vehicles have served as the fundamental building blocks for retirement accounts, pension plans, and personal brokerage accounts worldwide.

|

Fund Category |

Structural Setup |

Operational Model |

Primary Asset Base |

|

Exchange-Traded Fund |

Open market security |

Traded continuously throughout the day |

Stocks, bonds, or commodities |

|

Mutual Fund |

Direct issuer contract |

Processed once daily after market close |

Diversified portfolio mixes |

What Is an Exchange-Traded Fund?

An exchange-traded fund functions as an investment basket that lives and trades openly on public stock exchanges. You buy and sell shares of this basket through a standard brokerage account exactly like you would buy a share of any major tech stock. Because it trades publicly, the price of the fund moves up and down every second the market remains open. This setup grants you extreme flexibility to enter or exit a position at a specific moment during the regular trading day.

What Is a Mutual Fund?

A mutual fund handles your capital through a direct relationship with the financial institution managing the asset. Instead of matching with an independent buyer or seller on an open stock exchange, your transactions go through the fund issuer itself. The processing happens in one large batch after the final closing bell rings on Wall Street. This means every single person buying into the fund on a specific day receives the exact same transaction price, regardless of what time they submitted their paperwork.

ETF vs Mutual Fund: The Core Differences

Choosing between an ETF vs Mutual Fund requires you to weigh how much control you want over your daily transactions. The fundamental plumbing of these two choices creates completely different user experiences regarding liquidity and accessibility. Some investors prefer the fast, real-time nature of exchange trades, while others enjoy the slower rhythm of traditional banking transactions.

These structural differences also dictate how much starting capital you need to get your portfolio off the ground. By examining the mechanics of trading, minimum inputs, and operational management styles, you can easily map out which vehicle aligns with your personal workflow.

|

Comparison Area |

Exchange-Traded Option |

Mutual Option |

|

Order Execution |

Instant market execution |

Delayed end-of-day batching |

|

Price Discovery |

Fluctuation based on live supply |

Fixed net asset value calculation |

|

Account Minimums |

Single share entry barrier |

Flat dollar entry thresholds |

Trading Mechanics and Pricing

The open market setup gives you live pricing updates every single second. If a major political event happens at noon, you can react instantly by buying or selling your shares. You can also use specific order types like limit orders to ensure you never pay more than a target price. Traditional mutual setups completely bypass this live environment. Your order sits in a queue until the market closes down for the evening, meaning you cannot time your entry to avoid intraday volatility.

Minimum Investment Requirements

The amount of money sitting in your checking account will often choose your investment path for you. Traditional pooled funds routinely demand a high minimum financial commitment just to open the door. You might need a lump sum of two thousand dollars or more to buy into a premium fund class. Exchange-traded options eliminate this wall entirely because the minimum entry requirement is simply the cost of one single share. If a share costs fifty dollars, then fifty dollars is all you need to start investing.

Management Styles: Active vs Passive

The people managing the internal portfolio follow two distinct philosophies. Active management relies on a highly paid team of market experts who spend their days researching balance sheets to find undervalued companies. They try to beat the general market returns through clever timing and deep analysis. Passive management ignores this competitive approach entirely by using automated software to mimic an existing market index. The passive system simply holds every stock in the index, completely removing human bias and guesswork from the equation.

Cost Comparison: Expense Ratios and Fees

High operational fees act as an invisible anchor on your long-term financial growth. When you look at an ETF vs Mutual Fund matchup, the total cost of ownership will heavily influence your final net returns. Financial institutions do not manage your money out of charity, so they deduct their operational costs directly from your account balances.

Over a multi-decade investing career, a seemingly tiny difference of one percent in annual fees can compound into a massive loss of capital. You must audit every potential layer of fees, including management percentages, transaction costs, and hidden sales penalties, before committing your capital.

|

Fee Type |

Exchange-Traded Setup |

Mutual Setup |

|

Management Cost |

Minimal automated pricing |

Premium human analysis pricing |

|

Purchase Commissions |

Zero on most modern platforms |

Frequent sales loads from advisors |

|

Structural Overhead |

Extremely streamlined |

High administrative customer service |

Unpacking Expense Ratios

The expense ratio represents the percentage of your total investment that the fund company skims off each year to cover its internal bills. Passive exchange-traded options are famously cheap because they require very little human labor to maintain. You can easily find large index products that charge a tiny expense ratio of just 0.03 percent annually. Many actively managed alternatives charge ten or twenty times that amount because they have to fund expensive corporate offices and executive salaries.

Hidden Fees and Trading Commissions

Sleazy financial practices often hide extra costs deep inside the thick pages of a fund prospectus. Traditional funds are notorious for charging sales loads, which are flat commissions paid directly to the broker who sold you the product. A front-end load might instantly steal five percent of your cash before it ever gets invested into the market. Exchange-traded alternatives completely avoid these sales loads, though you must stay aware of the bid-ask spread on the open market, which acts as a tiny transaction friction.

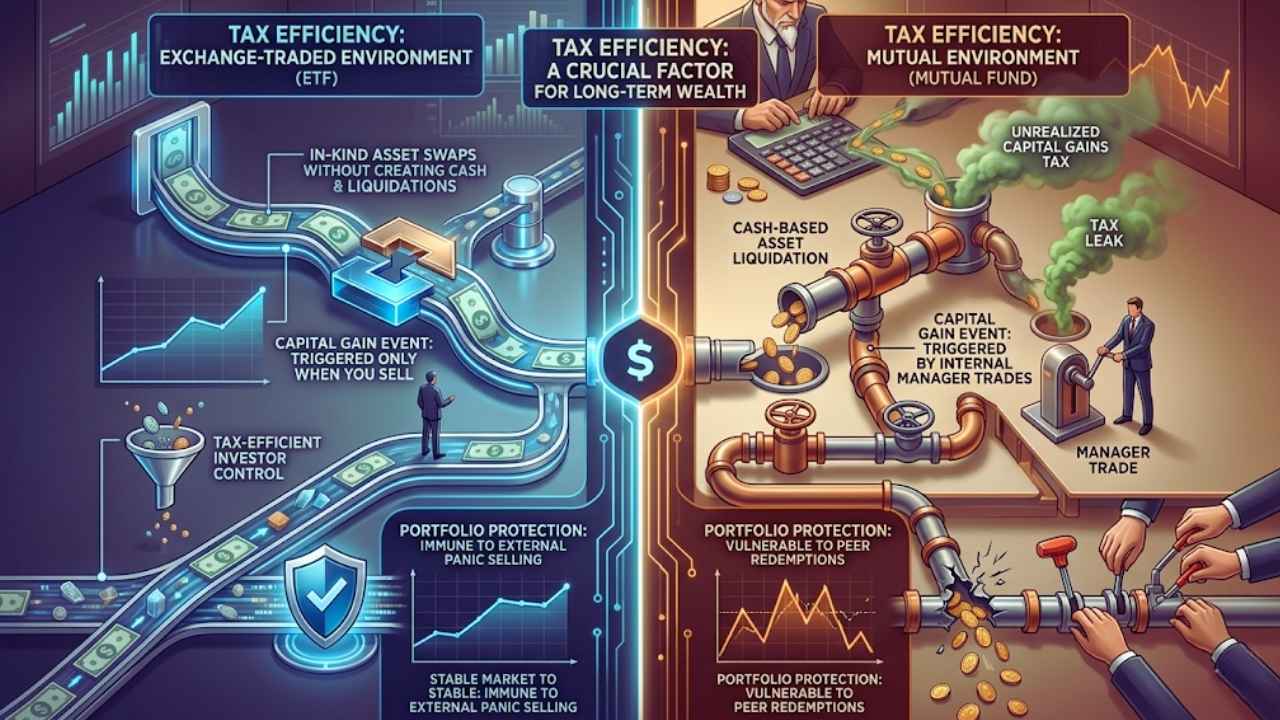

Tax Efficiency: A Crucial Factor for Long-Term Wealth

Minimizing your annual tax bill is just as important as choosing the right stocks for your portfolio. The debate of ETF vs Mutual Fund takes a drastic turn when you look at how the Internal Revenue Service treats each vehicle inside a standard taxable brokerage account.

Every time an investment fund shifts its internal holdings, it creates a potential tax event that can trigger a bill for the individual investor. If you are not careful, you can end up paying taxes on profits you never personally realized. Understanding the underlying transaction plumbing will keep your money growing instead of leaking away to Uncle Sam.

|

Tax Matrix |

Exchange-Traded Environment |

Mutual Environment |

|

Capital Gain Event |

Triggered only when you sell |

Triggered by internal manager trades |

|

Internal Settlement |

In-kind asset swaps |

Cash-based asset liquidation |

|

Portfolio Protection |

Immune to external panic selling |

Vulnerable to peer redemptions |

Capital Gains Distributions in Mutual Funds

Traditional pooled structures suffer from a massive structural tax flaw that harms long-term buy-and-hold investors. When a manager needs to rebalance the portfolio or raise cash to pay off departing investors, they must sell internal stocks on the open market. If those stocks have grown in value, the sale triggers a taxable capital gain. By federal law, the fund must distribute these capital gains to all current shareholders at the end of the year. This means you will owe annual income taxes on those gains, even if you never sold a single share yourself.

Why ETFs Often Hold a Tax Advantage?

Exchange-traded products bypass this unfair tax trap by utilizing an authorized participant system to execute in-kind creations and redemptions. When big institutional players want to move large chunks of money out of the fund, the manager does not sell stocks for cash. Instead, they hand over the actual physical shares of stock directly to the institutional player in an even swap. Because the fund never liquidates the stocks for cash, no official capital gain occurs under current tax laws, perfectly protecting everyday retail investors from surprise tax bills.

Performance and Long-Term Wealth Generation

The ultimate metric for any investment strategy is the final balance of your portfolio when you reach retirement age. Evaluating the performance of an ETF vs Mutual Fund requires you to understand how small structural frictions impact the mathematical reality of compounding interest over thirty or forty years.

A fund that tracks the market perfectly while keeping its internal expenses low will almost always outperform a fund that takes big risks while charging high fees. You need to look past flashy short-term marketing campaigns and focus on the cold historical data surrounding long-term market tracking.

|

Performance Element |

Passive Exchange Basket |

Active Managed Group |

|

Long-Term Objective |

Match the exact benchmark return |

Attempt to beat the benchmark return |

|

Internal Cash Reserves |

Zero cash drag maintained |

High cash buffer held for withdrawals |

|

Historical Success Rate |

High consistency over decades |

Low consistency due to human error |

The Power of Compounding over Decades

Compounding interest acts as the primary engine for wealth generation by generating returns on top of your previous returns. To get the absolute maximum power out of this mathematical compounding engine, you must remove as much operational friction as possible. A low-cost, tax-shielded index option allows your money to remain fully invested without regular interruptions from management fees or tax deductions. Over a multi-decade career, this clean compounding path can easily result in a six-figure difference in your final net worth.

Tracking Error and Market Returns

Passive funds aim to mirror the performance of a specific index as closely as humanly possible, and any deviation from that target is called a tracking error. Traditional funds often struggle with tracking errors because they suffer from cash drag. They must hold a substantial pile of uninvested cash in their accounts to pay out investors who request withdrawals on any given day. Exchange-traded options do not worry about daily cash redemptions, allowing them to remain completely invested in the market at all times to capture every bit of growth.

How to Choose the Right Fund for Your Portfolio?

You do not have to pick one single option and abandon the other for the rest of your life. The most successful wealth builders understand that an ETF vs Mutual Fund choice depends entirely on the specific account you are using and your personal style of money management.

Different financial goals require different financial tools. By analyzing your available workplace benefits, your tax status, and your technological preferences, you can easily build a blended portfolio that captures the absolute best features of both worlds.

|

Investor Scenario |

Primary Recommendation |

Strategic Reasoning |

|

Standard Taxable Brokerage |

Exchange-Traded Fund |

Maximum tax sheltering capabilities |

|

Workplace 401(k) Plan |

Mutual Fund |

Default option with direct payroll links |

|

Low Capital Weekly Savings |

Exchange-Traded Fund |

Low share prices with fractional buying |

When to Choose a Mutual Fund?

The traditional direct fund model makes perfect sense if your primary goal is complete automation. If you want a system that takes two hundred dollars out of your paycheck every single week and buys investments without you ever opening an app, this is your best option. They are also the standard default choice inside employer-sponsored 401(k) plans, where tax efficiency is not an issue because the account is already shielded from annual taxes by the government.

When to Choose an Exchange-Traded Fund?

You should favor the exchange-traded route whenever you are investing money inside a standard taxable brokerage account. The structural protection against annual capital gains distributions will save you a massive amount of money over time. They are also the undisputed champions for younger investors or people working with a small amount of seed capital. The ability to buy into major global indexes for the price of a single fractional share removes the elitist financial barriers that used to keep everyday working people out of the stock market.

The Future of Investing: Market Trends

The global investment landscape is moving rapidly away from old-school financial models toward highly streamlined digital alternatives. Every year, billions of dollars leave expensive, actively managed legacy accounts and pour directly into low-cost, transparent exchange options.

Retail investors are becoming highly educated about the destructive nature of hidden fees, and they are voting with their wallets. This massive shift in consumer behavior is forcing the largest financial institutions on Wall Street to completely rethink how they design and distribute their products to the public.

|

Market Shift |

Historical Standard |

Future Projection |

|

Capital Allocation |

High-cost active management |

Low-cost passive automation |

|

Product Structure |

Opaque end-of-day pricing |

Transparent real-time exchange access |

|

Access Barriers |

Wealthy client priority tiers |

Complete democratic retail parity |

Major asset management companies are now taking their most successful traditional funds and converting them directly into exchange-traded products to prevent their client base from leaving.

At the same time, the rise of algorithmic robo-advisors and zero-commission trading apps has made it incredibly easy for regular people to manage complex global portfolios from their smartphones. As these automated technologies continue to mature, the historic administrative advantages of traditional corporate funds are dissolving, making the exchange-traded model the absolute default choice for the next generation of savers.

Takeaways

Winning the game of long-term financial freedom does not require you to predict the future or take wild gambles on trendy investments. Success comes down to mastering the basic variables that you can actually control: fees, taxes, and asset diversification. When you evaluate an ETF vs Mutual Fund setup, remember that both options can act as highly effective vehicles to carry you toward your retirement goals. The key is to match the structural strengths of each tool to the specific tax status of your accounts.

Use the traditional automated fund setup to create a set-it-and-forget-it system inside your workplace retirement plans where taxes cannot hurt you. Utilize the sleek, tax-efficient nature of exchange-traded products to maximize the growth of your taxable brokerage accounts. By eliminating unnecessary fee drag and staying disciplined through market cycles, you ensure that the mathematical reality of compound interest works entirely in your favor.

Frequently Asked Questions (FAQs) About ETF vs Mutual Fund

Why do some mutual funds require such high minimum investments?

Managing individual customer accounts requires a significant amount of administrative paperwork, data tracking, and customer service staff. By setting a high entry barrier of a few thousand dollars, traditional management firms ensure that each account holds enough capital to generate profitable fee revenue to cover their operational corporate overhead.

Do exchange-traded funds pay dividends?

Yes, they pass along all dividends paid by the underlying stocks inside their basket. If you own an index fund that holds hundreds of dividend-paying corporations, the fund collects those payments throughout the quarter, aggregates them, and drops the cash directly into your brokerage account on a regular schedule.

Can I lose more money than I invested in these funds?

No, your total financial liability is strictly limited to the exact amount of cash you personally deposit into the fund. Unlike advanced trading strategies that involve borrowing money on margin or shorting stocks, standard long-term index funds can never drop below a value of zero, meaning you will never owe money to a broker.

Are there actively managed exchange-traded funds?

Yes, the financial industry has launched thousands of active variations over the past few years to satisfy demand for real-time trading options. These products feature an individual portfolio manager trying to beat the market while using the exchange-traded wrapper, though they usually carry much higher annual expense ratios than standard passive index options.

How does the bid-ask spread affect my returns?

The bid-ask spread operates as a tiny, invisible transaction cost every time you buy or sell a share on the open live stock market. For large, highly popular index funds, this price gap is usually just a single penny per share, making it completely irrelevant for long-term buy-and-hold investors who plan to hold the asset for decades.

What happens if the company managing my fund goes bankrupt?

Your investment capital remains completely safe because your assets are legally separated from the corporate balance sheet of the management company. The actual stocks and bonds are held by an independent third-party custodian bank, so if the management firm collapses, a new firm takes over or the assets are safely sold to return cash to shareholders.

You can only execute a direct conversion if the fund family explicitly offers an exchange-traded share class for that specific asset and your brokerage platform supports the internal paperwork. If you have to sell the traditional shares on the open market to buy the alternative, you will trigger a taxable capital gains event inside a standard brokerage account.

{kind=link}