We all know the frustrating monthly drill. Payday hits, and you immediately start paying everyone else. The landlord gets a massive cut right off the top. The electric company demands their share. The grocery store takes whatever is left over.

By the end of the month, you stare at your checking account, hoping to toss a few bucks into savings. Sadly, the money is already gone. It is a classic financial trap that keeps people broke. You pay every single external business before you ever pay yourself. You end up relying on the leftovers, and let us be completely honest—there are rarely any leftovers.

Flip that script, and your entire financial life changes. Enter pay yourself first budgeting. It means prioritizing your own financial future before a single dollar leaves your account for bills or entertainment. You take willpower out of the equation completely and put your wealth building on total autopilot. Stop waiting for scraps at the end of the month. Guarantee your savings upfront.

How Pay-Yourself-First Budgeting Fixes the Money Trap?

The concept is dead simple but completely transformative. The exact second your paycheck clears, a specific amount instantly moves into your savings or investment accounts. You do this before you pay rent, buy food, or hit the bars with friends. George S. Clason nailed this idea almost a century ago in his book The Richest Man in Babylon. He argued that a piece of everything you earn actually belongs to you. Think about it realistically. If you make $4,000 a month and spend $4,000 a month, you are just a middleman.

You work 40 hours a week just to hand your money to your landlord and local restaurants. Take your cut first and force yourself to live on the rest. If you automatically stash 15 percent of your pay, your lifestyle naturally shrinks to fit the remaining 85 percent. You completely bypass lifestyle creep. Forget tracking every single coffee purchase. When you secure your savings right off the top, the rest of your cash becomes entirely guilt-free spending money.

|

Feature |

Traditional Budgeting |

The Pay Yourself First Method |

|

First Move |

Pay bills and living expenses. |

Transfer money to savings and investments. |

|

Second Move |

Spend on wants and lifestyle. |

Pay bills and living expenses. |

|

Final Move |

Save whatever is left over. |

Spend on wants and lifestyle. |

|

Mental State |

High stress, hoping to have money left. |

Guilt-free spending on the remainder. |

The Core Mechanics Behind the Strategy

Setting this up takes about one hour of your weekend. It pays off massively for the rest of your life. The magic ingredient making this whole system work is absolute automation. If you rely on logging into your bank app every two weeks to transfer money manually, you will eventually fail. You will have a stressful day at work. Your car will need new brakes. You will just forget to log in. To make pay-yourself-first budgeting actually work, you must remove yourself from the active process.

Make the money vanish before you can even think about spending it. Grab your target number first. If you take home $5,000 a month and want to save 20 percent, your target is $1,000. Talk to your HR department to split your direct deposit. Send a fixed percentage directly to your savings, and route the rest to your checking account. This is the absolute best method because the money never even touches your spending account.

|

Setup Step |

Action Required |

The Expected Result |

|

1. Set Target |

Pick a percentage of your take-home pay. |

Gives you a hard financial goal to hit. |

|

2. Separate Cash |

Keep savings at a different bank than checking. |

Creates a massive barrier against impulse buys. |

|

3. Automate Flow |

Use HR direct deposit splits or auto-transfers. |

Kills the absolute need for daily discipline. |

|

4. Adjust Life |

Live strictly off the remaining checking balance. |

Forces natural frugality and stops overspending. |

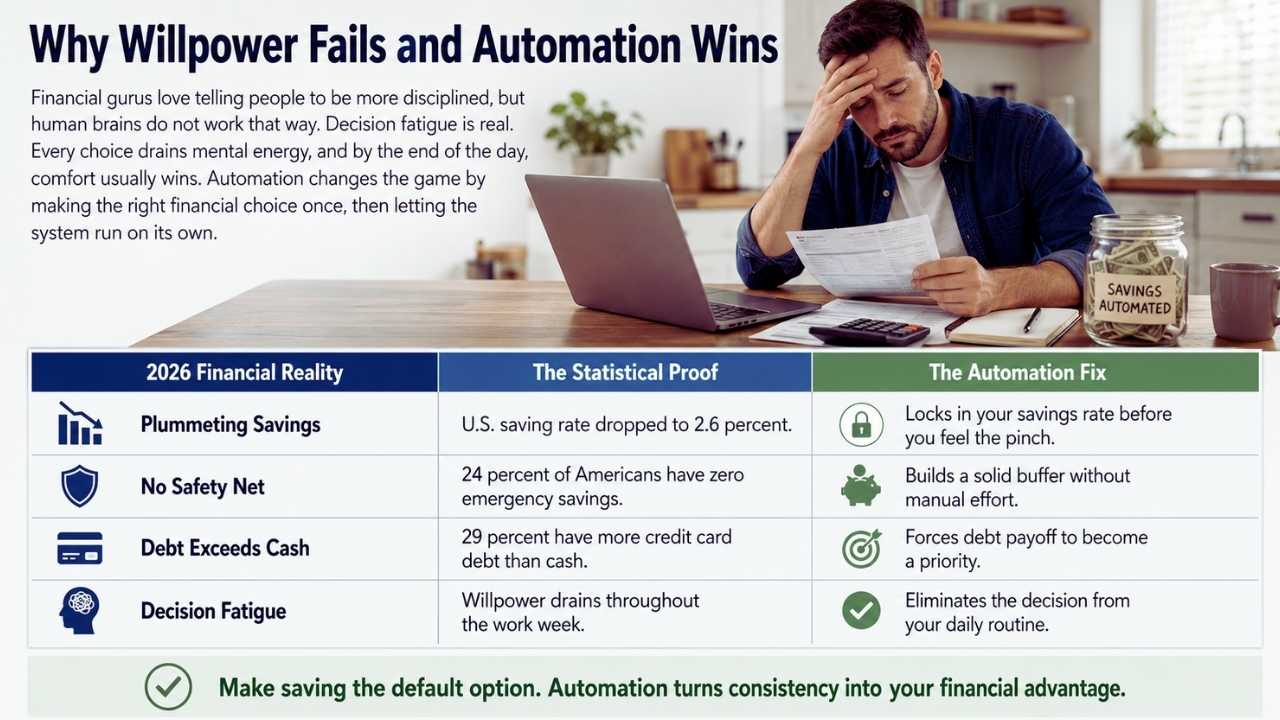

Why Willpower Fails and Automation Wins Today?

Financial gurus love yelling at us to be more disciplined. They want you to cut out every tiny joy to get ahead. Human brains simply do not work that way. Decision fatigue is a very real psychological barrier. Every choice you make throughout the day drains your mental battery. By dinner time, you are completely exhausted. Your brain naturally seeks comfort. You end up ordering an expensive pizza instead of cooking the pasta sitting right in your pantry.

Relying on sheer willpower is a losing battle because it eventually runs out. When you automate your cash flow, you only make the right financial choice once. You set it up on a Sunday, and it runs flawlessly for years. By early 2026, the United States saving rate dropped to a dismal 2.6 percent. Make laziness your financial superpower. Make saving the default option because changing it requires too much annoying effort.

|

2026 Financial Reality |

The Statistical Proof |

The Automation Fix |

|

Plummeting Savings |

U.S. saving rate dropped to 2.6 percent. |

Locks in your savings rate before you feel the pinch. |

|

No Safety Net |

24 percent of Americans have zero emergency savings. |

Builds a solid buffer without manual effort. |

|

Debt Exceeds Cash |

29 percent have more credit card debt than cash. |

Forces debt payoff to become priority number one. |

|

Decision Fatigue |

Willpower heavily drains throughout the work week. |

Eliminates the decision entirely from your daily routine. |

Picking Your Target Percentage

Do not get stuck obsessing over the perfect mathematical percentage. Pulling too much money upfront will cause you to bounce checks. You will then have to transfer money back from your savings account. You will feel like a total failure and probably quit the system entirely. The standard 50/30/20 rule gives you a solid baseline to start. Put 50 percent toward your needs, 30 percent toward wants, and 20 percent toward savings and debt.

If you cannot hit 20 percent right now, do not panic. The habit matters way more than the dollar amount on day one. Start with just 1 percent of your check. If you clear $3,000 a month, auto-transfer just $30. You will not even notice that cash is missing. Bump it up slowly over the next few months. Whenever you score a raise, send half of that new money straight to your investments.

|

Savings Rate |

Who It Is Best For |

Long-Term Impact on Wealth |

|

1% to 5% |

Beginners living strictly paycheck to paycheck. |

Builds the habit without breaking your budget. |

|

10% to 15% |

Average earners looking for standard retirement. |

Keeps you perfectly on track to retire on time. |

|

20% to 30% |

Aggressive savers wanting early financial security. |

Slashes the total years you have to spend working. |

|

40% or More |

Financial Independence and Retire Early chasers. |

Builds massive wealth and buys total time freedom. |

Where Does the Money Actually Go?

Yanking the cash out of your checking account is only step one. Step two requires putting that money to work. Leaving it in a basic checking account earning zero interest just lets inflation eat it alive. You need a specific waterfall strategy for your automated transfers. First, build a sturdy safety net. Aim for one month of bare-bones living expenses, then push for three to six months.

Stash this cash in a high-yield savings account. In mid-2026, top online banks still pay around 4.10 percent APY. Let your money make more money while you sleep. Second, grab the free money your company offers. If your boss offers a 401(k) match, take every single penny of it. Third, aggressively crush any toxic credit card debt. Finally, funnel the rest into low-cost index funds inside a Roth IRA.

Read Also: Best Personal Finance Apps in 2026: Honest Comparison

|

Priority Level |

Account Type Destination |

2026 Gameplan and Purpose |

|

Priority 1 |

Emergency Fund High Yield Savings |

Chase yields around 4.10 percent APY for cash liquidity. |

|

Priority 2 |

Employer 401(k) Retirement Match |

Max out free company money up to federal limits. |

|

Priority 3 |

High-Interest Credit Card Debt |

Kill credit card balances to stop daily wealth erosion. |

|

Priority 4 |

Roth IRA or Brokerage Account |

Buy low-cost index funds for long-term compound growth. |

Handling Variable Incomes and the Gig Economy

Freelancers and commissioned sales reps always push back hard on this concept. You might be thinking that you have no idea what you will make next week. Rigid dollar amounts will absolutely cause overdrafts if your income jumps around constantly. The easiest fix involves using percentages and a dedicated holding account. Funnel all your client payments and side-hustle cash into one central checking account. Do not spend a single dime directly from this specific account.

On the first day of every month, look at your total balance. Act exactly like your own payroll clerk. Send 20 percent straight to your savings account. Send a flat, realistic salary amount to your personal checking account for living expenses. Leave the remaining cash as a buffer for the inevitable slow months. This system completely kills the stressful feast-and-famine cycle.

|

Income Type |

Strategy Tweak Required |

The Best Tool to Use |

|

Steady W2 Salary |

Automate fixed dollars based on net pay. |

Human Resources direct deposit portal. |

|

Commission-Based |

Auto-transfer percentages when deals close. |

Smart-bank rules and automatic triggers. |

|

Freelance and Gig |

Route income to a holding account, pay a salary. |

Multiple separate checking accounts. |

|

Side Hustler |

Send 100 percent of side-income to investments. |

Separate business account linked to a savings account. |

Beating Inflation by Trimming the Fat

Saving a massive chunk of your income sounds great until your grocery bill doubles. By early 2026, over half of all Americans are living strictly paycheck to paycheck. Total household debt just shattered records, hitting an eye-watering $18.8 trillion. Things are incredibly tight for almost everyone right now. If you truly lack enough income to survive, a budgeting trick will not save you.

However, most middle-class earners can find a few financial leaks to plug. You need to ruthlessly audit your monthly life. Cancel the streaming service you have not watched in three months. Call your car insurance company today and demand a better rate. When you cut a $50 bill, increase your automatic savings transfer by exactly $50 that same afternoon. Capture that cash before it gets absorbed by random impulse buys.

|

The Monthly Expense |

How to Successfully Hack It |

Where the Saved Money Goes |

|

Subscriptions |

Audit statements and cancel unused applications. |

Straight into your emergency savings account. |

|

Food and Dining |

Meal prep and limit takeout to twice a month. |

Route directly to your long-term retirement accounts. |

|

Vehicle Insurance |

Shop around for better rates every single year. |

Use the difference to crush high-interest consumer debt. |

|

Impulse Purchases |

Use a strict 24-hour waiting rule for fun purchases. |

Keep the cash as a checking buffer to avoid fees. |

Final Thoughts

Wealth rarely happens because you decided to skip a latte on a Tuesday. It happens because you set up ironclad systems that make saving practically inevitable. Pay yourself first budgeting takes the heavy lifting off your shoulders. Stop fighting your natural urges to spend every dime you make. Lock up your future wealth before temptation even knocks on the door. Start incredibly small today.

Send just 5 percent to a high-yield account this Friday. Watch it grow without lifting a single finger. Once you see the magic happen, you will bump it to 10 percent, then 20 percent. Stop surviving on financial leftovers. Take control upfront and let the math do all the heavy lifting.

Frequently Asked Questions (FAQs) About Pay Yourself First Budgeting

Can I do this if I’m drowning in credit card debt?

Yes. Paying your future self includes wiping out bad debt. A guaranteed 25% return from killing credit card interest is incredible. Make debt your #1 automated target until it’s gone.

Does my employer 401(k) match count toward my savings goal?

Nope. Treat that as a bonus. If your goal is 15%, pull 15% from your own paycheck. The company match just gets you to the finish line faster.

What if a massive emergency drains my checking?

That’s exactly why you built the HYSA buffer first. Transfer the money back manually. Don’t starve yourself. Just make it slightly annoying to access the cash so you only tap it for real emergencies.

Should I pause automation for a vacation?

Please don’t. Keep the wealth engine running. Instead, set up a separate automated “sinking fund” just for travel. Send a small cut there every month so your trips are fully funded before you pack your bags.

{kind=link}